33.1: Fundamentals of Banking Crises

- Last updated

- Save as PDF

- Page ID

- 4775

- Boundless

- Boundless

Causes of Banking Crises

Banking crises can be caused by inadequate governmental oversight, bank runs, positive feedback loops in the market and contagion.

learning objectives

- Describe some common causes of a banking crisis, Explain a bank run

In light of recent market and banking failures, the economic analysis of banking crises both historically and presently is a constant source of interest and speculation. Banking crises are when there are widespread bank runs: an abnormal number depositors try to withdraw their deposits because they don’t trust that the bank will have the deposits for withdrawal in the future.

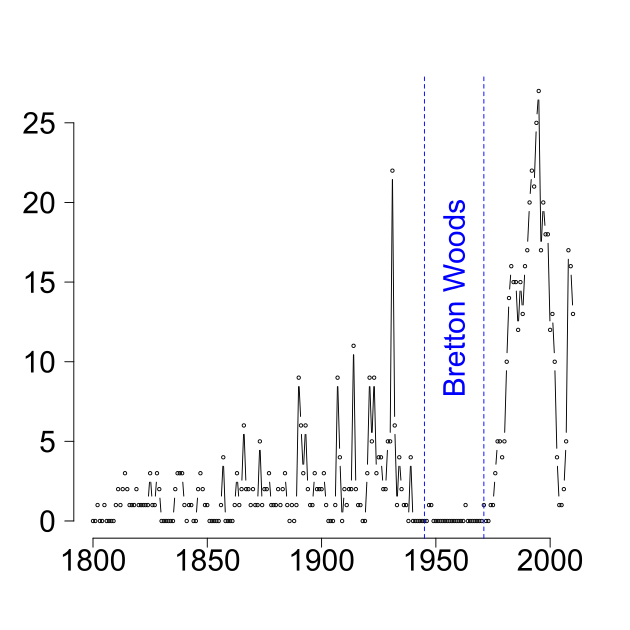

Banking crises are not a new economic phenomenon, and similarly are not the only source of financial crises. Over the course of the past two centuries there have been a surprisingly large number of financial crises, as demonstrated in the attached figure. In understanding banking crises over time, it is useful to identify the causes in context with historic examples of banking collapses.

Financial Crises Globally since 1800: This chart is an interesting take on the relatively consistent frequency in which financial crises occur across the globe. It is interesting to note both the efficacy of Bretton Woods alongside the increasing risk of financial collapse in modern times.

Causes of Banking Crises

Banks can fail for several different reasons:

- Bank Run: A bank occurs when many people try to withdraw their deposits at the same time. As much of the capital in a bank is tied up in investments, the bank’s liquidity will sometimes fail to meet the consumer demand. This can quickly induce panic in the public, driving up withdrawals as everyone tries to get their money back from a system that they are increasingly skeptical of. This leads to a bank panic which can result in a systemic banking crisis, which simply means that all of the free capital in the banking system is withdrawn.

- Stock Market Positive Feedback Loops: One particularly interesting cause of banking disasters is a similar positive feedback loop effect in the stock markets, which was a much more dynamic factor in more recent banking crises (i.e. 2007-2009 sub-prime mortgage disaster). John Maynard Keynes once compared financial markets to a beauty contest, where investors are merely trying to pick what is attractive to other investors. There is a profound truth to this, creating an interdependent and potentially self-fulfilling investment thought process. This can create dramatic rises and falls (bubbles and crashes), which in turn can throw banks with poorly designed leverage into huge losses.

- Regulatory Failure: One of the simplest ways in which bank crises can occur is a lack of governmental oversight. As noted above, banks often leverage themselves to capture gains despite extremely high risks (such as over-dependence on derivatives).

- Contagion: Due to globalization and international interdependence, the failure of one economy can create something of a domino effect. In 2008, when the U.S. economy collapses, the reduced buying power and economic output from that economy dramatically damaged all economies dependent upon it (which includes most of the world). This is called contagion.

The Great Depression

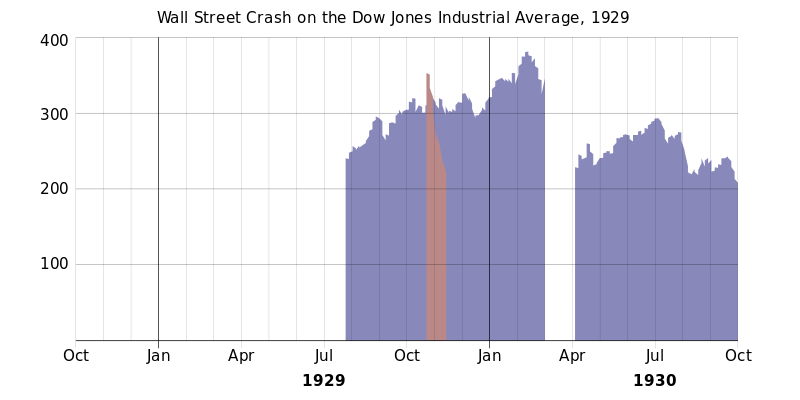

The Great Depression highlights how bank runs caused a banking crisis, which ultimately became a global economic crisis.The Great Depression in 1929 resulted from a variety of complex inputs, but the turning point came in the form of a mass stock market crash (Black Tuesday) and subsequent bank runs. As fear began to grip consumers across the United States, people became protective of their assets (including their cash). This caused a large number of people to the banks to withdraw, which in turn motivated others to go to the banks and get their capital out also. Since banks lend out some of their deposits, they did not have enough cash on hand to meet the immediate withdrawal requests (they became illiquid) and therefore went bankrupt. Within a few weeks this resulted in a systemic banking crisis.

1929 Stock Market Crash: As the market falls, investors create a positive feedback loop and self-fulfilling prophecy due to a lack of confidence that drives it down even further.

Consequences of Banking Crises

Banking crises have a range of short-term and long-term repercussions, domestically and globally, that reduce economic output and growth.

learning objectives

- Explain consequences of banking crises on the broader economy

Banking crises have a dramatic negative effect on the overall economy, often resulting in an eventual financial and economic crisis in a given economic system. Banking crises have a range of short-term and long-term repercussions, domestically and globally, that underline the severe repercussions of irresponsible banking practices, poor governmental regulation, and bank runs. The most useful way to frame the consequences of bank crises is by observing the critical role banks play in economic growth, primarily through investment and lending.

Domestic Consequences

Within a given system, banking failures create a range of negative repercussions from an economic perspective. Banks coordinate and economy’s savings and investment: the act of pooling money to capture higher returns for everyone while simultaneously funding business dependent upon leveraging debt and equity. With this in mind, a banking crises can have a variety of averse individual and economic consequences within the system.

First and foremost, investment suffers. When banks lack liquidity to invest, businesses that depend upon loans struggle to raise the capital required to execute upon their operations. When these businesses cannot produce the capital required to operate optimally, sales decline and prices rise. The overall economic performance of any debt-dependent industries becomes less dependable, driving down consumer and investor confidence while reduce overall economic output. Banks also perform more poorly, due to the fact that they have less capital to invest and returns to acquire.

This drives down the overall economic system, both in the short term and the long term, as companies struggle to succeed. The fall in liquidity and investment drives up unemployment, drives down governmental tax revenues and reduces investor and consumer confidence (damaging equity markets, which in turn limits businesses access to capital). There is a distinctive cyclical nature to these adverse effects, as each are interconnected in a way that creates a domino effect across the domestic economic system.

Global Consequences

While these domestic consequences are expected and, in many ways, intuitive, the global dependency upon foreign trade in modern markets has exacerbated these effects. Imports and exports play an increasingly large role in the health of most developed economies, and as a result the relative well-being of trade partners plays an increasingly critical role in the success of domestic economies.

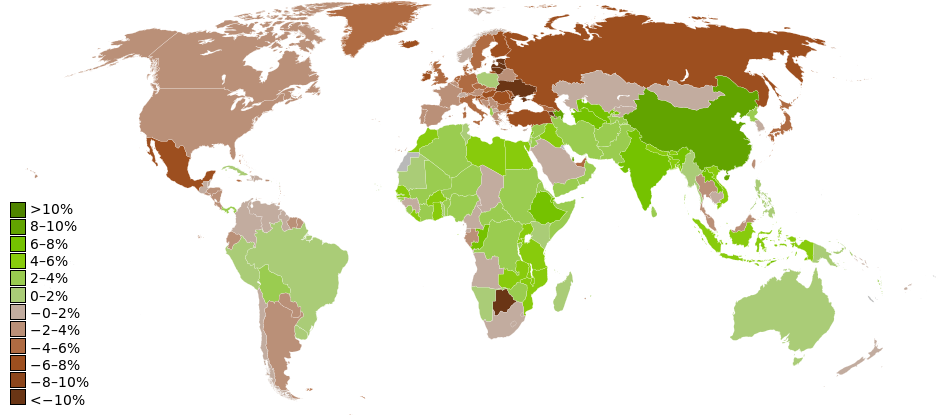

A good example of this is to look at the way in which the U.S. (and to some extent, European) banking disasters in 2008 and 2009 led to a complete global financial meltdown, destroying economies not involved in the irresponsible investing practices executed by banks in these specific regions. identifies the critical importance of economic well-being in trading partners, as the U.S. banking and financial crises spread rapidly (within the course of just one year) across a substantial portion of the globe (though there are certainly other factors that contributed to the financial crisis and its consequences). The domestic reduction of capital for businesses, income for consumers and tax revenue for governments ultimately results in a reduction of trade and economic activity for other economies.

2009 GDP Growth Rates: This figure shows the growth in GDP for world economies in 2009. The slow and negative growth demonstrates all of the economic losses that resulted in part from the U.S. financial crisis, highlighting the dependency of global economies.

Key Points

- A bank occurs when many people try to withdraw their deposits at the same time. As much of the capital in a bank is tied up in investments, the bank’s liquidity will sometimes fail to meet the consumer demand.

- Due to the mass interdependence of economies across the globe, a banking crisis in one nation is likely to dramatically affect other international economies.

- The Great Depression in 1929 resulted from a variety of complex inputs, but the turning point came in the form of a mass stock market crash (Black Tuesday) and subsequent bank runs.

- Irresponsible and unethical leveraging in these assets by the banks, and mass governmental failure to listen to economists predicting this over the past decade, caused the 2008 stock market crash and subsequent depression.

- Irresponsible and unethical leveraging in these assets by the banks, and mass governmental failure to listen to economists predicting this over the past decade, caused the 2008 stock market crash and subsequent depression.

- Banks play a critical role in economic growth, primarily through investment and lending.

- After a banking crisis, investment suffers. When banks lack liquidity to invest, growing business depending upon loans struggle to raise the capital required to execute upon their operations.

- The fall in liquidity and investment, in turn, drives up unemployment, drives down governmental tax revenues and reduces investor and consumer confidence.

- Imports and exports play an increasingly large role in the health of most developed economies, and as a result, the relative well-being of trade partners plays an increasingly critical role in the success of domestic economies.

Key Terms

- Bank Run: A large number of customers withdraw their deposits from a financial institution at the same time due to a loss of confidence in the banks.

- leverage: The use of borrowed funds with a contractually determined return to increase the ability of a business to invest and earn an expected higher return, but usually at high risk.

- Economic crisis: A period of economic slowdown characterised by declining productivity and devaluing of financial institutions often due to reckless and unsustainable money lending.

- liquidity: The degree to which an asset can be easily converted into cash.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SHARED PREVIOUSLY

- Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- leverage. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/leverage. License: CC BY-SA: Attribution-ShareAlike

- Financial crisis. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financial_crisis. License: CC BY-SA: Attribution-ShareAlike

- Bank run. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Bank_run. License: CC BY-SA: Attribution-ShareAlike

- Bretton Woods system. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Bretton_Woods_system. License: CC BY-SA: Attribution-ShareAlike

- Bank Run. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Bank%20Run. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...kingCrises.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...rash_graph.svg. License: CC BY-SA: Attribution-ShareAlike

- Financial crisis. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financial_crisis. License: CC BY-SA: Attribution-ShareAlike

- Bank run. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Bank_run. License: CC BY-SA: Attribution-ShareAlike

- Bretton Woods system. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Bretton_Woods_system. License: CC BY-SA: Attribution-ShareAlike

- Financial crisis of 2007u201308. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financi...007%E2%80%9308. License: CC BY-SA: Attribution-ShareAlike

- Economic crisis. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Economic+crisis. License: CC BY-SA: Attribution-ShareAlike

- liquidity. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/liquidity. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/Wikipedia/commons/2/27/BankingCrises.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/Wikipedia/commons/c/c5/1929_wall_street_crash_graph.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...eal_Growth.svg. License: CC BY-SA: Attribution-ShareAlike