13.4: Problems of Health Care in the United States

- Page ID

- 14574

Private Health Insurance and the Lack of Insurance

| Source of coverage | Percentage of people with this coverage |

|---|---|

| Employer | 49% |

| Individual | 5% |

| Medicaid | 16% |

| Medicare | 12% |

| Other public | 1% |

| Uninsured | 16% |

Applying Social Research

As the text discusses, studies show that Americans without health insurance are at greater risk for a variety of illnesses and life-threatening conditions. Although this research evidence is compelling, uninsured Americans may differ from insured Americans in other ways that also put their health at risk. For example, perhaps people who do not buy health insurance may be less concerned about their health and thus less likely to take good care of themselves. Because many studies have not controlled for all such differences, experimental evidence would be more conclusive (see Chapter 1).

For this reason, the results of a fascinating real-life experiment in Oregon were very significant. In 2008, Oregon decided to expand its Medicaid coverage. Because it could not accommodate all the poor Oregonians who were otherwise uninsured, it had them apply for Medicaid by lottery. Researchers then compared the subsequent health of the Oregonians who ended up on Medicaid with that of Oregonians who remained uninsured. Because the two groups resulted from random assignment (the lottery), it is reasonable to conclude that any later differences between them must have stemmed from the presence or absence of Medicaid coverage.

Although this study is ongoing, initial results obtained a year after it began showed that Medicaid coverage had already made quite a difference. Compared to the uninsured “control” group, the newly insured Oregonians rated themselves happier and in better health and reported fewer sick days from work. They were also 50 percent more likely to have seen a primary care doctor in the year since they received coverage, and women were 60 percent more likely to have had a mammogram. In another effect, they were much less likely to report having had to borrow money or not pay other bills because of medical expenses.

A news report summarized these benefits of the new Medicaid coverage: “[The researchers] found that Medicaid’s impact on health, happiness, and general well-being is enormous, and delivered at relatively low cost: Low-income Oregonians whose names were selected by lottery to apply for Medicaid availed themselves of more treatment and preventive care than those who remained excluded from government health insurance. After a year with insurance, the Medicaid lottery winners were happier, healthier, and under less financial strain.”

Because of this study’s experimental design, it “represents the best evidence we’ve got,” according to the news report, of the benefits of health insurance coverage. As researchers continue to study the two groups in the years ahead and begin to collect data on blood pressure, cardiovascular health, and other objective indicators of health, they will add to our knowledge of the effects of health insurance coverage.

Sources: Baicker & Finkelstein, 2011; Fisman, 2011Baicker, K., & Finkelstein, A. (2011). The effects of Medicaid coverage—learning from the Oregon experiment. New England Journal of Medicine, 365(8), 683–685; Fisman, R. (2011, July 7). Does health coverage make people healthier? Slate.com. Retrieved from http://www.slate.com/articles/business/the_dismal_science/2011/07/does_health_coverage_make_people_healthier.html.

Although 29 percent of Americans do have public insurance, this percentage and the coverage provided by this insurance do not begin to match the coverage enjoyed by the rest of the industrial world. Although Medicare pays some medical costs for the elderly, we saw in Chapter 6 that its coverage is hardly adequate, as many people must pay hundreds or even thousands of dollars in premiums, deductibles, coinsurance, and copayments. The other government program, Medicaid, pays some health-care costs for the poor, but many low-income families are not poor enough to receive Medicaid. Eligibility standards for Medicaid vary from one state to another, and a family poor enough in one state to receive Medicaid might not be considered poor enough in another state. The State Children’s Health Insurance Program (SCHIP), begun in 1997 for children from low-income families, has helped somewhat, but it, too, fails to cover many low-income children. Largely for these reasons, about two-thirds of uninsured Americans come from low-income families.

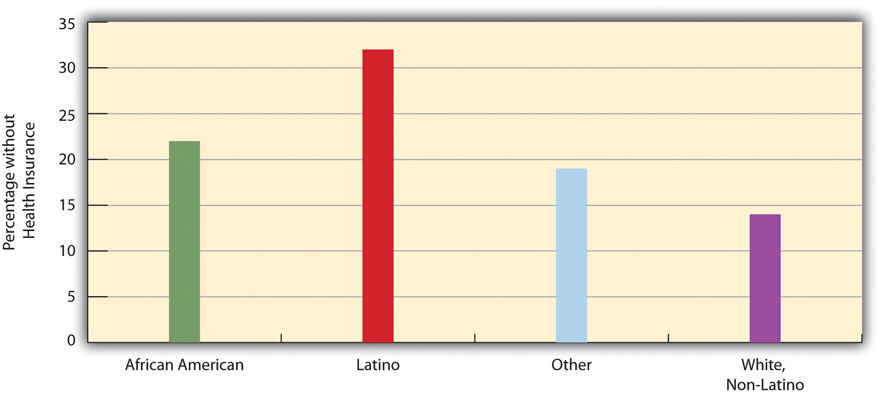

Not surprisingly, the 16 percent uninsured rate varies by race and ethnicity (see Figure 13.7). Among people under 65 and thus not eligible for Medicare, the uninsured rate rises to almost 22 percent of the African American population and 32 percent of the Latino population. Moreover, 45 percent of adults under 65 who live in official poverty lack health insurance, compared to only 6 percent of higher-income adults (those with incomes higher than four times the poverty level). Almost one-fifth of poor children have no health insurance, compared to only 3 percent of children in higher-income families (Kaiser Family Foundation, 2012).Kaiser Family Foundation. (2012). State health facts. Retrieved from http://www.statehealthfacts.org. As discussed earlier, the lack of health insurance among the poor and people of color is a significant reason for their poorer health.

The High Cost of Health Care

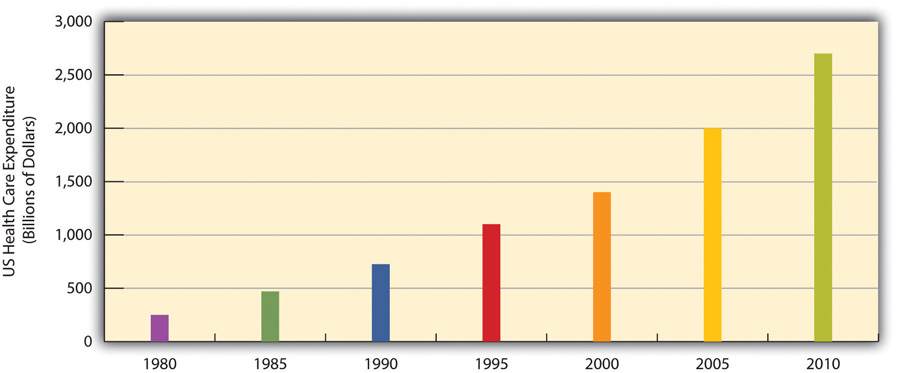

As noted earlier, the United States spends much more money per capita on health care than any other industrial nation. The US per capita health expenditure was $7,960 in 2009, the latest year for which data were available at the time of this writing. This figure was about 50 percent higher than that for the next two highest-spending countries, Norway and Switzerland; 80 percent higher than Canada’s expenditure; twice as high as Frances’s expenditure; and 2.3 times higher than the United Kingdom’s expenditure (Organisation for Economic Co-operation and Development, 2011).Organisation for Economic Co-operation and Development. (2011). Health at a glance 2011: OECD indicators. Paris, France: Author. The huge expenditure by the United States might be justified if the quality of health and of health care in this nation outranked that in its peer nations. As we have seen, however, the United States lags behind many of its peer nations in several indicators of health and health care quality. If the United States spends far more than its peer nations on health care yet still lags behind them in many indicators, an inescapable conclusion is that the United States is spending much more than it should be spending.

Why is US spending on health care so high? Although this is a complex issue, two reasons stand out (Boffey, 2012).Boffey, P. M. (2012, January 22). The money traps in US health care. New York Times, p. SR12. First, administrative costs for health care in the United States are the highest in the industrial world. Because so much of US health insurance is private, billing and record-keeping tasks are immense, and “hordes of clerks and accountants [are] needed to deal with insurance paperwork,” according to one observer (Boffey, 2012, p. SR12).Boffey, P. M. (2012, January 22). The money traps in US health care. New York Times, p. SR12. Billing and other administrative tasks cost about $360 billion annually, or 14 percent of all US health-care costs (Emanuel, 2011).Emanuel, E. J. (2011, November 12). Billions wasted on billing. New York Times. Retrieved from http://opinionator.blogs.nytimes.com/2011/2011/2012/billions-wasted-on-billing/?ref=opinion. These tasks are unnecessarily cumbersome and fail to take advantage of electronic technologies that would make them much more efficient.

Second, the United States relies on a fee for service model for private insurance. Under this model, physicians, hospitals, and health care professionals and business are relatively free to charge whatever they want for their services. In the other industrial nations, government regulations keep prices lower. This basic difference between the United States and its peer nations helps explain why the cost of health care services in the United States is so much higher than in its peer nations. Simply put, US physicians and hospitals charge much more for their services than do their counterparts in other industrial nations (Klein, 2012).Klein, E. (2012, March 2). High health-care costs: It’s all in the pricing. The Washington Post. Retrieved from http://www.washingtonpost.com/business/high-health-care-costs-its-all-in-the-pricing/2012/02/28/gIQAtbhimR_story.html. And because physicians are paid for every service they perform, they have an incentive to perform more diagnostic tests and other procedures than necessary. As one economic writer recently said, “The more they do, the more they earn” (Samuelson, 2011).Samuelson, R. J. (2011, November 28). A grim diagnosis for our ailing health care system. The Washington Post. Retrieved from http://www.washingtonpost.com/opinions/a-grim-diagnosis-for-our-ailing-us-health-care-system/2011/11/25/gIQARdgm2N_story.html.

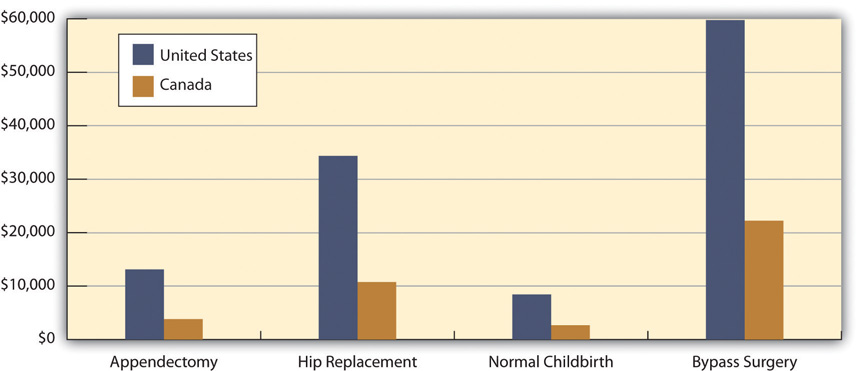

A few examples illustrate the higher cost of medical procedures in the United States compared to other nations. To keep things simple, we will compare the United States with just Canada (see Figure 13.8). The average US appendectomy costs $13,123, compared to $3,810 in Canada; the average US hip replacement costs $34,354, compared to $10,753 in Canada; the average US normal childbirth costs $8,435, compared to $2,667 in Canada; and the average US bypass surgery costs $59,770, compared to $22,212 in Canada. The costs of diagnostic tests also differ dramatically between the two nations. For example, a head CT scan costs an average of $464 in the United States, compared to only $65 in Canada, and an MRI scan costs and average of $1,009 in the United States, compared to only $304 in Canada (International Federation of Health Plans, 2010).International Federation of Health Plans. (2010). 2010 comparative price report: Medical and hospital fees by country. London, United Kingdom: Author.

Managed Care and HMOs

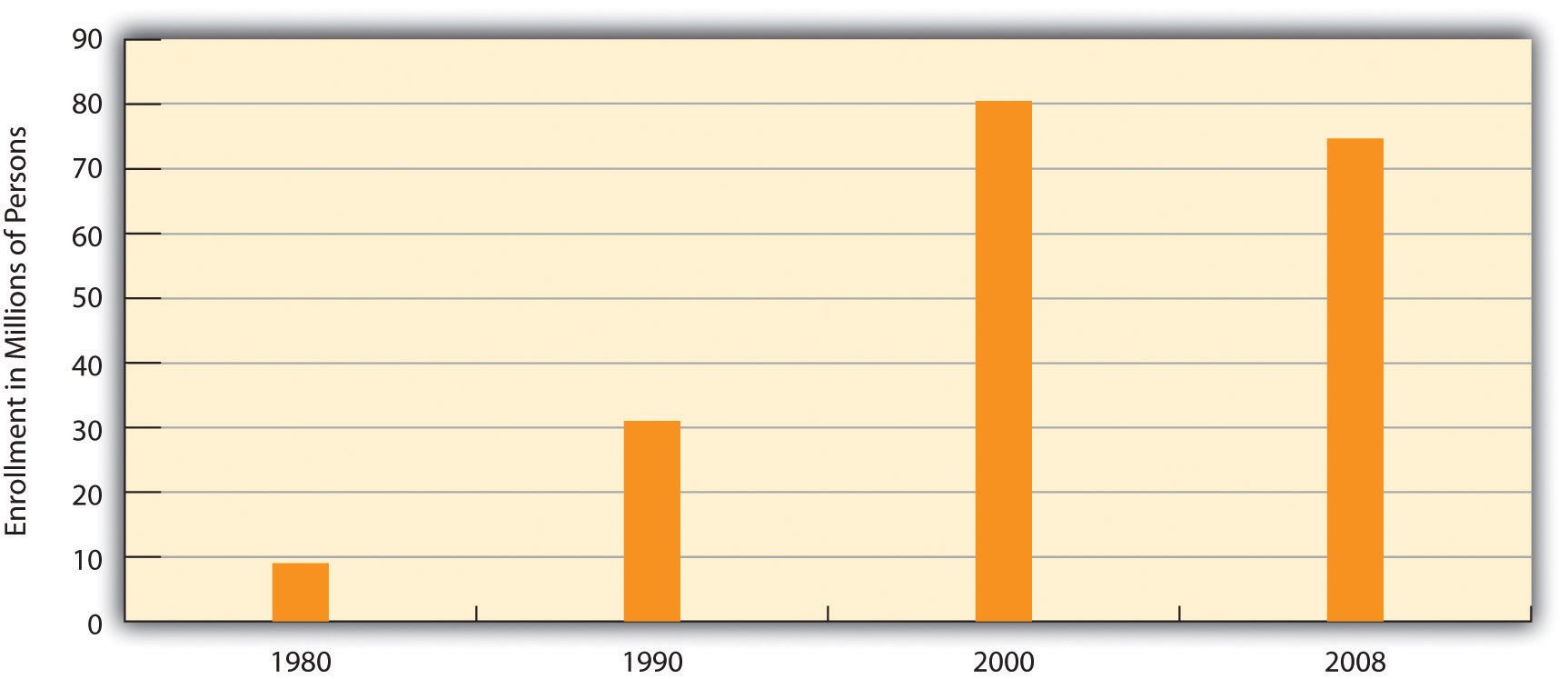

To many critics, a disturbing development in the US health-care system has been the establishment of health maintenance organizations, or HMOs, which typically enroll their subscribers through their workplaces. HMOs are prepaid health plans with designated providers, meaning that patients must visit a physician employed by the HMO or included on the HMO’s approved list of physicians. If their physician is not approved by the HMO, they have to either see an approved physician or see their own without insurance coverage. Popular with employers because they are less expensive than traditional private insurance, HMOs have grown rapidly in the last three decades and now enroll more than 70 million Americans (see Figure 13.9).

Although HMOs have become popular, their managed care is also very controversial for at least two reasons (Kronick, 2009).Kronick, R. (2009). Medicare and HMOs—The Search for Accountability. New England Journal of Medicine, 360, 2048–2050. The first is the HMOs’ restrictions just noted on the choice of physicians and other health-care providers. Families who have long seen a family physician but whose employer now enrolls them in an HMO sometimes find they have to see another physician or risk going without coverage. In some HMOs, patients have no guarantee that they can see the same physician at every visit. Instead, they see whichever physician is assigned to them at each visit. Critics of HMOs argue that this practice prevents physicians and patients from getting to know each other, reduces patients’ trust in their physician, and may for these reasons impair patient health.

The second reason for the managed-care controversy is perhaps more important. HMOs often restrict the types of medical exams and procedures patients may undergo, a problem called denial of care, and limit their choice of prescription drugs to those approved by the HMO, even if their physicians think that another, typically more expensive drug would be more effective. HMOs claim that these restrictions are necessary to keep medical costs down and do not harm patients.

Racial and Gender Bias in Health Care

Another problem in the US medical practice is apparent racial and gender bias in health care. Racial bias seems fairly common; as Chapter 3 discussed, African Americans are less likely than whites with the same health problems to receive various medical procedures (Samal, Lipsitz, & Hicks, 2012).Samal, L., Lipsitz, S. R., & Hicks, L. S. (2012). Impact of electronic health records on racial and ethnic disparities in blood pressure control at US primary care visits. Archives of Internal Medicine, 172(1), 75–76. Gender bias also appears to affect the quality of health care (Read & Gorman, 2010).Read, J. G., & Gorman, B. M. (2010). Gender and health inequality. Annual Review of Sociology, 36, 371–386. Research that examines either actual cases or hypothetical cases posed to physicians finds that women are less likely than men with similar health problems to be recommended for various procedures, medications, and diagnostic tests, including cardiac catheterization, lipid-lowering medication, kidney dialysis or transplant, and knee replacement for osteoarthritis (Borkhoff et al., 2008).Borkhoff, C. M., Hawker, G. A., Kreder, H. J., Glazier, R. H., Mahomed, N. N., & Wright, J. G. (2008). The effect of patients’ sex on physicians’ recommendations for total knee arthroplasty. Canadian Medical Association Journal, 178(6), 681–687.

Other Problems in the Quality of Care

Other problems in the quality of medical care also put patients unnecessarily at risk. We examine three of these here:

Medical Ethics and Medical Fraud

A final set of problems concerns questions of medical ethics and outright medical fraud. Many types of health-care providers, including physicians, dentists, medical equipment companies, and nursing homes, engage in many types of health-care fraud. In a common type of fraud, they sometimes bill Medicare, Medicaid, and private insurance companies for exams or tests that were never done and even make up “ghost patients” who never existed or bill for patients who were dead by the time they were allegedly treated. In just one example, a group of New York physicians billed their state’s Medicaid program for over $1.3 million for 50,000 psychotherapy sessions that never occurred. All types of health-care fraud combined are estimated to cost about $100 billion per year (Kavilanz, 2010).Kavilanz, P. (2010, January 13). Health care: A “gold mine” for fraudsters. CNN Money. Retrieved from http://money.cnn.com/2010/01/13/news/economy/health_care_fraud.

Other practices are legal but ethically questionable. Sometimes physicians refer their patients for tests to a laboratory that they own or in which they have invested. They are more likely to refer patients for tests when they have a financial interest in the lab to which the patients are sent. This practice, called self-referral, is legal but does raise questions of whether the tests are in the patient’s best interests or instead in the physician’s best interests (Shreibati & Baker, 2011).Shreibati, J. B., & Baker, L. C. (2011). The relationship between low back magnetic resonance imaging, surgery, and spending: Impact of physician self-referral status. Health Services Research, 46(5), 1362–1381.

In another practice, physicians have asked hundreds of thousands of their patients to take part in drug trials. The physicians may receive more than $1,000 for each patient they sign up, but the patients are not told about these payments. Characterizing these trials, two reporters said that “patients have become commodities, bought and traded by testing companies and physicians” and said that it “injects the interests of a giant industry into the delicate physician-patient relationship, usually without the patient realizing it” (Eichenwald & Kolata, 1999; Galewitz, 2009).Eichenwald, K., & Kolata, G. (1999, May 16). Drug trials hide conflicts for doctors. New York Times, p. A1; Galewitz, P. (2009, February 22). Cutting-edge option: Doctors paid by drugmakers, but say trials not about money. Palm Beach Post. Retrieved from http://www.mdmediaconnection.com/printmedia.php#!prettyPhoto[iframe2]/0/. These trials raise obvious conflicts of interest for the physicians, who may recommend their patients do something that might not be good for them but would be good for the physicians’ finances.