Economic Growth as a Measuring Stick

Economic growth is measured as the increase in real gross domestic product (GDP) in the long-run, through higher resources or productivity.

learning OBJECTIVES

- Examine the components that cause economic growth

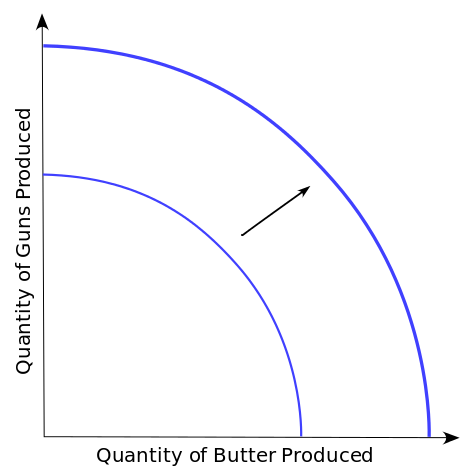

Economic growth can be defined as the increase in real gross domestic product (GDP) in the long-run, or as increased productivity or via an increase in the natural resources (inputs) that create output. It is important to note that real GDP adjusts for inflation, rather than looking at output in nominal dollars. Economic growth could also be described as an outward shift in the production-possibility frontier, allowing for the production of a higher quantity of goods.

Production-Possibility Frontier: This outward shift in the Production-Possibility frontier is indicative of economic growth within the economy it represents.

Standard Measures of Economic Growth

Measuring economic growth is reasonably straight-forward, primarily focusing on either increases in productivity or increases in the available production inputs in a given system. This increase in productivity is converted into a relative percent based upon previous years, and expressed as a growth or decline. For example, if a given economy is producing $1,000,000 in 1900 and 1,050,000 in 1901, the economic growth rate (or GDP growth) will be expressed as 5%. If inflation is calculated to be 3% between 1900 and 1901, real economic growth will equate to 2%.

Alternative Economic Growth Models

While measuring real GDP is useful in some ways, and considered a standard measure of economic growth, there is a great deal more complexity than is being captured (both quantitatively and qualitatively). An outline of the perspectives of economic growth over time include:

- Classical Growth Theory: Dating back to Adam Smith and the foundation of capitalism, classical growth theory uses the production function to measure economic growth. \(\mathrm{Y=f(K,L,N)}\), where Y, K, L and N represent output, capital, labor and land respectively. In this model, the overall growth of an economy will compound exponentially and capture economies of scale, implying that economic expansion via consistent growth is a reasonable proposition.

- Growth Accounting: Growth accounting came into popularity after the classical model, identifying the crucial role of technology in economic growth. Using the same classical growth equation, this method of measuring economic growth replaces the ‘land’ variable with ‘technology’ (technology including all of the contextual components that enable growth). In this scenario, technological leaps and bounds can be captured in the overall growth model.

- Salter Cycle: Economic growth is ultimately enabled by increases in productivity, and thus reductions in the required inputs to achieve each subsequent output per unit. As a result, an economy will continuously decrease price and thus increase demand, minimizing marginal utility over time and saturating markets.

- Endogenous Growth Model: This model takes into account technology, as in the growth accounting system discussed above, alongside increases in skills and intellectual capital. A more educated workforce will result in increases in real output, as will advances in technology and innovation.

- Energy Growth Theory: There has been a consistent correlation between economic growth and energy increase, alongside a paradox that increased energy and resource utilization efficiency actually increases consumption of that resource (similar to the Salter Cycle concept). As a result, energy growth theory economists identify a critical role of energy and resources in measuring overall economic growth.

How to Compare Economies Throughout History

Economies throughout history are defined by an evolution towards common currencies, global trade, and technologies driving productivity.

learning OBJECTIVES

- Describe historical trends in rates of economic growth

Comparing historical economies and economic trends over the course of human history is a difficult endeavor, as the comparisons are not always equal. The evolution of trade and the construction of measurement systems, currencies, standards, and the accuracy of historical record present a challenge to economists evaluating economies over time. That being said, timelines have been generated that capture useful insights, and modern economic comparisons (country to country) are growing increasingly accurate. Both of these perspectives shed light as to the overall patterns of economic growth over time.

Relevant Time Periods

For the sake of this discussion, four general time frames are useful to highlight:

- Stone Age: Including the Paleolithic, Mesolithic, and Neolithic time frames (up to 3500 B.C.), economics was virtually basic trade between small, local groups. This age is particularly worthy of note due to the crucial development of bartering and specialization. Specialization refers to the fact that a small group of people performing (and specializing) in different tasks can create substantially more value than every individual learning all tasks (think of Henry Ford’s assembly line).

- Antiquity: This includes the Bronze Age and the Iron Age, antiquity spans from 3500 B.C. around 500 A.D. As the names imply, the leveraging of natural resources (such as metals) were a critical step forward for trade. During this time frame the Babylonians are credited with generating the first metric to measure economic value (i.e. currency), and standardizing trade through leveraging this metric. This is an absolutely critical component to the ultimately measurement and comparison of economies from this time period forward.

- Middle Ages: The Silk Road is a famous economic historical element of this time frame, as is the creation of the first official paper currency (or banknotes) by the Tang Dynasty in China around the 9th century. The Middle Ages stretched from 500 A.D.-1500 A.D., and eventually saw the roots of accounting and financial trade roles in society.

- Modernity: From 1500 A.D. forward, trade grew increasingly global and increasingly standardized as a result. This era is marked by the Industrial Revolution, and the exponential productivity growth inherently found in technological advancement and standardized education systems. As the 20th century dawned, real world GDP is estimated to have quadrupled as a result of the advances in industry, technology and intellectual innovations. Subsequently, population expanded as well.

With these four eras in mind, it is easy to empathize with economists attempting to unveil relative economic strength in the context of capitalist evolution. The modern age provides the most consistent data in which to analyze growth.

Comparing Modern Economies

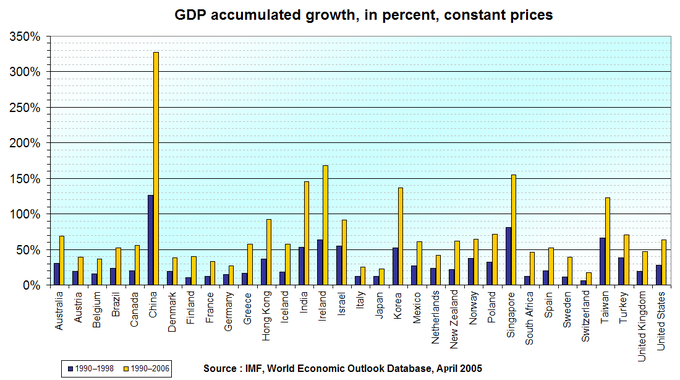

Modern economies have been consistently measured for growth over the past couple centuries, underlining useful economic data on overall growth between nations. To simplify these comparisons, economic growth is generally assessed as general GDP (or increased productivity within a nation). The figure demonstrates these comparisons between 1990 and 2006, with a few countries standing out (China in particular).

GDP Growth Across Nations: This graph underlines the important fact that economic growth is not mutually or equally distributed, resulting from a wide variety of factors with external and global systems.

Over time, countries can change significantly, and these changes must be considered in order to make accurate comparisons. Inflation, for example, changes the value of one unit of currency across time, so comparisons across time should be made using Real GDP, a GDP index, or another measure that accounts for changes in price.

There are also a number of other factors that must be taken into account such as GDP per capita, energy consumption, pollution metrics, education levels, innovation, etc. As you can imagine, it is difficult to compare countries across large time horizons, but, after controlling for as many of these effects as you can, comparisons are possible.

Economic Growth in the 20th Century: As a result of technological advances and increased intellectual capacity, real productivity increased by over 400% during this time frame.

Is Economic Growth a Good Goal?

Economic growth is typically viewed as positive, but there are mixed repercussions of increased productivity within an economic system.

learning OBJECTIVES

- Identify the value of economic growth objectives.

Throughout history, economists have typically assumed a positive relationship between economic growth (increased productivity) and the well-being of a society. It seems logical to assume that a stronger economy would create a higher standard of living. However, there is some debate surrounding the validity of this assumption. Is economic growth the appropriate objective?

Why is Growth Good?

Economic growth is the increase in the market value of the goods and services produced by an economy over time. Simply, more economic growth means that people are able to buy more of the things they like. Presumably, this translates into higher overall utility.

On a societal level, increases in GDP growth and overall productivity generates high prospective tax revenues, both on business profits and consumer purchases. Higher tax revenues will allow governments more financial flexibility to invest in social services such as education, welfare, transportation, etc.

Drawbacks to Economic Growth

There are, however, some downsides to economic growth, which are summarized in the idea of uneconomic growth. The concept of uneconomic growth postulates that the costs of economic growth – primarily environmental and social costs – may outweigh the benefits. There are a few specific observations of this that are worth noting:

- Jevon’s Paradox: Interestingly, increases in efficiency which drive increased economic growth often result in higher consumption. For example, when an economic system creates higher efficiency for generating electricity it will often increase the amount of electricity consumer in spite of that increased efficiency. This creates a culture of consumerism which is often wasteful.

- Malthusian Trap: Named after a political economist named Thomas Robert Malthus, the Malthusian trap simply states that increases in efficiency tend to result in population growth rather than wealth growth. Increased productivity within a system is only useful if it translates to an increase in per capita wealth.

- Imbalanced Distribution: Another issue is income distribution. This is what was meant by the adage that the rich get richer while the poor get poorer. It is quite common to see the rich absorb the vast majority of the value generated through increased productivity, creating a larger relative gap between the rich and the poor. In this circumstance there is limited utilitarian value to economic growth.

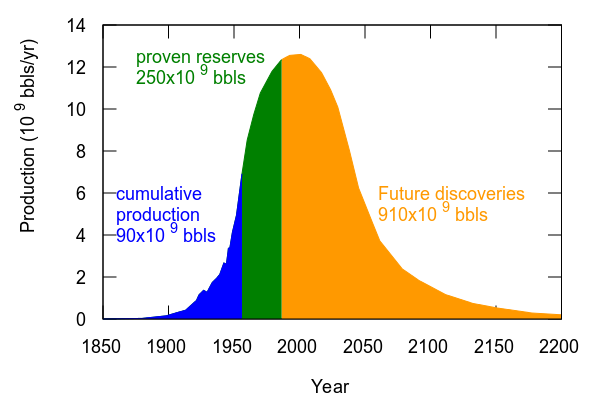

- Environmental Degradation: The final criticism is often the most discussed, particularly in light of the overwhelming evidence of global warming and the destructive nature of excessive consumption. It is also reasonable to consider the finite nature of natural resources (see ). Scientific modeling by environmental scientists often demonstrate significant long-term risks for the well-being of the ecosystem, posing a very real threat to the overall value in continued economic growth. Is it worth having more to consume if there is no ecosystem in which to enjoy it?

The important takeaway from this is to think carefully about the value created by economic growth. It is imperative that increased productivity can be created in a context in which the value can be captured in a positive and meaningful way.

Petroleum Consumption Over Time: This figure demonstrates the risk of over-consuming our natural resources, ultimately resulting in scarcity of necessary goods. A continued drive for economic growth could lead to overconsumption of natural resources.

Key Points

- Economic growth could also be described as an outward shift in the production-possibility frontier, allowing for the generation of a higher quantity of goods.

- While measuring real GDP is useful in some ways, and considered a standard measure of economic growth, there is a great deal more complexity than is being captured (both quantitatively and qualitatively).

- Classic growth theory uses the production function to measure economic growth, which ultimately implies that economic growth constantly compounds.

- Growth accounting came into popularity after the classic model, identifying the crucial role of technology in economic growth.

- A more educated workforce will result in increases in real output, as will advances in technology and innovation.

- Comparing historical economies and economic trends over the course of human history is a difficult endeavor, as the comparisons are not always equal.

- Babylonians are credited with generating the first metric to measure economic value (i.e. currency ) and standardizing trade through leveraging this metric.

- The creation of the first official paper currency (or banknotes) by the Tang Dynasty in China around the 9th century.

- As the 20th century dawned, real world GDP is estimated to have quadrupled as a result of the advances in industry (see, technology, and intellectual innovations.

- Modern economies have been consistently measured for growth over the past couple centuries, underlining useful economic data on overall growth between nations. To simplify these comparisons, economic growth is generally assessed as general GDP.

- The relationship between economic growth and the well-being of a society has largely been viewed as positive throughout the course of history.

- Economic growth increases consumer purchasing power and leisure time along with governmental purchasing power for societal benefits.

- The concept of uneconomic growth postulates that the costs of economic growth may outweigh the benefits, those costs being the environmental and societal repercussions.

- It is imperative that increased productivity can be created in a context in which the value can be captured in a positive and meaningful way.

- It is imperative that increased productivity can be created in a context in which the value can be captured in a positive and meaningful way.

Key Terms

- inflation: The rise in the general level of prices of goods and services in an economy over a period of time.

- gross domestic product: A measure of the economic production of a particular territory in financial capital terms over a specific time period.

- evolution: Gradual directional change especially one leading to a more advanced or complex form; growth; development.

- Bartering: Exchange goods or services without involving money.

- economic growth: The increase of the economic output of a country.

- Jevon’s Paradox: The proposition that technological progress that increases the efficiency with which a resource is used tends to increase the rate of consumption of that resource.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- gross domestic product. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/gross_domestic_product. License: CC BY-SA: Attribution-ShareAlike

- Economic growth. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Economic_growth. License: CC BY-SA: Attribution-ShareAlike

- Gross domestic product. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Gross_domestic_product. License: CC BY-SA: Attribution-ShareAlike

- Growth accounting. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Growth_accounting. License: CC BY-SA: Attribution-ShareAlike

- inflation. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/inflation. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._expansion.svg. License: CC BY-SA: Attribution-ShareAlike

- Economic growth. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Economic_growth. License: CC BY-SA: Attribution-ShareAlike

- Economic history of the world. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Economi...y_of_the_world. License: CC BY-SA: Attribution-ShareAlike

- Bartering. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Bartering. License: CC BY-SA: Attribution-ShareAlike

- evolution. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/evolution. License: CC BY-SA: Attribution-ShareAlike

- economic growth. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/economic_growth. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._expansion.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...th_century.GIF. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...ted_change.png. License: CC BY-SA: Attribution-ShareAlike

- Economic growth. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Economic_growth. License: CC BY-SA: Attribution-ShareAlike

- Uneconomic growth. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Uneconomic_growth. License: CC BY-SA: Attribution-ShareAlike

- Human development theory. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Human_development_theory. License: CC BY-SA: Attribution-ShareAlike

- Malthusian trap. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Malthusian_trap. License: CC BY-SA: Attribution-ShareAlike

- Jevon's Paradox. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Jevon's+Paradox. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: http://upload.wikimedia.org/wikipedi..._expansion.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...th_century.GIF. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: http://upload.wikimedia.org/wikipedi...ted_change.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...k_oil_plot.svg. License: CC BY-SA: Attribution-ShareAlike