10.1: Perfect Competition

- Last updated

- Save as PDF

- Page ID

- 3491

- Boundless

- Boundless

Definition of Perfect Competition

Perfect competition is a market structure that leads to the Pareto-efficient allocation of economic resources.

Learning Objectives

- Describe degrees of competition in different market structures

Market structure is determined by the number and size distribution of firms in a market, entry conditions, and the extent of product differentiation. The major types of market structure include the following:

- Monopoly: An industry structure where a single firm produces a product for which there are no close substitutes. Monopolists are price makers. Barriers to entry and exit exist, and, in order to ensure profits, a monopoly will attempt to maintain them.

- Monopolistic competition: A market structure in which there is a large number of firms, each having a small portion of the market share and slightly differentiated products. There are close substitutes for the product of any given firm, so competitors have slight control over price. There are relatively insignificant barriers to entry or exit, and success invites new competitors into the industry.

- Oligopoly: An industry structure in which there are a few firms producing products that range from slightly differentiated to highly differentiated. Each firm is large enough to influence the industry. Barriers to entry exist.

- Perfect competition: An industry structure in which there are many firms, none large enough to influence the industry, producing homogeneous products. Firms are price takers. There are no barriers to entry. Agriculture comes close to being perfectly competitive.

Perfect competition leads to the Pareto-efficient allocation of economic resources. Because of this it serves as a natural benchmark against which to contrast other market structures. However, in practice, very few industries can be described as perfectly competitive. Nevertheless, it is used because it provides important insights.

A perfectly competitive market has several important characteristics:

- All producers contribute insignificantly to the market. Their own production levels do not change the supply curve.

- All producers are price takers. They cannot influence the market. If a firm tries to raise its price consumers would buy from a competitor with a lower price instead.

- Products are homogeneous. The characteristics of a good or service do not vary between suppliers.

- Producers enter and exit the market freely.

- Both buyers and sellers have perfect information about the price, utility, quality, and production methods of products.

- There are no transaction costs. Buyers and sellers do not incur costs in making an exchange of goods in a perfectly competitive market.

- Producers earn zero economic profits in the long run.

Conditions of Perfect Competition

A firm in a perfectly competitive market may generate a profit in the short-run, but in the long-run it will have economic profits of zero.

Learning Objectives

- Calculate total revenue, average revenue, and marginal revenue for a firm in a perfectly competitive market

The concept of perfect competition applies when there are many producers and consumers in the market and no single company can influence the pricing. A perfectly competitive market has the following characteristics:

- There are many buyers and sellers in the market.

- Each company makes a similar product.

- Buyers and sellers have access to perfect information about price.

- There are no transaction costs.

- There are no barriers to entry into or exit from the market.

All goods in a perfectly competitive market are considered perfect substitutes, and the demand curve is perfectly elastic for each of the small, individual firms that participate in the market. These firms are price takers–if one firm tries to raise its price, there would be no demand for that firm’s product. Consumers would buy from another firm at a lower price instead.

Firm Revenues

A firm in a competitive market wants to maximize profits just like any other firm. The profit is the difference between a firm’s total revenue and its total cost. For a firm operating in a perfectly competitive market, the revenue is calculated as follows:

- Total Revenue = Price * Quantity

- AR (Average Revenue) = Total Revenue / Quantity

- MR (Marginal Revenue) = Change in Total Revenue / Change in Quantity

The average revenue (AR) is the amount of revenue a firm receives for each unit of output. The marginal revenue (MR) is the change in total revenue from an additional unit of output sold. For all firms in a competitive market, both AR and MR will be equal to the price.

Profit Maximization

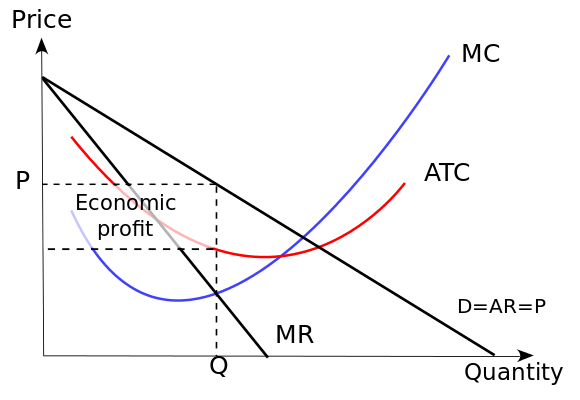

In order to maximize profits in a perfectly competitive market, firms set marginal revenue equal to marginal cost (MR=MC). MR is the slope of the revenue curve, which is also equal to the demand curve (D) and price (P). In the short-term, it is possible for economic profits to be positive, zero, or negative. When price is greater than average total cost, the firm is making a profit. When price is less than average total cost, the firm is making a loss in the market.

Perfect Competition in the Short Run: In the short run, it is possible for an individual firm to make an economic profit. This scenario is shown in this diagram, as the price or average revenue, denoted by P, is above the average cost denoted by C.

Over the long-run, if firms in a perfectly competitive market are earning positive economic profits, more firms will enter the market, which will shift the supply curve to the right. As the supply curve shifts to the right, the equilibrium price will go down. As the price goes down, economic profits will decrease until they become zero.

When price is less than average total cost, firms are making a loss. Over the long-run, if firms in a perfectly competitive market are earning negative economic profits, more firms will leave the market, which will shift the supply curve left. As the supply curve shifts left, the price will go up. As the price goes up, economic profits will increase until they become zero.

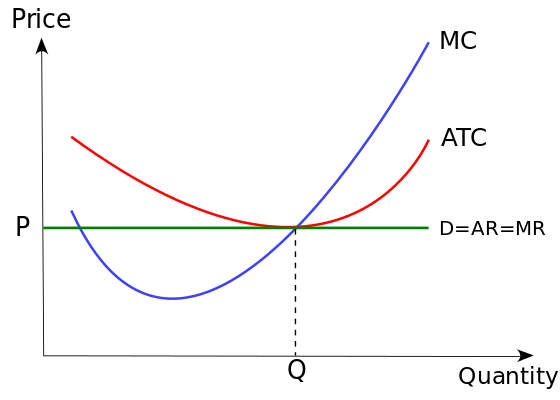

In sum, in the long-run, companies that are engaged in a perfectly competitive market earn zero economic profits. The long-run equilibrium point for a perfectly competitive market occurs where the demand curve (price) intersects the marginal cost (MC) curve and the minimum point of the average cost (AC) curve.

Perfect Competition in the Long Run: In the long-run, economic profit cannot be sustained. The arrival of new firms in the market causes the demand curve of each individual firm to shift downward, bringing down the price, the average revenue and marginal revenue curve. In the long-run, the firm will make zero economic profit. Its horizontal demand curve will touch its average total cost curve at its lowest point.

The Demand Curve in Perfect Competition

A perfectly competitive firm faces a demand curve is a horizontal line equal to the equilibrium price of the entire market.

Learning Objectives

- Describe the demand for goods in perfectly competitive markets

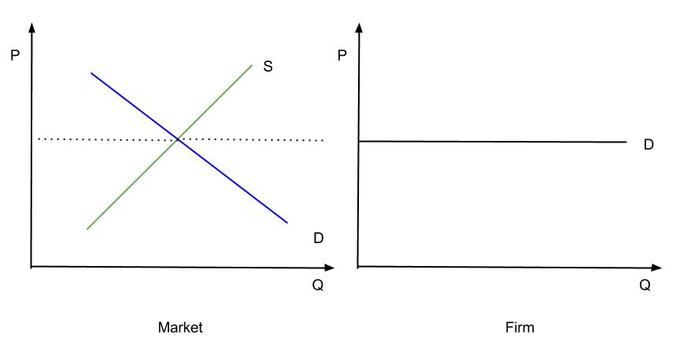

In a perfectly competitive market the market demand curve is a downward sloping line, reflecting the fact that as the price of an ordinary good increases, the quantity demanded of that good decreases. Price is determined by the intersection of market demand and market supply; individual firms do not have any influence on the market price in perfect competition. Once the market price has been determined by market supply and demand forces, individual firms become price takers. Individual firms are forced to charge the equilibrium price of the market or consumers will purchase the product from the numerous other firms in the market charging a lower price (keep in mind the key conditions of perfect competition). The demand curve for an individual firm is thus equal to the equilibrium price of the market.

Demand Curve for a Firm in a Perfectly Competitive Market: The demand curve for an individual firm is equal to the equilibrium price of the market. The market demand curve is downward-sloping.

The demand curve for a firm in a perfectly competitive market varies significantly from that of the entire market.The market demand curve slopes downward, while the perfectly competitive firm’s demand curve is a horizontal line equal to the equilibrium price of the entire market. The horizontal demand curve indicates that the elasticity of demand for the good is perfectly elastic. This means that if any individual firm charged a price slightly above market price, it would not sell any products.

A strategy often used to increase market share is to offer a firm’s product at a lower price than the competitors. In a perfectly competitive market, firms cannot decrease their product price without making a negative profit. Instead, assuming that the firm is a profit-maximizer, it will sell its goods at the market price.

Key Points

- The major types of market structure include monopoly, monopolistic competition, oligopoly, and perfect competition.

- Perfect competition is an industry structure in which there are many firms producing homogeneous products. None of the firms are large enough to influence the industry.

- The characteristics of a perfectly competitive market include insignificant contributions from the producers, homogenous products, perfect information about products, no transaction costs, and no long-term economic profits.

- In practice, very few industries can be described as perfectly competitive, though agriculture comes close.

- A perfectly competitive market is characterized by many buyers and sellers, undifferentiated products, no transaction costs, no barriers to entry and exit, and perfect information about the price of a good.

- The total revenue for a firm in a perfectly competitive market is the product of price and quantity (TR = P * Q). The average revenue is calculated by dividing total revenue by quantity. Marginal revenue is calculated by dividing the change in total revenue by change in quantity.

- A firm in a competitive market tries to maximize profits. In the short-run, it is possible for a firm’s economic profits to be positive, negative, or zero. Economic profits will be zero in the long-run.

- In the short-run, if a firm has a negative economic profit, it should continue to operate if its price exceeds its average variable cost. It should shut down if its price is below its average variable cost.

- In a perfectly competitive market individual firms are price takers. The price is determined by the intersection of the market supply and demand curves.

- The demand curve for an individual firm is different from a market demand curve. The market demand curve slopes downward, while the firm’s demand curve is a horizontal line.

- The firm’s horizontal demand curve indicates a price elasticity of demand that is perfectly elastic.

Key Terms

- monopoly: A situation, by legal privilege or other agreement, in which solely one party (company, cartel etc. ) exclusively provides a particular product or service, dominating that market and generally exerting powerful control over it.

- Monopolistic competition: A market structure in which there is a large number of firms, each having a small proportion of the market share and slightly differentiated products.

- oligopoly: An economic condition in which a small number of sellers exert control over the market of a commodity.

- economic profit: The difference between the total revenue received by the firm from its sales and the total opportunity costs of all the resources used by the firm.

- Perfectly elastic: Describes a situation when any increase in the price, no matter how small, will cause demand for a good to drop to zero.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- Principles of Economics/Perfect Competition. Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/Princip...ct_competition. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition - Interpretation of the long-run supply curve. Provided by: mbaecon Wikispace. Located at: http://mbaecon.wikispaces.com/Perfec...n+supply+curve. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Perfect_competition. License: CC BY-SA: Attribution-ShareAlike

- Imperfect competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Imperfect_competition. License: CC BY-SA: Attribution-ShareAlike

- Market structure. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Market_structure. License: CC BY-SA: Attribution-ShareAlike

- IB Economics/Microeconomics/Markets. Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/IB_Econ...nomics/Markets. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Perfect_competition. License: CC BY-SA: Attribution-ShareAlike

- IB Economics/Microeconomics/Theory of the Firm (HL). Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/IB_Econ...ct_Competition. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Perfect_competition. License: CC BY-SA: Attribution-ShareAlike

- Monopolistic competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Monopol...%20competition. License: CC BY-SA: Attribution-ShareAlike

- Boundless. Provided by: Boundless Learning. Located at: www.boundless.com//economics/...ition/monopoly. License: CC BY-SA: Attribution-ShareAlike

- oligopoly. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/oligopoly. License: CC BY-SA: Attribution-ShareAlike

- Chapter 14 FIRMS IN COMPETITIVE MARKET Erica. Provided by: mrski-apecon-2008 Wikispace. Located at: http://mrski-apecon-2008.wikispaces....E+MARKET+Erica. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition - Interpretation of the long-run supply curve. Provided by: mbaecon Wikispace. Located at: http://mbaecon.wikispaces.com/Perfec...n+supply+curve. License: CC BY-SA: Attribution-ShareAlike

- Ch.14 Firms in Competitive Markets. Provided by: mrski-apecon-2008 Wikispace. Located at: http://mrski-apecon-2008.wikispaces....titive+Markets. License: CC BY-SA: Attribution-ShareAlike

- Microeconomics/Perfect Competition. Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/Microec...ct_Competition. License: CC BY-SA: Attribution-ShareAlike

- Boundless. Provided by: Boundless Learning. Located at: www.boundless.com//economics/...omic-profit--2. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition in the short run. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Pe..._short_run.svg. License: CC BY-SA: Attribution-ShareAlike

- Economics Perfect competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Ec...ompetition.svg. License: CC BY-SA: Attribution-ShareAlike

- Perfect Competition. Provided by: Central Economics Wiki. Located at: http://centralecon.wikia.com/wiki/Perfect_Competition. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition - Interpretation of the long-run supply curve. Provided by: mbaecon Wikispace. Located at: http://mbaecon.wikispaces.com/Perfec...n+supply+curve. License: CC BY-SA: Attribution-ShareAlike

- Chapter 14 FIRMS IN COMPETITIVE MARKET Erica. Provided by: mrski-apecon-2008 Wikispace. Located at: http://mrski-apecon-2008.wikispaces....E+MARKET+Erica. License: CC BY-SA: Attribution-ShareAlike

- Interpretation of the long-run supply curve (perfect competition). Provided by: mba651fall2007 Wikispace. Located at: http://mba651fall2007.wikispaces.com...++competition). License: CC BY-SA: Attribution-ShareAlike

- Perfectly elastic. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Perfectly%20elastic. License: CC BY-SA: Attribution-ShareAlike

- Perfect competition in the short run. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Pe..._short_run.svg. License: CC BY-SA: Attribution-ShareAlike

- Economics Perfect competition. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Ec...ompetition.svg. License: CC BY-SA: Attribution-ShareAlike

- Demand in Perfectly Competitive Market. Provided by: Wikimedia. Located at: commons.wikimedia.org/wiki/F...ive_Market.jpg. License: CC BY-SA: Attribution-ShareAlike