Elasticity values are critical in determining the impact of a government's taxation policies. The spending and taxing activities of the government influence the use of the economy's resources. By taxing cigarettes, alcohol and fuel, the government can restrict their use; by taxing income, the government influences the amount of time people choose to work. Taxes have a major impact on almost every sector of the Canadian economy.

To illustrate the role played by demand and supply elasticities in tax analysis, we take the example of a sales tax. These can be of the specific or ad valorem type. A specific tax involves a fixed dollar levy per unit of a good sold (e.g., $10 per airport departure). An ad valorem tax is a percentage levy, such as Canada's Goods and Services tax (e.g., 5 percent on top of the retail price of goods and services). The impact of each type of tax is similar, and we will use the specific tax in our example below.

A layperson's view of a sales tax is that the tax is borne by the consumer. That is to say, if no sales tax were imposed on the good or service in question, the price paid by the consumer would be the same net of tax price as exists when the tax is in place. Interestingly, this is not always the case. The study of the incidence of taxes is the study of who really bears the tax burden, and this in turn depends upon supply and demand elasticities.

Tax Incidence describes how the burden of a tax is shared between buyer and seller.

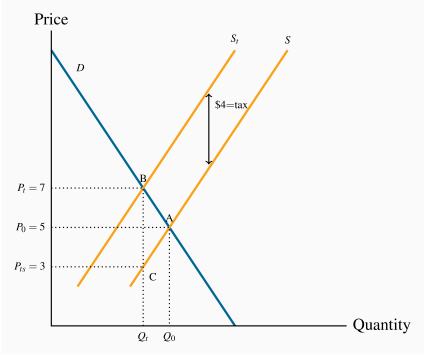

Consider Figures 4.8 and 4.9, which define an imaginary market for inexpensive wine. Let us suppose that, without a tax, the equilibrium price of a bottle of wine is $5, and Q0 is the equilibrium quantity traded. The pre-tax equilibrium is at the point A. The government now imposes a specific tax of $4 per bottle. The impact of the tax is represented by an upward shift in supply of $4: Regardless of the price that the consumer pays, $4 of that price must be remitted to the government. As a consequence, the price paid to the supplier must be $4 less than the consumer price, and this is represented by twin supply curves: One defines the price at which the supplier is willing to supply (S), and the other is the tax-inclusive supply curve that the consumer faces (St).

The introduction of the tax in Figure 4.8 means that consumers now face the supply curve St. The new equilibrium is at point B. Note that the price has increased by less than the full amount of the tax—in this example it has increased by $3. This is because the reduced quantity at B is provided at a lower supply price: The supplier is willing to supply the quantity Qt at a price defined by C ($4), which is lower than the price at A ($5).

So what is the incidence of the $4 tax? Since the market price has increased from $5 to $8, and the price obtained by the supplier has fallen by $1, we say that the incidence of the tax falls mainly on the consumer: The price to the consumer has risen by three dollars and the price received by the supplier has fallen by just one dollar.

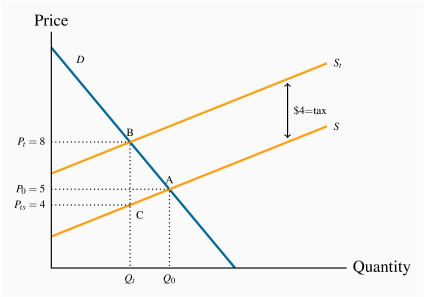

Consider now Figure 4.9, where the supply curve is less elastic, and the demand curve is unchanged. Again the supply curve must shift upward with the imposition of the  specific tax. But here the price received by the supplier is lower than in Figure 4.8, and the price paid by the consumer does not rise as much – the incidence is different. The consumer faces a price increase that is one-half, rather than three-quarters, of the tax value. The supplier faces a lower supply price, and bears a higher share of the tax.

specific tax. But here the price received by the supplier is lower than in Figure 4.8, and the price paid by the consumer does not rise as much – the incidence is different. The consumer faces a price increase that is one-half, rather than three-quarters, of the tax value. The supplier faces a lower supply price, and bears a higher share of the tax.

We can conclude from this example that, for any given demand, the more elastic is supply, the greater is the price increase in response to a given tax. Furthermore, a more elastic supply curve means that the incidence falls more on the consumer; while a less elastic supply curve means the incidence falls more on the supplier. This conclusion can be verified by drawing a third version of Figure 4.8 and 4.9, in which the supply curve is horizontal – perfectly elastic. When the tax is imposed the price to the consumer increases by the full value of the tax, and the full incidence falls on the buyer. While this case corresponds to the layperson's intuition of the incidence of a tax, economists recognize it as a special case of the more general outcome, where the incidence falls on both the supply side and the demand side.

These are key results in the theory of taxation. It is equally the case that the incidence of the tax depends upon the demand elasticity. In Figure 4.8 and 4.9 we used the same demand curve. However, it is not difficult to see that, if we were to redo the exercise with a demand curve of a different elasticity, the incidence would not be identical. At the same time, the general result on supply elasticities still holds. We will return to this material in Chapter 5.

Statutory incidence

In the above example the tax is analyzed by means of shifting the supply curve. This implies that the supplier is obliged to charge the consumer a tax and then return this tax revenue to the government. But suppose the supplier did not bear the obligation to collect the revenue; instead the buyer is required to send the tax revenue to the government, as in the case of employers who are required to deduct income tax from their employees' pay packages (the employers here are the demanders). If this were the case we could analyze the impact of the tax by reducing the market demand curve by the $4. This is because the demand curve reflects what buyers are willing to pay, and when suppliers are paid in the presence of the tax they will be paid the buyers' demand price minus the tax that the buyers must pay. It is not difficult to show that whether we move the supply curve upward (to reflect the responsibility of the supplier to pay the government) or move the demand curve downward, the outcome is the same – in the sense that the same price and quantity will be traded in each case. Furthermore the incidence of the tax, measured by how the price change is apportioned between the buyers and sellers is also unchanged.

Tax revenues and tax rates

It is useful to relate elasticity values to the policy question of the impact of higher or lower taxes on government tax revenue. Consider a situation in which a tax is already in place and the government considers increasing the rate of tax. Can an understanding of elasticities inform us on the likely outcome? The answer is yes. Suppose that at the initial tax-inclusive price demand is inelastic. We know immediately that a tax rate increase that increases the price must increase total expenditure. Hence the outcome is that the government will get a higher share of an increased total expenditure. In contrast, if demand is elastic at the initial tax-inclusive price a tax rate increase that leads to a higher price will decrease total expenditure. In this case the government will get a larger share of a smaller pie – not as valuable from a tax-revenue standpoint as a larger share of a larger pie.

), the government gets $4 also and the consumer pays $8. The greater part of the incidence is upon the buyer, on account of the relatively elastic supply curve: His price increases by $3 of the $4 tax.

), the government gets $4 also and the consumer pays $8. The greater part of the incidence is upon the buyer, on account of the relatively elastic supply curve: His price increases by $3 of the $4 tax.