25.1: Major Theories in Macroeconomics

- Last updated

- Save as PDF

- Page ID

- 4507

- Boundless

- Boundless

Keynesian Theory

Keynesian theory posits that aggregate demand will not always meet the supply produced.

Learning objectives

- Explain the main tenets of Keynesian economics

Historical Background

John Maynard Keynes published a book in 1936 called The General Theory of Employment, Interest, and Money, laying the groundwork for his legacy of the Keynesian Theory of Economics. It was an interesting time for economic speculation considering the dramatic adverse effect of the Great Depression. Keynes’s concepts played a role in public economic policy under Roosevelt as well as during World War II, becoming the dominant perspective in Europe following the war.

John Maynard Keynes: John Maynard Keynes came to fame after publishing his economic theories during the Great Depression.

At the time, the primary school of economic thought was that of the classical economists (which is still a popular school of thought today). The central tenet of the classical argument says that supply can always create demand, and that surpluses will result in price reductions to the point of consumption. Put simply, people have infinite needs and the market will self-correct to the aggregate demands and available resources. This implies a hands-of public policy where markets are capable of taking care of themselves.

Keynes positioned his argument in contrast to this idea, stating that markets are imperfect and will not always self correct. Keynes theorized that natural inefficiencies in the market will see goods that are not met with demand. This wasted capital can result in market losses, unemployment, and market inefficiency (this was called ‘general glut’ in the classical model, when aggregate demand does not meet supply). Keynes insisted that markets do need moderate governmental intervention through fiscal policy (government investment in infrastructure) and monetary policy ( interest rates ).

Main Tenets

With this overview in mind, Keynesian Theory generally observes the following concepts:

- Unemployment: Under the classical model, unemployment is often attributed to high and rigid real wages. Keynes argues there is more complexity than that, specifically that societies are highly resistant to wage cuts and furthermore that reducing wages would pose a great threat to an economy. Specifically, cutting wages reduces spending and may result in a downwards spiral.

- Excessive Saving: Keynes’s concept here is somewhat complicated, but in short Keynes notes excessive saving as a threat and prospective cause of economic decline. This is because excessive saving leads to reduced investment and reduced spending, which drives down demand and the potential for consumption. This can be another spiraling issue, as money not being exchanged is actively reducing prospective employment, revenues, and future investments.

- Fiscal Policy: The key concept in fiscal policy for Keynes is ‘counter-cyclical’ fiscal policy, which is the expectation that governments can reduce the negative effects of the natural business cycle. This is, generally, achieved through deficit spending in recessions and suppression of inflation during boom times. Simply put, the government should try to curb the extremes of economic fluctuation through informed fiscal policy.

- The Multiplier Effect: This idea has in many ways already been implied in the atom, but inversely. Consider the unemployment and excessive savings problems, and how they stand to lead to spiraling decline. The other side of that coin is that positive economic situations can spiral upwards. Take for example a government investment in transportation, putting money in the pockets of various individuals who build trains and tracks. These individuals will spend that extra capital, putting money in the hands of other business (and this will continue). This is called the multiplier effect.

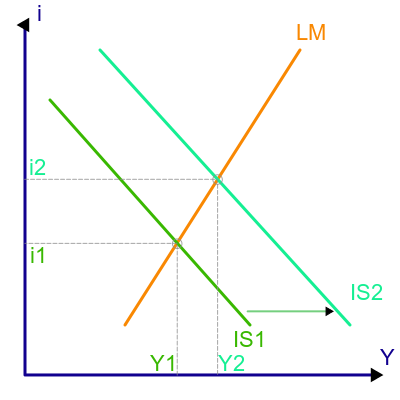

- IS-LM: While the IS-LM Model is a complicated byproduct of Keynesian economics, it can be summarized as the relationship between interest rates (y-axis) and the real economic output (x-axis). This is done through analyzing the invest-saving relationship (IS) in contrast to the liquidity preference and money supply relationship (LM), generating an equilibrium where certain interest rates and outputs will be generated.

While Keynesian Theory has been expounded upon significantly over the years, the important takeaway here is that aggregate demand (and thus the amount of supply consumed) is not a perfect system. Instead, demand is affected by various external forces that can create an inefficient market which will in turn affect employment, production, and inflation.

IS-LM Model: In this figure, the IS (Interest – Saving) curve is shifted outward in a way that raises both interest rates (i) and the ‘real’ economy (Y). The implication is that interest rates affect investment levels, and that these investment levels in turn affect the overall economy.

Monetarist

Monetarism focuses on the macroeconomic effects of the supply of money and the role of central banking on an economic system.

Learning objectives

- Explain the main tenets of Monetarism

Background

In the rise of monetarism as an ideology, two specific economists were critical contributors. Clark Warburton, in 1945, has been identified as the first thinker to draft an empirically sound argument in favor of monetarism. This was taken more mainstream by Milton Friedman in 1956 in a restatement of the quantity theory of money. The basic premise these two economists were putting forward is that the supply of money and the role of central banking play a critical role in macroeconomics.

The generation of this theory takes into account a combination of Keynesian monetary perspectives and Friedman’s pursuit of price stability. Keynes postulated a demand-driven model for currency; a perspective on printed money that was not beholden to the ‘ gold standard ‘ (or basing economic value off of rare metal). Instead, the amount of money in a given environment should be determined by monetary rules. Friedman originally put forward the idea of a ‘k-percent rule,’ which weighed a variety of economic indicators to determine the appropriate money supply.

Evidence

Theoretically, the idea is actually quite straight-forward. When the money supply is expanded, individuals will be induced to higher spending. In turn, when the money supply retracted, individuals would limit their budgetary spending accordingly. This would theoretically provide some control over aggregate demand (which is one of the primary areas of disagreement between Keynesian and classical economists).

Monetarism began to deviate more from Keynesian economics however in the 70’s and 80’s, as active implementation and historical reflection began to generate more evidence for the monetarist view. In 1979 for example, Jimmy Carter appointed Paul Volcker as Chief of the Federal Reserve, who in turn utilized the monetarist perspective to control inflation. He eventually created a price stability, providing evidence that the theory was sound. In addition, Milton Friedman and Ann Schwartz analyzed the Great Depression in the context of monetarism as well, identifying a shortage of the money supply as a critical component of the recession.

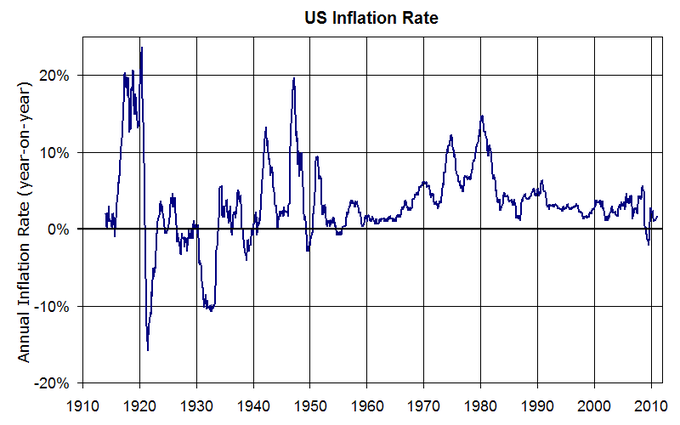

The 1980s were an interesting transitional period for this perspective, as early in the decade (1980-1983) monetary policies controlling capital were attributed to substantial reductions in inflation (14% to 3%)(see ). However, unemployment and the rise of the use of credit are quoted as two alternatives to money supply control being the primary influence of the boom that followed 1983.

U.S. Inflation Rates: The inflation rates over time in the U.S. represent some of the evidence put forward by monetarist economists, stating that governmental control of the money supply allows for some control over inflation.

Counter Arguments

As these counter arguments in the 1980s began to arise, critics of monetarism became more mainstream. Of the current monetarism critics, the Austrian school of thought is likely the most well-known. The Austrian school of economic thought perceives monetarism as somewhat narrow-minded, not effectively taking into account the subjectivity involved in valuing capital. That is to say that monetarism seems to assume an objective value of capital in an economy, and the subsequent implications on the supply and demand.

Other criticisms revolve around international investment, trade liberalization, and central bank policy. This can be summarized as the effects of globalization, and the interdependence of markets (and consequently currencies). To manipulate money supply there will inherently be effects on other currencies as a result of relativity. This is particularly important in regards to the U.S. currency, which is considered a standard in international markets. Controlling supply and altering value may have effects on a variety of internal economic variables, but it will also have unintended consequences on external variables.

Austrian

Austrian economic thought is about methodological individualism, or the idea that people will act in meaningful ways which can be analyzed.

Learning objectives

- Explain the main tenets of Austrian economics

Background

The Austrian school of economics originated in the 19th century in Vienna, Austria. While there were a variety of famous economists attributed to the early foundations and later expansions of the Austrian economic perspective, Carl Menger, Friedrich von Weiser, and Eugen von Bohm-Bawerk are widely recognized as critical early pioneers. The general perspective of Austrian economic thought is methodological individualism, or the recognition that people will act in meaningful ways which can be analyzed for trends.

Central Tenets

The Austrian school of thought provided enormous value to the economic climate, both as a foundation for future economics and as a deliberate counterpoint to more quantitative analysis. Of the most important ideologies, the following central tenets are:

- Opportunity Cost: This is a concept you are likely already familiar with, and one of the most important ideas in all of business and economics. Essentially, the price of a good must also incorporate the value sacrificed of the next best alternative. Basically each choice a consumer or business makes intrinsically has the cost of not being able to make an alternative choice.

- Capital and Interest: Largely in response to Karl Marx’s labor theories, Austrian economist Bohm-Bawerk identified the building blocks of interest rates and profit are supply and demand alongside time preference. In short, present consumption is more valuable than future consumption (the time value of money).

- Inflation: The idea that prices and wages must rise as a result of increased money supply is inflation (note: this is different that price inflation). Simply put, more money in the system without a higher demand for that money will drive down the relative value of each dollar.

- Business Cycles: The Austrian business cycle theory (ABCT) is the simple observation that the issuance of credit (by banks) creates economic fluctuations that tend to be cyclical (see ). In simple terms, banks will lend out money at rates lower than the risk in which that money will be used. So when businesses fail more often than they succeed, thus losing interest as opposed to accruing it, will struggle to repay their debts. When the banks call in those debts the business cannot pay, creating negative business cycles.

- The Organizing Power of Markets: The idea of this concept is that no one person knows what the appropriate price of a good should be. Instead, markets naturally generate incentives to identify optimal price points. This negates the ideas of socialism common at the time, as communist systems will be unable to identify the appropriate exchange value of each good.

As you can see from the above points, this school of economics is largely about making qualitative observations of the markets. These observations are absolutely critical in understanding the theoretical landscape, but difficult to enact in practice.

Criticisms

Austrian economists are often criticized for ignoring arithmetic or statistical ways to measure and analyze economics. Indeed, Austrian economists do not often place much weight on concepts such as econometrics, experimental economics, and aggregate macroeconomic analysis. In this sense, the Austrian school of thought is something of an outsider relative to other perspectives (i.e. classical, Keynesian, etc.).

Paul Krugman criticized Austrian economics as lacking explicit models of analysis, or essentially a lack of clarity in their approach. This results in inadvertent blind spots. This is a sensible criticism in many ways, as the fundamental idea behind this economic theory is that it is driven by individuals and individuals are not always rational (indeed, they are quite often irrational). As a result of this, Austrian economics often rests on the integration of social sciences (psychology, sociology, etc.) to explain preferences and consumer behavior, which is often counter-intuitive. As a result, it is very difficult to accurately measure and provide tangible proof of the efficacy of Austrian models.

Alternative Views

Neoclassical and neo-Keynesian ideas can be coupled and referred to as the neoclassical synthesis, combining alternative views in economics.

Learning objectives

- Summarize neoclassical and Neo-Keynesian economics

Background

The history of different economic schools of thought have consistently generated evolving theories of economics as new data and new perspectives are taken into consideration. The two most well-known schools, classical economics and Keynesian economics, have been adapting to incorporate new information and ideas from one another as well as lesser known schools of economics (Chicago, Austrian, etc.). These different perspectives have motivated economists to generate the neoclassical and neo-Keynesian perspectives. The neoclassical perspective, in conjunction with Keynesian ideas, is referred to as the neoclassical synthesis, which is largely considered the ‘mainstream’ economic perspective.

Neoclassical

In approaching Neoclassical economics, it is most important to keep in mind the following three principles:

- People have rational preferences in the context of options or outcomes that can be identified and associated with a given value (usually monetary). In short, people make smart choices regarding how they spend their money.

- Individuals maximize utility and firms maximize profit. People will try to get the most from their money while corporations will try to invest their time and assets to capture the highest margin.

- People act independently based upon comprehensive and relevant information. People are influenced by rational forces (mostly information and logic), and will make the best personal purchasing decisions based upon this.

A brief timeline of classical to neoclassical perspectives would begin with thought processes put forward by Adam Smith and David Ricardo (alongside many others). The basic idea is that aggregate demand will adjust to supply, and that value theory and distribution will reflect this rational, cost of production model. The next phase was the observation that consumer goods demonstrated a relative value based on utility, which could deviate from consumer to consumer. The final phase, and most central to the advent of the neoclassical perspective, is the introduction of marginalism. Marginalism notes that economic participants make decisions based on marginal utility or margins. For example, a company hiring a new employee will not think of the fixed value of that employee, but instead the marginal value of adding that employee (usually in regards to profitability).

Neo-Keynesian

Neo-Keynesian economics is often confused with ‘New Keynesian’ economics (which attempts to provide microeconomic foundation to Keynesian views, particularly in light of stagflation in the 1970s). Neo-Keynesian economics is actually the formalization and coordination of Keynes’s writings by a number of other economists (most notably John Hicks, Franco Modigliani, and Paul Samuelson). Much of the conceptual value is captured in the previous atoms on Keynesian views, but the substantial value of a few neo-Keynesian ideas is worth reiterating:

- IS/LM Model: This model was put forward by John Hicks in order to capture the inherent relationship between investment and savings (IS) relative to liquidity and the overall money supply (LM) (see ). The implications of this graph pertain to the static representation of monetary policy and the effects on an economic system.

- Phillips Curve: Another important model following Keynes’s publications is the Phillips Curve, put forward by William Phillips in 1958. The idea here was also largely Keynesian, revolving around the relationship between inflation and unemployment (see ).This implies a trade off between inflation rates and the creation of employment, which governments could consider in policy making. Stagflation (economic stagnation and inflation simultaneously) created issues with this however, necessitating New Keynesian ideas (as discussed briefly above).

Synthesis

When learning about these economic perspectives, it is important to understand the value they add to one another and the overall efficacy of all economic theory. Economists are often the product of multiple schools of thought, and don’t fit neatly into one school or another.

Key Points

- John Maynard Keynes published a book in 1936 called The General Theory of Employment, Interest, and Money, laying the groundwork for his legacy of the Keynesian Theory of Economics.

- Keynes positioned his argument in contrast to this idea, stating that markets are imperfect and will not always self correct.

- Keynes believed that wage reductions in recessions and excessive savings were potential threats to an economy.

- Keynesian theory expects fiscal policy to offset business cycles (employ counter-cyclical strategies).

- Clark Warburton, in 1945, has been identified as the first thinker to draft an empirically sound argument in favor of monetarism. This was taken more mainstream by Milton Friedman in 1956.

- More money in the system results in higher spending and vice verse. This would theoretically provide some control over aggregate demand.

- Historical implementation of monetarism demonstrated some correlation with control over inflation rates and increased economic performance. This could have been a result of other factors however.

- The Austrian school of economic thought perceives monetarism as somewhat narrow-minded, not effectively taking into account the subjectivity involved in valuing capital.

- Due to the globalization of the economy, monetarism may have a negative impact on external economies. This is particularly true of the U.S., whose capital is an international standard.

- The Austrian school of economics is one of the oldest economic perspectives, originating in the 19th century in Vienna.

- Austrian economics is attributed for the identification of opportunity cost, capital and interest, inflation, business cycles and the organizing power of markets.

- Austrian economists do not often place much weight on concepts such as econometrics, experimental economics, and aggregate macroeconomic analysis. In this sense, the Austrian school of thought is something of an outsider relative to other perspectives (i.e. classical, Keynesian, etc. ).

- Paul Krugman criticized Austrian economics as lacking explicit models of analysis, or essentially a lack of clarity in their approach. This results in inadvertent blind spots.

- The history of different economic schools of thought have consistently generated evolving theories of economics as new data and new perspectives are taken into consideration.

- The neoclassical perspective in conjunction with Keynesian ideas is referred to as the neoclassical synthesis, which is largely considered the ‘mainstream’ economic perspective.

- A critical difference between classical and neoclassical perspectives is the introduction of marginalism. Marginalism notes that economic participants make decisions based on marginal utility or margins.

- Neo- Keynesian economics is the formalization and coordination of Keynes’s writings by a number of other economists (most notably John Hicks, Franco Modigliani and Paul Samuelson).

- The important to understand that these economic perspectives add value to one another and the overall efficacy of all economic theory.

Key Terms

- fiscal policy: Government policy that attempts to influence the direction of the economy through changes in government spending or taxes.

- monetary policy: The process of controlling the supply of money in an economy, often conducted by central banks.

- Keynesian: Of or pertaining to an economic theory based on the ideas of John Maynard Keynes, as put forward in his book The General Theory of Employment, Interest, and Money.

- Monetarism: The doctrine that economic systems are controlled by variations in the supply of money.

- gold standard: A monetary system where the value of circulating money is linked to the value of gold.

- Opportunity cost: The cost of any activity measured in terms of the value of the next best alternative forgone (that is not chosen).

- time value of money: The time value of money is the principle that a certain currency amount of money today has a different buying power (value) than the same currency amount of money in the future.

- stagflation: Inflation accompanied by stagnant growth, unemployment or recession.

- static: Unchanging; that cannot or does not change.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SHARED PREVIOUSLY

- Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- fiscal policy. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/fiscal_policy. License: CC BY-SA: Attribution-ShareAlike

- IS/LM model. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/IS/LM_model. License: CC BY-SA: Attribution-ShareAlike

- Keynesian economics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Keynesian_economics. License: CC BY-SA: Attribution-ShareAlike

- Macroeconomics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Macroeconomics. License: CC BY-SA: Attribution-ShareAlike

- Keynesian. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Keynesian. License: CC BY-SA: Attribution-ShareAlike

- monetary policy. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/monetary_policy. License: CC BY-SA: Attribution-ShareAlike

- John Maynard Keynes. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Jo...ard_Keynes.jpg. License: Public Domain: No Known Copyright

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi.../b/b9/Islm.svg. License: CC BY-SA: Attribution-ShareAlike

- gold standard. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/gold_standard. License: CC BY-SA: Attribution-ShareAlike

- Monetarism. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Monetarism. License: CC BY-SA: Attribution-ShareAlike

- Macroeconomics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Macroeconomics. License: CC BY-SA: Attribution-ShareAlike

- Monetarism. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Monetarism. License: CC BY-SA: Attribution-ShareAlike

- John Maynard Keynes. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Jo...ard_Keynes.jpg. License: Public Domain: No Known Copyright

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi.../b/b9/Islm.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._Inflation.png. License: CC BY-SA: Attribution-ShareAlike

- Macroeconomics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Macroeconomics. License: CC BY-SA: Attribution-ShareAlike

- Austrian School. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Austrian_School. License: CC BY-SA: Attribution-ShareAlike

- time value of money. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/time%20...e%20of%20money. License: CC BY-SA: Attribution-ShareAlike

- Opportunity cost. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Opportunity+cost. License: CC BY-SA: Attribution-ShareAlike

- John Maynard Keynes. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Jo...ard_Keynes.jpg. License: Public Domain: No Known Copyright

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi.../b/b9/Islm.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._Inflation.png. License: CC BY-SA: Attribution-ShareAlike

- Macroeconomics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Macroeconomics. License: CC BY-SA: Attribution-ShareAlike

- New Keynesian. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/New_Keynesian. License: CC BY-SA: Attribution-ShareAlike

- New classical macroeconomics. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/New_cla...macroeconomics. License: CC BY-SA: Attribution-ShareAlike

- Chicago school (economics). Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Chicago...ol_(economics). License: CC BY-SA: Attribution-ShareAlike

- stagflation. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/stagflation. License: CC BY-SA: Attribution-ShareAlike

- static. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/static. License: CC BY-SA: Attribution-ShareAlike

- John Maynard Keynes. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Jo...ard_Keynes.jpg. License: Public Domain: No Known Copyright

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi.../b/b9/Islm.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._Inflation.png. License: CC BY-SA: Attribution-ShareAlike