14.5: Capital, Productivity, and Technology

- Last updated

- Save as PDF

- Page ID

- 3523

- Boundless

- Boundless

Capital and Technology

Firms add capital to the point where the value of marginal product of capital is equal to the rental rate of capital.

learning objectives

- Analyze how firms determine the amount of capital to use in production.

Capital is a factor of production, along with labor and land. It consists of the infrastructure and equipment used to produce goods and services. Capital can include factory buildings, vehicles, plant machinery, and tools used in the production process. Firms may buy, rent, or lease infrastructure and tools in the capital market, but even if the firm owns these factors of production, the opportunity cost of using this capital is the foregone rent that the firm could receive if it rented the capital to somebody else rather than using it for production. Because of this, we say that the price of capital is the rental rate.

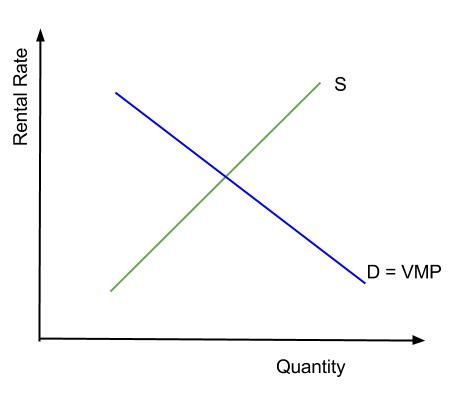

A firm decides how much of each factor input to use and how much output to produce based on the market prices for outputs and inputs, as well as exogenous technological determinants represented by the production function. The production function describes the relationship between the quantity of inputs used in production and the quantity of output. It can be used to derive the marginal product for capital, which is the increase in the amount of output from an additional unit of capital. The value of marginal product (VMP) of capital is the marginal product of capital multiplied by price. The downward-sloping demand curve for capital, which is equal to the VMP of capital, reflects the fact that the production process exhibits diminishing marginal product. A firm will continue to add capital up to the point where the rental rate is equal to the value of marginal product of capital, which is the point of equilibrium.

Firm Demand for Capital: Firms will increase the quantity of capital hired to the point where the value of marginal product of capital is equal to the rental rate of capital.

Total Factor Productivity

Total factor productivity, which captures how efficiently inputs are utilized, is a key indicator of competitiveness.

learning objectives

- Discuss the importance of Total Factor Productivity in comparing firms, industries, and countries.

Total factor productivity measures the residual growth in total output of a firm, industry, or national economy that cannot be explained by the accumulation of traditional inputs such as labor and capital. Increases in total factor productivity reflect a more efficient use of inputs, and total factor productivity is often taken as a measure of long-term technological change or dynamism brought about by such factors as technical innovation.

Total Factor Productivity: Total output is not only a function of labor and capital, but also of total factor productivity, a measure of efficiency.

Total factor productivity cannot be measured directly. Instead, it is a residual which accounts for effects on total output not caused by inputs. In the Cobb-Douglas production function, total factor productivity is captured by the variable A:

\[Y=AK^αL^β\]

In the equation above, Y represents total output, K represents capital input, L represents labor input, and alpha and beta are the two inputs’ respective shares of output. An increase in K or L will lead to an increase in output. However, due to to the law of diminishing returns, the increased use of inputs will fail to yield increased output in the long run. The quantity of inputs used thus does not completely determine the amount of output produced. How effectively the factors of production are used is also important. Total factor productivity is less tangible than capital and labor inputs, and it can account for a range of factors, from technology, to human capital, to organizational innovation.

Total factor productivity can be used to measure competitiveness. The higher a country’s total factor productivity, the more competitive it is likely to be (subject to constraints such as resources). It is also generally viewed as one of the main vehicles for driving economic growth.

When a country is able to increase its total factor productivity, it can yield higher output with the same resources, and therefore drive economic growth.

Changes in Technology Over Time

Technological improvement improves the efficiency of production, which increases supply and lowers prices.

learning objectives

- Summarize how changes in technology affect a firm’s decision to produce.

Factors of production typically include land, labor, capital, and natural resources. These inputs are used directly to produce a good or service. Technology, on the other hand, is used to put these factors of production to work. A firm doesn’t purchase additional units of technology to feed into the production process in the same way that a firm might hire more labor in order to increase output. Instead, the technology available in a particular industry or economy allows firms to use labor and capital more or less efficiently. It is important to note that advances in technology are a result of innovation, innovative practices such as process changes are also worth mentioning in this context. Innovation is the driving economic force behind these leaps in efficiency.

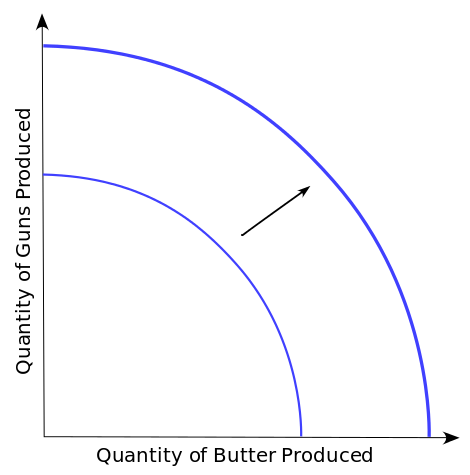

Technological change is a term used to describe any change in the set of feasible production possibilities. A change in technology alters the combinations of inputs or the types of inputs required in the production process. An improvement in technology usually means that fewer and/or less costly inputs are needed. If the cost of production is lower, the profits available at a given price will increase, and producers will produce more. With more produced at every price, the supply curve will shift to the right, meaning an increase in supply and a decrease in prices. For the economy as a whole, an improvement in technology shifts the production possibilities frontier outward.

Production Possibility Frontier (PPF): An increase in technology that allows for greater output based upon the same inputs can be described as an outward shift of the PPF, as demonstrated in this figure.

The invention and popularization of the assembly line is an example of process change, which is worth mentioning in context with technological change. Innovative practices to how we do this is an example of the way in which output can be increased with the same input, and is often discussed in conjunction with technological innovation. During the industrial revolution, many products that had previously been created by hand by a single person or a team of craftsmen began to be manufactured instead in factories in which each worker performed one simple operation. This meant that companies could produce much more output using the same amount of raw materials, capital, and labor. Supply of these goods increased, and the production possibilities curve for the entire economy shifted outwards.

Technological change in the computer industry has resulting in a shift of the computer supply curve. Due to advances in technology, computers can now be manufactured more cheaply, even though they continue to grow smaller, faster, and more powerful. Producers respond to the cheaper production process by increasing output, shifting the supply curve outwards. Thus, the number of computers produced increases and the price of computers falls.

Key Points

- Capital is the infrastructure and equipment used to produce goods and services.

- The production function describes the relationship between the quantity of inputs used in production and the quantity of output. It can be used to derive the marginal product for capital.

- The value of marginal product (VMP) of capital is the marginal product of capital multiplied by its price. The firm ‘s demand curve for capital is derived from the VMP of capital.

- Total factor productivity measures the residual growth in total output of a firm, industry, or national economy that cannot be explained by the accumulation of traditional inputs such as labor and capital.

- Total factor productivity cannot be measured directly. Instead, it is a residual which accounts for effects on total output not caused by inputs.

- Total factor productivity is considered one of the key indicators of competitiveness. It is also accepted by economics as the main contributing factor to economic growth.

- The technology available in a particular industry or economy allows firms to use labor and capital more or less efficiently.

- A change in technology alters the combination of inputs required in the production process. An improvement in technology usually means that fewer and/or less costly inputs are needed.

- If the cost of production is lower, the profits available at a given price will increase, and producers will produce more.

- While we usually think of technology as enhancing production, declines in production due to problems in technology are also possible.

Key Terms

- Production function: Relates physical output of a production process to physical inputs or factors of production.

- Value of marginal product of capital: The marginal product of capital multiplied by its price.

- Total factor productivity: A variable which accounts for effects in total output not caused by traditionally measured inputs of labor and capital.

- input: Something fed into a process with the intention of it shaping or affecting the outputs of that process.

- assembly line: A system of workers and machinery in which a product is assembled in a series of consecutive operations; typically the product is attached to a continuously moving belt

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- CHAPTER 18 .THE MARKETS FOR THE FACTORS OF PRODUCTION. Provided by: mrski-apecon-2008 Wikispace. Located at: http://mrski-apecon-2008.wikispaces....F+PRODUCTION+;). License: CC BY-SA: Attribution-ShareAlike

- IB Economics/Development Economics/Sources of Economic Growth and/or Development. Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/IB_Econ...pment.2FGrowth. License: CC BY-SA: Attribution-ShareAlike

- A-level Economics/AQA/Markets and Market failure. Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/A-level..._of_Production. License: CC BY-SA: Attribution-ShareAlike

- Factor payments (economics). Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Factor_payments_(economics). License: CC BY-SA: Attribution-ShareAlike

- Production function. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Production_function. License: CC BY-SA: Attribution-ShareAlike

- Boundless. Provided by: Boundless Learning. Located at: www.boundless.com//economics/...uct-of-capital. License: CC BY-SA: Attribution-ShareAlike

- Production function. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Production%20function. License: CC BY-SA: Attribution-ShareAlike

- Capital Equilibrium. Provided by: Wikimedia. Located at: commons.wikimedia.org/wiki/File:Capital_Equilibrium.jpg. License: CC BY: Attribution

- 208346048. Provided by: mizan128 Wikispace. Located at: http://mizan128.wikispaces.com/file/....ppt/208346048. License: CC BY-SA: Attribution-ShareAlike

- Solow residual. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Solow_residual. License: CC BY-SA: Attribution-ShareAlike

- Total factor productivity. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Total_f...r_productivity. License: CC BY-SA: Attribution-ShareAlike

- Productivity. Provided by: ba5551 Wikispace. Located at: http://ba5551.wikispaces.com/Productivity. License: CC BY-SA: Attribution-ShareAlike

- Productivity. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Productivity. License: CC BY-SA: Attribution-ShareAlike

- Total factor productivity. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Total%2...20productivity. License: CC BY-SA: Attribution-ShareAlike

- Capital Equilibrium. Provided by: Wikimedia. Located at: commons.wikimedia.org/wiki/File:Capital_Equilibrium.jpg. License: CC BY: Attribution

- Angulus-Produktionshalle. Provided by: Wikimedia. Located at: commons.wikimedia.org/wiki/Fi...tionshalle.jpg. License: Public Domain: No Known Copyright

- Transportation Economics/Production. Provided by: Wikibooks. Located at: en.wikibooks.org/wiki/Transpo...mand_Functions. License: CC BY-SA: Attribution-ShareAlike

- Factors of production. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Factors_of_production. License: CC BY-SA: Attribution-ShareAlike

- input. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/input. License: CC BY-SA: Attribution-ShareAlike

- assembly line. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/assembly_line. License: CC BY-SA: Attribution-ShareAlike

- Capital Equilibrium. Provided by: Wikimedia. Located at: commons.wikimedia.org/wiki/File:Capital_Equilibrium.jpg. License: CC BY: Attribution

- Angulus-Produktionshalle. Provided by: Wikimedia. Located at: commons.wikimedia.org/wiki/Fi...tionshalle.jpg. License: Public Domain: No Known Copyright

- Provided by: Wikimedia. Located at: http://upload.wikimedia.org/wikipedi..._expansion.svg. License: CC BY-SA: Attribution-ShareAlike