16.3: Progressive, Proportional, and Regressive Taxes

- Last updated

- Save as PDF

- Page ID

- 3535

- Boundless

- Boundless

Comparing Marginal and Average Tax Rates

Taxes can be evaluated based on an average impact or a marginal impact and can be categorized as progressive, regressive, or proportional.

learning objectives

- Calculate the average tax rate and marginal tax rate

Computing Taxes

Average and marginal tax rate

An average tax rate is the ratio of the total amount of taxes paid, T, to the total tax base, P, (taxable income or spending), expressed as a percentage. If a company pays different rates on the first $100,000 in earning than the next $100,000, it will sum up the total tax paid and divide it by $200,000 to calculate the average tax rate.

T/P = average tax rate

The marginal tax rate is sometimes defined as the tax rate that applies to the last (or next) unit of the tax base (taxable income or spending), it is in effect, the tax percentage on the highest dollar earned. For example, if a company pays 5% tax on its first $100,000 earned, and 10% on the next $100,000, the marginal tax rate of earning the $101,000th dollar is 10%.

Broadly, the marginal tax rate equals the change in taxes, divided by the change in tax base, expressed as a percentage.

\[\dfrac{\text{change in T}}{\text{change in P}} = \text{marginal tax rate}\]

Types of Taxes

Progressive tax

A progressive tax is a tax in which the tax rate increases as the taxable base amount increases. The term “progressive” describes a distribution effect on income or expenditure, referring to the way the rate progresses from low to high, where the average tax rate is less than the marginal tax rate. The term can be applied to individual taxes or to a tax system as a whole; a year, multi-year, or lifetime. Progressive taxes are imposed in an attempt to reduce the tax incidence of people with a lower ability-to-pay, as such taxes shift the incidence increasingly to those with a higher ability-to-pay. The opposite of a progressive tax is a regressive tax, where the relative tax rate or burden increases as an individual’s ability to pay it decreases.

Progressive taxation: Graph demonstrates a progressive tax distribution on income that becomes regressive for top earners.

Regressive tax

A regressive tax is a tax imposed in such a manner that the average tax rate decreases as the amount subject to taxation increases. “Regressive” describes a distribution effect on income or expenditure, referring to the way the rate progresses from high to low, where the average tax rate exceeds the marginal tax rate. In terms of individual income and wealth, a regressive tax imposes a greater burden (relative to resources) on the poor than on the rich — there is an inverse relationship between the tax rate and the taxpayer’s ability to pay as measured by assets, consumption, or income.

Proportional tax

A proportional tax is a tax imposed so that the tax rate is fixed, with no change as the taxable base amount increases or decreases. The amount of the tax is in proportion to the amount subject to taxation. “Proportional” describes a distribution effect on income or expenditure, referring to the way the rate remains consistent (does not progress from “low to high” or “high to low” as income or consumption changes), where the marginal tax rate is equal to the average tax rate.

Tax Incidence, Efficiency, and Fairness

Tax incidence is the analysis of the effect of a particular tax on the distribution of economic welfare.

learning objectives

- Identify who bears the tax burden in various scenarios

In economics, tax incidence is the analysis of the effect of a particular tax on the distribution of economic welfare. Tax incidence is said to “fall” upon the group that ultimately bears the burden of, or ultimately has to pay, the tax. The key concept is that the tax incidence or tax burden does not depend on where the revenue is collected, but on the price elasticity of demand and price elasticity of supply.

Tax incidence does not consider the concept of tax efficiency or the excess burden of taxation, also known as the distortionary cost or deadweight loss of taxation, is one of the economic losses that society suffers as the result of a tax. For example, United States Social Security payroll taxes are paid half by the employee and half by the employer. However, some economists think that the worker is bearing almost the entire burden of the tax because the employer passes the tax on in the form of lower wages. The tax incidence is thus said to fall on the employee and due to the need for workers for a particular job, the tax burden also falls, in this case, on the worker.

Example of Tax Incidence

Imagine a $1 tax on every barrel of apples an apple farmer produces. If the product (apples) is price inelastic to the consumer (whereby if price rose, a small demand loss would be accounted for by the extra revenue), the farmer is able to pass the entire tax on to consumers of apples by raising the price by $1. In this example, consumers bear the entire burden of the tax; the tax incidence falls on consumers. On the other hand, if the apple farmer is unable to raise prices because the product is price elastic (if prices rose, more demand would be lost than extra revenue gained), the farmer has to bear the burden of the tax or face decreased revenues: the tax incidence falls on the farmer. If the apple farmer can raise prices by an amount less than $1, then consumers and the farmer are sharing the tax burden. When the tax incidence falls on the farmer, this burden will typically flow back to owners of the relevant factors of production, including agricultural land and employee wages.

Shared tax incidence: The imposition of a tax can result in a reduction to both consumer and producer surplus relative to the pre-tax scenario.

Where the tax incidence falls depends (in the short run) on the price elasticity of demand and price elasticity of supply. Tax incidence falls mostly upon the group that responds least to price (the group that has the most inelastic price-quantity curve). If the demand curve is inelastic relative to the supply curve the tax will be disproportionately borne by the buyer rather than the seller. If the demand curve is elastic relative to the supply curve, the tax will be borne disproportionately by the seller.

Tax efficiency

In the example provided, the tax burden falls disproportionately on the party exhibiting relatively more inelasticity in the situation. This characteristic results in a reduction of the ability of the party to participate in the market to the level of willingness that would have been present in the absence of the tax. The loss is conceptually defined as a loss of surplus and the loss of surplus is characterized as deadweight loss. Policy makers evaluate the surplus and deadweight loss in relation to the imposition of a tax in order to better evaluate the efficiency of a tax or the distortion that the imposed tax causes on the attainment of market equilibrium.

Policymakers must consider the predicted tax incidence when creating them. If taxes fall on an unintended party, it may not achieve its intended objective and may not be fair.

Tax Incidence and Elasticity

Tax incidence or tax burden does not depend on where the revenue is collected, but on the price elasticity of demand and price elasticity of supply.

learning objectives

- Explain how elasticity influences the relative tax burden between suppliers and consumers (demand).

Tax incidence refers to who ultimately pays the tax, the producer or consumer, and the resulting societal effect. Tax incidence is said to “fall” upon the group that ultimately bears the burden of, or ultimately has to pay, the tax. The key concept is that the tax incidence or tax burden does not depend on where the revenue is collected, but on the price elasticity of demand and price elasticity of supply.

Inelastic Supply, Elastic Demand

If a producer is inelastic, he will produce the same quantity no matter what the price. If the consumer is elastic, the consumer is very sensitive to price. A small increase in price leads to a large drop in the quantity demanded.

Tax: Inelastic supply and elastic demand: In a scenario with inelastic supply and elastic demand, the tax burden falls disproportionately on suppliers.

The imposition of the tax causes the market price to increase from P without tax to P with tax and the quantity demanded to fall from Q without tax to Q with tax. Because the consumer is elastic, the quantity change is significant. Because the producer is inelastic, the price does not change much. The producer is unable to pass the tax onto the consumer and the tax incidence falls on the producer. In this example, the tax is collected from the producer and the producer bears the tax burden.

Comparable Elasticities

In most markets, elasticities of supply and demand are fairly similar in the short-run, as a result the burden of an imposed tax is shared between the two groups albeit in varying proportions.

Tax: Similar elasticity for supply and demand: When a tax is imposed in a scenario where demand and supply exhibit similar elasticities, the tax burden is shared.

In general, the tax burden will be greater for the group exhibiting the greater relative inelasticity.

Trading off Equity and Efficiency

Taxes may be considered equitable if they are administered in accordance with the definition of either horizontal or vertical equity.

learning objectives

- Explain tax equity in relation to the progressive, proportional, and regressive nature of taxes.

In public finance, horizontal equity conforms to the concept that people with a similar ability to pay taxes should pay the same or similar amounts. It is related to tax neutrality or the idea that the tax system should not discriminate between similar things or people, or unduly distort behavior. Vertical equity usually refers to the idea that people with a greater ability to pay taxes should pay more.

Horizontal Equity, Vertical Equity, and Taxes

Income taxes are a laddered progressive tax where income tax rates are set in income bands or ranges. Each tax rate corresponds to a particular income range; income above a tax range is subject to a higher tax rate that corresponds to a higher income range and income below a specific range is subject to a lower tax rate, similarly identified with a lower income range. Within any given income range, the tax rate is the same.

The income range conforms with the idea that the individuals included within it are similar with respect to their ability to pay. The range can be identified as conforming to the concept of horizontal equity. Vertical equity follows from the laddering of income tax to progressively higher rates. The laddering of income taxes conforms to the underlying definition of vertical equity, as those who have a greater ability to pay tax, pay a higher proportion of their income.

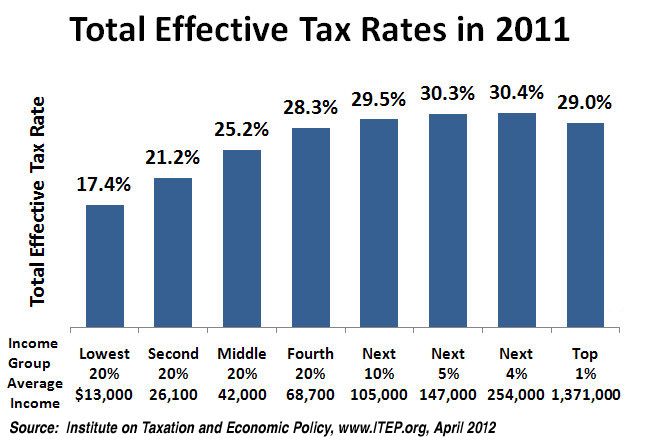

Proportional taxes, conform to horizontal equity. By definition proportional taxes are levied in proportion to income. However, income taxes are only proportional within specific income ranges. At the highest income tax rate, income taxes can become regressive, since high earners are only subject to a constant albeit highest rate on their income. For example, income from $500,000 and above will be subject to the same rate, making the overall tax burden as a proportion of income higher for the individuals on the starting point of the range.

Income tax: Income tax is a progressive tax that assumes a regressive nature at the highest tax rate.

Tax efficiency and tax equity

The purpose of a progressive tax system is to increase the tax burden to those most able to pay. However, some policy makers believe that progressive taxation is an overall inefficiency within the tax structure. These individuals and groups support a flat tax or proportional tax instead. Their argument for a tax modification is related to the view that increasing the tax rate in conjunction with income creates a disincentive to individuals to earn more and is, as a result, punitive to those that achieve income related success. The net result from this reasoning is that progressive taxation results in lower GDP than would have resulted in a proportional tax regime, also referred to as a loss of economic efficiency.

Key Points

- An average tax rate is the ratio of the total amount of taxes paid, T, to the total tax base, P, whereas the marginal tax rate equals the change in taxes, divided by the change in tax base.

- A proportional tax is a tax imposed so that the tax rate is fixed, with no change as the taxable base amount increases or decreases. The average tax rate equals the marginal tax rate.

- A regressive tax is a tax imposed in such a manner that the tax rate decreases as the amount subject to taxation increases. The average tax rate is higher than the marginal tax rate.

- A progressive tax is a tax in which the tax rate increases as the taxable base amount increases. The average tax rate is lower than the marginal tax rate.

- Tax incidence or tax burden does not depend on where the revenue is collected, but on the price elasticity of demand and price elasticity of supply.

- Tax incidence falls mostly upon the group that responds least to price (the group that has the most inelastic price-quantity curve).

- If the demand curve is inelastic relative to the supply curve the tax will be disproportionately borne by the buyer rather than the seller. If the demand curve is elastic relative to the supply curve, the tax will be born disproportionately by the seller.

- If a producer (consumer) is inelastic, it will produce (demand) the same quantity no matter what the price.

- If the producer (consumer) is elastic, the producer (consumer) is very sensitive to price.

- The sensitivity between quantity and price will determine the proportion of tax incidence between producers and consumers of a good.

- Horizontal equity conforms to the concept that people with a similar ability to pay taxes should pay the same or similar amounts.

- Vertical equity usually refers to the idea that people with a greater ability to pay taxes should pay more.

- Income taxes are incorporate both horizontal and vertical equity via a progressive tax mechanism. Sales taxes are regressive and are considered inequitable.

Key Terms

- average tax rate: The ratio of the amount of taxes paid to the tax base (taxable income or spending).

- marginal tax rate: The tax rate that applies to the last unit of currency of the tax base (taxable income or spending), and is often applied to the change in one’s tax obligation as income rises.

- elastic: Sensitive to changes in price.

- tax: Money paid to the government other than for transaction-specific goods and services.

- inelastic: Not sensitive to changes in price.

- inelasticity: The insensitivity of changes in a quantity with respect to changes in another quantity.

- elasticity: The sensitivity of changes in a quantity with respect to changes in another quantity.

- progressive tax: A tax by which the rate increases as the taxable base amount increases.

- income tax: A tax levied on earned and unearned income, net of allowed deductions.

- equity: Justice, impartiality or fairness.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- Progressive tax. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Progressive_tax. License: CC BY-SA: Attribution-ShareAlike

- Tax rate. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Tax_rate. License: CC BY-SA: Attribution-ShareAlike

- Proportional tax. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Proportional_tax. License: CC BY-SA: Attribution-ShareAlike

- Regressive tax. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Regressive_tax. License: CC BY-SA: Attribution-ShareAlike

- marginal tax rate. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/marginal%20tax%20rate. License: CC BY-SA: Attribution-ShareAlike

- average tax rate. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/average%20tax%20rate. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...Rates_2011.jpg. License: CC BY: Attribution

- Tax incidence. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Tax_incidence. License: CC BY-SA: Attribution-ShareAlike

- Excess burden of taxation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Excess_burden_of_taxation. License: CC BY-SA: Attribution-ShareAlike

- elastic. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/elastic. License: CC BY-SA: Attribution-ShareAlike

- tax. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/tax. License: CC BY-SA: Attribution-ShareAlike

- inelastic. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/inelastic. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...Rates_2011.jpg. License: CC BY: Attribution

- Tax incidence. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Tax_incidence. License: CC BY-SA: Attribution-ShareAlike

- elasticity. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/elasticity. License: CC BY-SA: Attribution-ShareAlike

- inelasticity. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/inelasticity. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/Wikipedia/commons/thumb/5/55/Total_Effective_Tax_Rates_2011.jpg/220px-Total_Effective_Tax_Rates_2011.jpg. License: CC BY: Attribution

- Progressive tax. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Progres...ve_progression. License: CC BY-SA: Attribution-ShareAlike

- Equity (economics). Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Equity_(economics). License: CC BY-SA: Attribution-ShareAlike

- equity. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/equity. License: CC BY-SA: Attribution-ShareAlike

- progressive tax. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/progressive%20tax. License: CC BY-SA: Attribution-ShareAlike

- income tax. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/income_tax. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/Wikipedia/commons/thumb/5/55/Total_Effective_Tax_Rates_2011.jpg/220px-Total_Effective_Tax_Rates_2011.jpg. License: CC BY: Attribution

- Provided by: Wikimedia. Located at: upload.wikimedia.org/Wikipedia/commons/thumb/5/55/Total_Effective_Tax_Rates_2011.jpg/220px-Total_Effective_Tax_Rates_2011.jpg. License: CC BY-SA: Attribution-ShareAlike