Monetary policy is the process by which a monetary authority controls the money supply, often to produce stable prices and low unemployment.

learning objectives

Justify expansionary and contractionary monetary policy.

Monetary policy is the process by which the monetary authority of a country, which could be a government agency or a central bank, controls the supply of money, often targeting a rate of interest for the purpose of promoting economic growth and stability. The official goals usually include relatively stable prices and low unemployment.

Monetary policy is referred to as either being expansionary or contractionary, where an expansionary policy increases the total supply of money in the economy more rapidly than usual, and contractionary policy expands the money supply more slowly than usual or even shrinks it. Expansionary policy is traditionally used to try to combat unemployment in a recession by easing credit to entice businesses into expanding. Contractionary policy is intended to slow inflation in order to avoid the resulting distortions and deterioration of asset values, or to cool an overheating economy. Monetary policy differs from fiscal policy, which refers to taxation, government spending, and associated borrowing.

Expansionary Monetary Policy

A monetary authority will typically pursue expansionary monetary policy when there is an output gap – that is, a country is producing output at a lower level than its potential output. Without a policy intervention the output gap may correct itself, if falling wages and prices shift the short-run aggregate supply curve to the right until the economy returns to the long-run equilibrium. Alternatively, the monetary authority could intervene in order to increase aggregate demand and close the output gap. Expansionary monetary policy consists of the tools that a central bank uses to achieve this increase in aggregate demand.

In practice, this means that a monetary authority will use the tools at its disposal in order to increase the money supply and decrease interest rates. Since interest rates represent the price of money, lower interest rates will cause the quantity of money demanded to increase, stimulating investment and spending. In addition, lower interest rates make a currency worth less in the currency exchange market. This reduces the demand for and increases the supply of dollars in the currency market, reducing the exchange rate (in foreign currency per dollar). A lower exchange rate makes a country’s goods relatively more affordable for the rest of the world, stimulating exports and further increasing output.

Contractionary Monetary Policy

By contrast, a monetary authority will pursue a contractionary monetary policy when it considers inflation a threat. Suppose, for example, that high short-run aggregate demand creates an equilibrium in which prices are higher than in the long-run equilibrium. This will cause high levels of inflation. In response, the monetary authority may reduce the money supply and thereby raise the interest rate. Investment falls as the interest rate rises. The higher interest rate also increases the demand for dollars as foreign investors shift their investments to the United States. Likewise, the supply of dollars declines. Consumers in the United States purchase domestic interest-bearing assets rather than purchasing assets abroad, taking advantage of the higher domestic interest rate. Increased demand and decreased supply cause an increase in the exchange rate, which boots imports while reducing exports. Thus, contractionary monetary policy causes aggregate demand to fall, thereby reducing the rate of inflation..

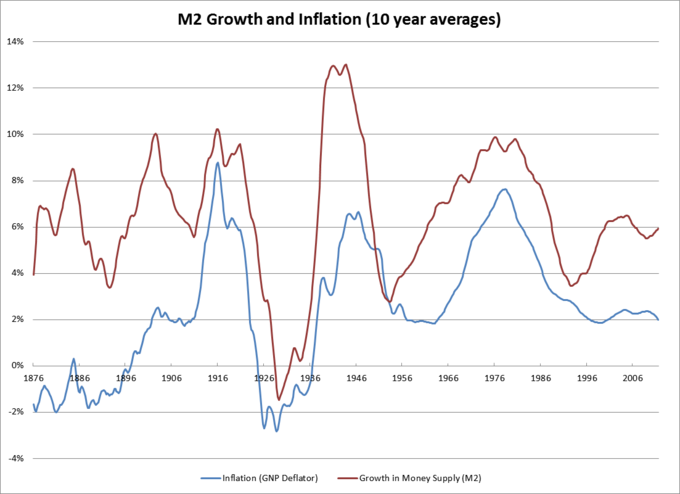

Money Supply and Inflation: The graph shows the relationship between the money supply and the inflation rate. By controlling the money supply, monetary authorities hope to influence the rate of inflation.

The Creation of the Federal Reserve

The Federal Reserve was created to promote financial stability, provide regulation and banking services, and conduct monetary policy.

learning objectives

Explain monetary policy as the main function of a central bank

The Federal Reserve Act of 1913

Until 1913, the United States did not have a true central bank. The US suffered through a number of financial crises that eventually drove Congress to create the US central bank, the Federal Reserve (the Fed), through the Federal Reserve Act of 1913.

The Act established three key objectives for monetary policy: maximum employment, stable prices, and moderate long-term interest rates. The first two objectives are sometimes referred to as the Federal Reserve’s dual mandate and are the most emphasized of the three.

Over the years, the Fed has expanded its duties to include conducting monetary policy, supervising and regulating banking institutions, maintaining the stability of the financial system, and providing financial services.

How the Fed Conducts Monetary Policy

The Fed has three main policy tools: setting reserve requirements, operating the discount window and other credit facilities, and conducting open-market operations.

Reserve Requirements

Commercial banks are required to hold a certain proportion of their deposits in reserves and not lend them out. This proportion is called the reserve requirement and is controlled by the Fed. By changing the reserve requirement, the Fed can impact the amount of money available for lending, and by extension, spending and investment.

Discount Window

Commercial banks are required to have a certain amount of reserves on hand at the end of each day. If they are going to come up short, they must borrow from other banks or the Fed. The Fed extends these loans through the discount window and charges what is called the discount rate. The discount rate is set by the Fed, and is important because it radiates throughout the economy: if it becomes more expensive to borrow at the discount window, interest rates will rise and borrowing will become more expensive economy-wide. In this way, the Fed can use the discount window to affect interest rates and the money supply.

Increasing the Money Supply: The diagram shows how the central bank can increase the money supply by lending money through the discount window or purchasing bonds (open market operations).

Open-Market Operations

The government borrows by issuing bonds. Recall that the interest rate that the government pays is determined by the price of the bond: the higher the price of the bond, the lower the interest rate. The Fed can affect the interest rate by conducting open-market operations (OMOs) in which it buys or sells bonds. Buying or selling bonds changes the demand or supply of the bonds, and therefore their price. By extension, OMOs change the interest rate, hopefully to achieve one of the Fed’s monetary goals.

Structure of the Federal Reserve

The Federal Reserve System (The Fed) was designed in order to maintain the central bank’s independence and promote decentralized power.

learning objectives

Recall the structure of the Federal Reserve System of the United States

The Federal Reserve (the Fed) was designed to be independent of the Congress and the government. The idea justification for independence is that it allows the Fed to operate without being put under political pressure to take actions that may not be in the best long-term economic interest of the country.

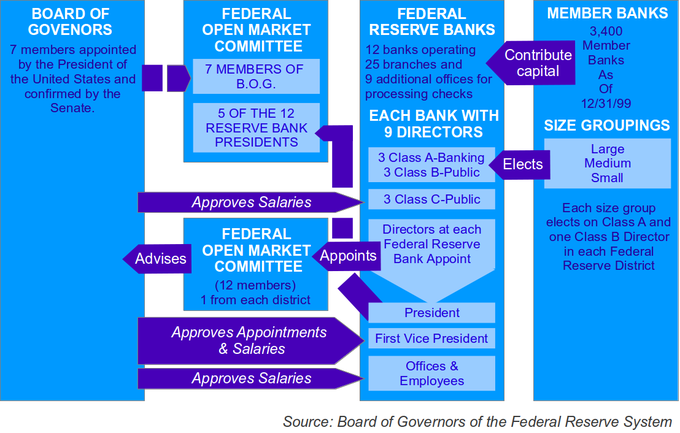

The Federal Reserve System is composed of five parts:

Structure of the Federal Reserve: The diagram shows the relationship between the different organizations that compose the Federal Reserve System

The presidentially appointed Board of Governors (or Federal Reserve Board), an independent federal government agency located in Washington, D.C. Each governor serves a 14 year term. As of February 2014, the Chair of the Board of Governors is Janet Yellen, who succeeded Ben Bernanke.

The Federal Open Market Committee (FOMC), composed of the seven members of the Federal Reserve Board and five of the 12 Federal Reserve Bank presidents, which oversees open market operations, the principal tool of U.S. monetary policy.

Twelve regional Federal Reserve Banks located in major cities throughout the nation, which divide the nation into twelve Federal Reserve districts. The Federal Reserve Banks act as fiscal agents for the U.S. Treasury, and each has its own nine-member board of directors.

Numerous other private U.S. member banks, which own required amounts of non-transferable stock in their regional Federal Reserve Banks.

Various advisory councils.

The Fed can be thought of as having both private and public organization characteristics, though it considers itself to be private. On one hand, the Fed works toward achieving public goals such as moderate inflation and low unemployment. It does not exist to make money. On the other hand, it is, by design, separate from the government. It operates independently, and is not subject to political pressures directly as is Congress or the President.

The Federal Open Market Committee and the Role of the Fed

The Federal Open Market Committee is responsible for conducting open market operations in order to achieve a target interest rate.

learning objectives

Describe the structure and operations of the Federal Open Market Committee (FOMC)

One of the primary tools used by the Federal Reserve (the Fed) to conduct monetary policy is open market operations: the buying and selling of federal government bonds in order to influence the money supply and interest rate. These operations are the primary responsibility of the Federal Open Market Committee (FOMC). The FOMC is a twelve-person committee composed of the seven members of the Board of Governors, plus a rotating combination of five presidents of the Federal Reserve Regional Banks. The president of the New York regional bank is always a member of the FOMC; the other four seats are filled by four of the other eleven bank presidents.

When conducting monetary policy the Fed sets a target for the federal funds rate, which it attempts to achieve using open market operations. To lower the federal funds rate, for example, the Fed buys securities on the open market, increasing the money supply. In order to raise the federal funds rate, on the other hand, the Fed sells securities and thereby reduces the money supply.

Open Market Operations

As mentioned previously, the aim of open market operations is to manipulate the short term interest rate and the total money supply. This involves meeting the demand for money at the target interest rate by buying and selling government securities or other financial instruments. Monetary targets, such as inflation, interest rates, or exchange rates, are used to guide this implementation.

Imagine the Fed is targeting a federal funds rate of 3%. If there is an increased demand for money and the Fed takes no action, interest rates will rise. This may produce unintended contractionary effects in the economy. Instead, the FOMC responds to an increase in the demand for money by going to the open market to buy a financial asset, such as government bonds, foreign currency, or gold. To pay for these assets, the Fed transfers bank reserves to the seller’s bank and the seller’s account is credited. Since the bank now has more reserves than it had before, it can lend out more money and the money supply increases. Thus, the increase in demand for money is met with an increase in supply, and the interest rate remains unchanged.

Conversely, if the central bank sells its financial assets on the open market, reserves are transferred from the buyer’s bank back to the Fed. This reduces the amount of money that a bank may loan out and the total money supply falls. The process works because the central bank has the authority to bring money in and out of existence. They are the only point in the whole system with the unlimited ability to produce money.

FOMC Meeting: The members of the FOMC meet eight times a year in order to vote on current monetary policies.

The Federal Reserve and the Financial Crisis of 2008

The Fed responded to the financial crisis with conventional open market operations and unconventional credit facilities and bailouts.

learning objectives

Summarize the monetary policy tools used by the Federal Reserve in response to the financial crisis of 2008.

In late 2007, the bursting of the U.S. housing bubble triggered the worst financial crisis since the Great Depression of the 1930s. It resulted in the threat of total collapse of large financial institutions, the bailout of banks by national governments, and downturns in stock markets around the world. The crisis caused the failure of businesses, huge declines in consumer wealth, and a downturn in economic activity that lead to the 2008-2012 global recession.

The Federal Reserve ‘s response to the 2008 crisis saw the use of both conventional and new monetary tools in order to stabilize the economy, support market liquidity, and encourage economic activity. Conventional monetary policy suggests that in an economic downturn, a central bank should conduct open market operations in order to increase the money supply and lower interest rates. Lower interest rates stimulate loans, spending, and investment and help an economy escape from recession. Further, this type of financial crisis meant that banks’ assets were suddenly worth far less; open market operations can ensure that these banks have the liquidity they need to carry out their financial activities.

Conventional Monetary Tools

The Federal Reserve (the Fed) did engage in these types of conventional operations in 2007 and 2008, cutting the target federal funds rate and the discount rate seven times. Normally, a low federal funds rate would encourage banks to borrow money in order to lend it out to firms and individuals, stimulating the economy, but in the aftermath of the financial crisis the Fed was unable to lower interest rates enough to successfully induce banks to make loans. One reason why traditional monetary policies failed is due to the zero lower bound and the low levels of inflation that accompanied the crisis.

The zero lower bound refers to the fact that the central bank cannot push nominal interest rates below 0%. This is because any creditor can do better by keeping their money in cash than by loaning it out at an interest rate below 0%. When inflation is high, however, central banks may be able to push the real interest rate below 0%. Recall that the nominal interest rate is the sum of the real interest rate and the expected inflation rate. If the nominal interest rate is 1% and inflation is 3%, the real interest rate is -2%. However, following the crisis, the U.S. experienced very low levels of inflation, and cutting the federal funds rate failed to provide enough economic stimulus to get the country out of the recession.

Unconventional Monetary Tools

Unable to create interest rates low enough to encourage banks to resume lending money, the Fed turned to other, untried policy tools to encourage economic activity. To deal with the shrinking credit markets, the Fed created a selection of new credit facilities. The Primary Dealer Credit Facility (PDCF) allows the banks that normally handle open market operations on behalf of the Fed to apply for overnight loans. The Term Asset-Backed Securities Loan Facility uses the primary dealers to give companies access to loans based on asset-backed securities, such as those related to credit card or small business debt. These new credit facilities were created based on the hope that increasing liquidity in the market would induce firms and consumers to borrow and spend.

The Fed also provided targeted assistance to bail out large financial institutions that would have otherwise collapsed. During the crisis, housing prices fell and the number of foreclosures increased dramatically. Investors, banks, and other financial institutions came under pressure as their mortgage-based assets lost value. The Fed provided credit to these institutions in an attempt to mitigate the effect of falling asset prices and stem the crisis. This included bailouts of two housing finance firms – Fannie Mae and Freddie Mac – which had been established by the government in order to encourage home ownership and stimulate the housing market.

The Fed also provided billions of dollars of assistance to AIG, an insurance firm that had invested heavily in mortgage loans. Without the assistance the firm would have collapsed, possibly causing a chain reaction of failing financial institutions. The Fed determined that these consequences were too severe to be allowed – that is, that AIG was “too big to fail. ” Many argue that when the Fed provided this type of emergency aid, it encouraged banks to take even more extreme risks, safe in the knowledge that they would be bailed out if their investments failed. Others praise the Fed for avoiding an even deeper financial crisis.

Government Bails Out AIG With $85 Billion Loan: September 16, 2008: The Federal Reserve says the U.S. government has agreed to provide an $85 billion emergency loan to rescue the huge insurer AIG. The Fed says the U.S. Treasury Department is in full support of the decision.

The Structure and Function of Other Banks

While central banks share responsibility for monetary policy, their structures, methods, and primary goals differ across countries.

learning objectives

Summarize the structure of the ECB, the Bank of England, and the People’s Bank of China

The primary function of a central bank is to manage the nation’s money supply (monetary policy), through active duties such as managing interest rates, setting the reserve requirement, and acting as a lender of last resort to the banking sector during times of bank insolvency or financial crisis. Central banks usually also have supervisory powers, intended to prevent bank runs and to reduce the risk that commercial banks and other financial institutions engage in reckless or fraudulent behavior. Central banks in most developed nations are institutionally designed to be independent from political interference. However, the structure, tools, and primary goals of these banks differ between countries.

European Central Bank

The European Central Bank (ECB) is the central bank for the euro and administers the monetary policy of the Eurozone, which consists of 17 EU member states and is one of the largest currency areas in the world. The bank was established by the Treaty of Amsterdam in 1998, and is headquartered in Frankfurt, Germany. In contrast with the Federal Reserve, the ECB has the primary objective of maintaining price stability within the Eurozone, but is not charged with regulating unemployment or economic output.

In the U.S., liquidity is furnished to the economy primarily through the purchase of Treasury bonds by the Federal Reserve (the Fed), but the European system uses a different method. Instead, there are about 1,500 eligible banks that can bid for short term repurchase contracts, or “repos”. The banks borrow cash, and when the repo notes come due the participating banks bid again. Because the loans have a short duration, the ECB can adjust interest rates and money supply by varying the quantity of notes offered at auction.

The ECB has three decision-making bodies: the Executive Board, the Governing Council, and the General Council. The Executive Board is responsible for implementing monetary policy and the day-to-day running of the bank. The Governing Council makes decisions about what monetary policies to implement. The General Council deals with the transitional issues that come about as new countries adopt the euro.

The Bank of England

The Bank of England is the central bank of the United Kingdom and the model on which most modern central banks have been based. Established in 1694, it is the second oldest central bank in the world. It was established to act as the English Government’s banker, and was privately owned from its foundation in 1694 until it was nationalized in 1946. In 1998, it became an independent public organization, owned by the Treasury Solicitor on behalf of the government, with independence in setting monetary policy. The primary goals of the Bank of England are to maintain price stability and support the economic policies of the government.

Bank of England Charter: The illustration shows the sealing of the Bank of England Charter in 1694. The structure and function of the Bank of England served as a model for the central banks formed later.

The Monetary Policy Committee is responsible for formulating monetary policy and for setting interest rates in order to maintain a given inflation target. The recently-established Financial Policy Committee is responsible for regulating the UK’s financial sector in order to maintain financial stability.

The People’s Bank of China

The People’s Bank of China (PBC) is the central bank of the People’s Republic of China with the power to control monetary policy and regulate financial institutions in mainland China. The People’s Bank of China has the most financial assets of any single public finance institution. It is responsible for making and implementing monetary policy for safeguarding the overall financial stability and provision of financial services.

The PBC has nine regional branches, as well as many sub-branches and six overseas representative offices. It is divided into 18 functional departments that oversee such issues as monetary policy, financial stability, anti-money laundering, and legal affairs. The top management of the PBC is composed of the governor and a certain number of deputy governors. The PBC adopts a governor responsibility system under which the governor supervises the overall work of the PBC while the deputy governors provide assistance to the governor to fulfill his or her responsibility.

Key Points

Monetary policy is referred to as either being expansionary or contractionary, where an expansionary policy increases the money supply more rapidly than usual, and contractionary policy expands the money supply more slowly than usual.

Expansionary policy is traditionally used to try to combat unemployment by lowering interest rates. A monetary authority will typically pursue expansionary monetary policy when there is an output gap.

Contractionary policy is intended to slow inflation in order to avoid the resulting distortions and deterioration of asset values.

The Federal Reserve (the Fed) was originally created in response to a series of bank panics. While its policy goals were originally unclear, today the Fed has a dual mandate: to achieve maximum employment and stable prices.

The Fed has three main policy tools: setting reserve requirements, operating the discount window and other credit facilities, and conducting open-market operations.

The Fed sets the required ratio of reserves that banks must hold relative to their deposit liabilities.

The discount rate is the interest rate charged by the Fed when it lends reserves to banks.

The buying and selling of federal government bonds by the Fed are called open-market operations.

The Fed is a system of 12 regional banks, each of which has its own board of directors and rotating representative to the Federal Open Market Committee (FOMC).

The Fed is run by a Board of Governors, the head of which is the Chairperson.

The Federal Open Market Committee (FOMC) consists of the seven members of the Board of Governors and five rotating regional bank presidents. It is primarily responsible for buying and selling federal government bonds in order to conduct monetary policy.

Open market operations are the buying and selling of federal government bonds in order to influence the money supply and interest rate.

The Fed sets targets for the federal funds rate and then conducts operations to maintain that rate. To achieve a lower federal funds rate, for example, the Fed goes into the open market to buy securities and thus increase the money supply.

The FOMC decides on a target federal funds rate by looking at monetary targets such as inflation, interest rates, or exchange rates.

In late 2007, the bursting of the U.S. housing bubble triggered the worst financial crisis since the Great Depression of the 1930s.

The Fed cut the target federal funds rate and the discount lending rate seven times. Normally, a low federal funds rate would encourage banks to make loans, stimulating the economy, but this failed to work following the crisis.

Unable to rely on conventional tools, the Fed created a variety of credit facilities to provide liquidity to the economy.

The Fed also provided emergency funds to support financial institutions deemed “too big to fail”.

The European Central Bank controls interest rates through auctions rather than the bond market, and is responsible for maintaining price stability over all other goals.

The Bank of England is the second-oldest central bank in the world. Monetary policy is dictated by the Monetary Policy Committee, and recently the Financial Policy Committee was formed in order to regulate the UK’s financial sector.

The People’s Bank of China conducts monetary policy and is the largest central bank in the world.

Key Terms

output gap: The difference between an economy’s actual GDP and its long-run potential GDP

inflation: An increase in the general level of prices or in the cost of living.

central bank: The principal monetary authority of a country or monetary union; it normally regulates the supply of money, issues currency and controls interest rates.

reserve requirement: The minimum amount of deposits each commercial bank must hold (rather than lend out).

open market operations: An activity by a central bank to buy or sell government bonds on the open market. A central bank uses them as the primary means of implementing monetary policy.

monetary policy: The process by which the central bank, or monetary authority manages the supply of money, or trading in foreign exchange markets.

federal funds rate: The interest rate at which depository institutions actively trade balances held at the Federal Reserve with each other.

reserve: Banks’ holdings of deposits in accounts with their central bank.

discount rate: An interest rate that a central bank charges to depository institutions that borrow reserves from it.

liquidity: The degree to which an asset can be easily converted into cash.

Eurozone: Those European Union member states whose official currency is the euro.

price stability: A state of economy characterized by low inflation, and thus a stable value of money.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SHARED PREVIOUSLY

Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

Monetary policy. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Monetary_policy. License: CC BY-SA: Attribution-ShareAlike

output gap. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/output%20gap. License: CC BY-SA: Attribution-ShareAlike

inflation. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/inflation. License: CC BY-SA: Attribution-ShareAlike

M2andInflation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:M2andInflation.png. License: CC BY-SA: Attribution-ShareAlike

Federal Funds. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Federal_funds. License: Public Domain: No Known Copyright

Central banks. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Central_bank. License: CC BY-SA: Attribution-ShareAlike

Federal Reserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Federal_reserve. License: CC BY-SA: Attribution-ShareAlike

Discount Rate. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Discount_window. License: CC BY-SA: Attribution-ShareAlike

History of central banking in the united states. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/History..._United_States. License: CC BY-SA: Attribution-ShareAlike

reserve requirement. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/reserve%20requirement. License: CC BY-SA: Attribution-ShareAlike

central bank. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/central_bank. License: CC BY-SA: Attribution-ShareAlike

M2andInflation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:M2andInflation.png. License: CC BY-SA: Attribution-ShareAlike

Money-creation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Money-creation.gif. License: CC BY: Attribution

Structure of the Federal Reserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Structu...Reserve_System. License: CC BY-SA: Attribution-ShareAlike

Janet Yellen. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Janet_Yellen. License: CC BY-SA: Attribution-ShareAlike

Federal Reserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Federal_Reserve_System. License: CC BY-SA: Attribution-ShareAlike

Federal Reserve Board of Governors. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Board_o...Reserve_System. License: CC BY-SA: Attribution-ShareAlike

Central Bank. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Central...23Independence. License: CC BY-SA: Attribution-ShareAlike

open market operations. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/open%20...t%20operations. License: CC BY-SA: Attribution-ShareAlike

monetary policy. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/monetary_policy. License: CC BY-SA: Attribution-ShareAlike

M2andInflation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:M2andInflation.png. License: CC BY-SA: Attribution-ShareAlike

Money-creation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Money-creation.gif. License: CC BY: Attribution

FederalReserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...rve_System.png. License: Public Domain: No Known Copyright

Open market operations. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Open_market_operations. License: CC BY-SA: Attribution-ShareAlike

Boundless. Provided by: Boundless Learning. Located at: www.boundless.com//economics/...ral-funds-rate. License: CC BY-SA: Attribution-ShareAlike

reserve. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/reserve. License: CC BY-SA: Attribution-ShareAlike

M2andInflation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:M2andInflation.png. License: CC BY-SA: Attribution-ShareAlike

Money-creation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Money-creation.gif. License: CC BY: Attribution

FederalReserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...rve_System.png. License: Public Domain: No Known Copyright

Federal Open Market Committee Meeting. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...ee_Meeting.jpg. License: CC BY-SA: Attribution-ShareAlike

discount rate. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/discount_rate. License: CC BY-SA: Attribution-ShareAlike

Financial crisis of 2007-2010. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financi...s_of_2007-2010. License: CC BY-SA: Attribution-ShareAlike

open market operations. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/open%20...t%20operations. License: CC BY-SA: Attribution-ShareAlike

liquidity. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/liquidity. License: CC BY-SA: Attribution-ShareAlike

M2andInflation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:M2andInflation.png. License: CC BY-SA: Attribution-ShareAlike

Money-creation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Money-creation.gif. License: CC BY: Attribution

FederalReserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...rve_System.png. License: Public Domain: No Known Copyright

Federal Open Market Committee Meeting. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...ee_Meeting.jpg. License: CC BY-SA: Attribution-ShareAlike

Government Bails Out AIG With $85 Billion Loan. Located at: http://www.youtube.com/watch?v=B9vpSlctbDA. License: Public Domain: No Known Copyright. License Terms: Standard YouTube license

Bank of england. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Bank_of_england. License: CC BY-SA: Attribution-ShareAlike

People's Bank of China. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/People's_Bank_of_China. License: CC BY-SA: Attribution-ShareAlike

European Central Bank. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/European_Central_Bank. License: CC BY-SA: Attribution-ShareAlike

Central bank. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Central_bank. License: CC BY-SA: Attribution-ShareAlike

Eurozone. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Eurozone. License: CC BY-SA: Attribution-ShareAlike

monetary policy. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/monetary_policy. License: CC BY-SA: Attribution-ShareAlike

price stability. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/price_stability. License: CC BY-SA: Attribution-ShareAlike

M2andInflation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:M2andInflation.png. License: CC BY-SA: Attribution-ShareAlike

Money-creation. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Money-creation.gif. License: CC BY: Attribution

FederalReserve System. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...rve_System.png. License: Public Domain: No Known Copyright

Federal Open Market Committee Meeting. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Fe...ee_Meeting.jpg. License: CC BY-SA: Attribution-ShareAlike

Government Bails Out AIG With $85 Billion Loan. Located at: http://www.youtube.com/watch?v=B9vpSlctbDA. License: Public Domain: No Known Copyright. License Terms: Standard YouTube license

Bank of England Charter sealing 1694. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/File:Ba...aling_1694.jpg. License: Public Domain: No Known Copyright