24.2: Introducing Aggregate Demand and Aggregate Supply

- Last updated

- Save as PDF

- Page ID

- 4497

- Boundless

- Boundless

Explaining Fluctuations in Output

In the short run, output fluctuates with shifts in either aggregate supply or aggregate demand; in the long run, only aggregate supply affects output.

learning objectives

- Differentiate between short-run and long-run effects of nominal fluctuations

Economic Output

In economics, output is the quantity of goods and services produced in a given time period. The level of output is determined by both the aggregate supply and aggregate demand within an economy. National output is what makes a country rich, not large amounts of money. For this reason, understanding the fluctuations in economic output is critical for long term growth. There are a series of factors that influence fluctuations in economic output including increases in growth and inputs in factors of production. Anything that causes labor, capital, or efficiency to go up or down results in fluctuations in economic output.

Aggregate Supply and Aggregate Demand

Aggregate supply is the total amount of goods and services that firms are willing to sell at a given price in an economy. The aggregate demand is the total amounts of goods and services that will be purchased at all possible price levels.

In a standard AS-AD model, the output (Y) is the x-axis and price (P) is the y-axis. Aggregate supply and aggregate demand are graphed together to determine equilibrium. The equilibrium is the point where supply and demand meet to determine the output of a good or service.

Short-run vs. Long-run Fluctuations

Supply and demand may fluctuate for a number of reasons, and this in turn may affect the level of output. There are noticeable differences between short-run and long-run fluctuations in output.

Over the short-run, an outward shift in the aggregate supply curve would result in increased output and lower prices. An outward shift in the aggregate demand curve would also increase output and raise prices. Short-run nominal fluctuations result in a change in the output level. In the short-run an increase in money will increase production due to a shift in the aggregate supply. More goods are produced because the output is increased and more goods are bought because of the lower prices.

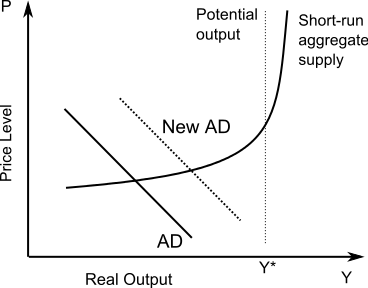

AS-AD Model: This AS-AD model shows how the aggregate supply and aggregate demand are graphed to show economic output. The AD curve shifts to the right which increases output and price.

In the long-run, the aggregate supply curve and aggregate demand curve are only affected by capital, labor, and technology. Everything in the economy is assumed to be optimal. The aggregate supply curve is vertical which reflects economists’ belief that changes in aggregate demand only temporarily change the economy’s total output. In the long-run an increase in money will do nothing for output, but it will increase prices.

Classical Theory

Classical theory, the first modern school of economic thought, reoriented economics from individual interests to national interests.

learning objectives

- Identify the assumptions fundamental to classical economics

Classical Theory

Classical theory was the first modern school of economic thought. It began in 1776 and ended around 1870 with the beginning of neoclassical economics. Notable classical economists include Adam Smith, Jean-Baptiste Say, David Ricardo, Thomas Malthus, and John Stuart Mill. During the period in which classical theory emerged, society was undergoing many changes. The primary economic question involved how a society could be organized around a system in which every individual sought his own monetary gain. It was not possible for a society to grow as a unit unless its members were committed to working together. Classical theory reoriented economics away from individual interests to national interests. Classical economics focuses on the growth in the wealth of nations and promotes policies that create national expansion. During this time period, theorists developed the theory of value or price which allowed for further analysis of markets and wealth. It analyzed and explained the price of goods and services in addition to the exchange value.

Adam Smith: Adam Smith was one of the individuals who helped establish classical economic theory.

Classical Theory Assumptions

Classical theory was developed according to specific economic assumptions:

- Self-regulating markets: classical theorists believed that free markets regulate themselves when they are free of any intervention. Adam Smith referred to the market’s ability to self-regulate as the “invisible hand” because markets move towards their natural equilibrium without outside intervention.

- Flexible prices: classical economics assumes that prices are flexible for goods and wages. They also assumed that money only affects price and wage levels.

- Supply creates its own demand: based on Say’s Law, classical theorists believed that supply creates its own demand. Production will generate an income enough to purchase all of the output produced. Classical economics assumes that there will be a net saving or spending of cash or financial instruments.

- Equality of savings and investment: classical theory assumes that flexible interest rates will always maintain equilibrium.

- Calculating real GDP: classical theorists determined that the real GDP can be calculated without knowing the money supply or inflation rate.

- Real and Nominal Variables: classical economists stated that real and nominal variables can be analyzed separately.

Keynesian Theory

Keynesian economics states that in the short-run, economic output is substantially influenced by aggregate demand.

learning objectives

- Differentiate “Chicago School” or “Austrian School” economists from “Keynesian School” economists

Keynesian Theory

In economics, the Keynesian theory was first introduced by British economist John Maynard Keynes in his book The General Theory of Employment, Interest, and Money which was published in 1936 during the Great Depression. Keynesian economics states that in the short-run, especially during recessions, economic output is substantially influenced by aggregate demand (the total spending in the economy). According to the Keynesian theory, aggregate demand does not necessarily equal the productive capacity of the economy. Keynesian theorists believe that aggregate demand is influenced by a series of factors and responds unexpectedly. The shift in aggregate demand impacts production, employment, and inflation in the economy.

John Maynard Keynes: John Maynard Keynes introduced Keynesian theory in his book, The General Theory of Employment, Interest, and Money.

Economic Thought

At the time that Keynesian theory was developed, mainstream economic thought believed that the economy existed in a state of general equilibrium. The belief was that the economy naturally consumes whatever it produces because the act of producing creates enough income in the economy for that consumption to take place.

Keynesian theory has certain characteristic beliefs:

- Unemployment is the result of structural inadequacies within the economic system. It is not a product of laziness as believed previously.

- During a recession, the economy may not return naturally to full employment. The government must step in and utilize government spending to stimulate economic growth. A lack of investment in goods and services causes the economy to operate below its potential output and growth rate.

- An active stabilization policy is needed to reduce the amplitude of the business cycle. Keynesian economists believed that aggregate demand for goods and services not meeting the supply was one of the most serious economic problems.

- Excessive saving, saving beyond investment, is a serious problem that encouraged recession and even depression.

- Cutting wages will not cure a recession.

- Overcoming an economic depression requires economic stimulus, which could be achieved by cutting interest rates and increasing the level of government investment.

Schools of Economic Thought

It is important to understand the stances of the various school of economic thought. Although the beliefs of each school vary, all of the schools of economic thought have contributed to economic theory is some way.

The Keynesian School of economic thought emphasized the need for government intervention in order to stabilize and stimulate the economy during a recession or depression. In contrast, the Chicago School of economic thought focused price theory, rational expectations, and free market policies with little government intervention. The Austrian School of economic thought focused on the belief that all economic phenomena are caused by the subjective choices of individuals. Unlike other schools, the Austrian school focused on individual actions instead of society as a whole.

Key Points

- In the short run, output is determined by both the aggregate supply and aggregate demand within an economy. Anything that causes labor, capital, or efficiency to go up or down results in fluctuations in economic output.

- Aggregate supply and aggregate demand are graphed together to determine equilibrium. The equilibrium is the point where supply and demand meet.

- According to Hume, in the short-run, and increase in the money supply will lead to an increase in production.

- According to Hume, in the long-run, an increase in the money supply will do nothing.

- When classical theory emerged, society was undergoing many changes. The primary economic question involved how a society could be organized around a system in which every individual sought his own monetary gain.

- Classical economics focuses on the growth in the wealth of nations and promotes policies that create national economic expansion.

- Classical theory assumptions include the beliefs that markets self-regulate, prices are flexible for goods and wages, supply creates its own demand, and there is equality between savings and investments.

Key Terms

- nominal: Without adjustment to remove the effects of inflation (in contrast to real).

- economic output: The productivity of a country or region measured by the value of goods and services produced.

- self-regulating: Describing something capable of controlling itself.

- Keynesian Economics: A school of thought that is characterized by a belief in active government intervention in an economy and the use of monetary policy to promote growth and stability.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SHARED PREVIOUSLY

- Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- Output (economics). Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Output_(economics). License: CC BY-SA: Attribution-ShareAlike

- Aggregate supply. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Aggregate_supply. License: CC BY-SA: Attribution-ShareAlike

- Aggregate demand. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Aggregate_demand. License: CC BY-SA: Attribution-ShareAlike

- nominal. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/nominal. License: CC BY-SA: Attribution-ShareAlike

- economic output. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/economic_output. License: CC BY-SA: Attribution-ShareAlike

- AS AD graph. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:AS_+_AD_graph.svg. License: CC BY-SA: Attribution-ShareAlike

- Classical economics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Classical_economics. License: CC BY-SA: Attribution-ShareAlike

- self-regulating. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/self-regulating. License: CC BY-SA: Attribution-ShareAlike

- AS AD graph. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:AS_+_AD_graph.svg. License: CC BY-SA: Attribution-ShareAlike

- Smith. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Smith.gif. License: Public Domain: No Known Copyright

- Chicago school of economics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Chicago...s%23Discussion. License: CC BY-SA: Attribution-ShareAlike

- Keynesian economics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Keynesian_economics. License: CC BY-SA: Attribution-ShareAlike

- Austrian School. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Austrian_School. License: CC BY-SA: Attribution-ShareAlike

- Keynesianism. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Keynesianism. License: CC BY-SA: Attribution-ShareAlike

- Keynesian Economics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Keynesian%20Economics. License: CC BY-SA: Attribution-ShareAlike

- AS AD graph. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:AS_+_AD_graph.svg. License: CC BY-SA: Attribution-ShareAlike

- Smith. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Smith.gif. License: Public Domain: No Known Copyright

- John Maynard Keynes. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Jo...ard_Keynes.jpg. License: Public Domain: No Known Copyright