What Taxes Do

On a general level, tax collections provide a revenue source to support the outlays or primary activities of a government.

learning objectives

- Explain the role of taxation with respect to consumer and firm behavior

Taxes are the primary source of revenue for most governments. They are simply defined as a charge or fee on income or commerce. Taxes are most readily understood from the perspective of income taxes or sales tax, although there are many other types of taxes levied on both individuals and firms.

Necessarily, taxes raise the price of purchasing the good or resource for firms and consumers. As a result, the quantity demanded and supplied reacts according to the supply and demand curves.

Tax Authority

In the United States, Congress has the power to tax as stated in The United States Constitution, Article 1, Section 8, Clause 1: “The Congress shall have the Power to lay and collect Taxes, Duties, Imposts, and Excises to pay the Debts and provide for the common Defense and general Welfare of the United States.” This power was reinforced in the Sixteenth Amendment to the Constitution: “The Congress shall have the power to lay and collect taxes on income, from whatever source derived, without apportionment among the several States, and without regard to any census or enumeration.”

It is important to note that Congress has delegated to the Internal Revenue Service (IRS) the responsibility of administering the tax laws, known as the Internal Revenue Code (the Code). Congress enacts these tax laws, and the IRS enforces them. Individual states also have the power to tax as do smaller government entities such as towns, cities, counties, and municipalities.

Purpose of Taxation

On a general level, tax collections provide a revenue source to support the outlays or primary activities of a government including but not limited to public buildings, military, national parks, and public welfare in the form of transfer payments. Taxes allow the government to perform and provide services that would not evolve naturally through a free market mechanism, for example, public parks. However, governments also use taxes to establish income equity and modify consumption decisions.

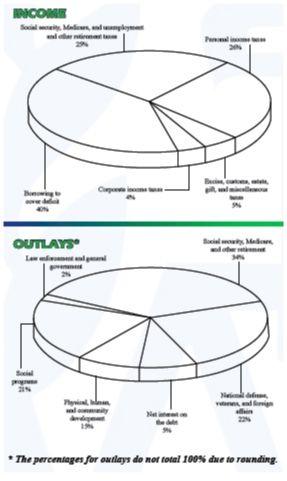

Income and Outlays (IRS Publication 2105; Rev 3-2011): Tax revenue is used by the government to support services and activities available to all residents.

Sources of Tax Revenue: Income Taxation

Governments use different kinds of taxes and vary the tax rates. This is done to distribute the tax burden among individuals or classes of the population involved in taxable activities, such as business, or to redistribute resources between individuals or classes in the population. This type of taxation is referred to as progressive taxation because the tax liability increases in proportion to income.

Sources of Tax Revenue: Sales Taxes

Sales taxes are borne by the consumer when s/he purchases certain goods. It is an ad valorem tax: the charged value is based on the value of what is being sold. This is in contrast to an excise tax, where the charged value is based on the number of items being sold.

Sales tax is a form of regressive taxation; the liability is based on the percentage of income consumed, which is higher for low income earners. As a result, individuals earning a relatively lower income will pay a higher proportion of income in the form of sales tax, defining the regressive nature of the tax. Though a general revenue source, sales taxes are also used to modify behavior. For example taxes on cigarettes are meant to dissuade purchase due to the inherent health implications of smoking.

How Taxes Impact Efficiency: Deadweight Losses

In economics, deadweight loss is a loss of economic efficiency that can occur when equilibrium for a good or service is not Pareto optimal.

learning objectives

- Discuss how taxes create deadweight loss

Deadweight Loss

In economics, a deadweight loss (also known as excess burden or allocative inefficiency) is a loss of economic efficiency that can occur when equilibrium for a good or service is not Pareto optimal (resource allocation where it is impossible to make any one individual better off without making at least one individual worse off). Causes of deadweight loss can include actions that prevent the market from achieving an equilibrium clearing condition (where supply and demand are equal) and include taxes or subsidies and binding price ceilings or floors (including minimum wages). Deadweight loss can generally be referenced as a loss of surplus to either the consumer, producer, or both.

Harberger’s Triangle, Taxes, and Deadweight Loss

Harberger’s triangle, generally attributed to Arnold Harberger, refers to the deadweight loss (as measured on a supply and demand graph) associated with government intervention in a perfect market. This can happen through price floors, caps, taxes, tariffs, or quotas. In the case of a tax on the supplier of a good, the supply curve will shift inward in proportion to the tax and resulting in a non-market clearing level of supply. As a result, the price of the good increases and the quantity available decreases.

Taxation and Deadweight Loss: Taxation can be evaluated as a non-market cost. In this case imposition of taxes reduces supply, resulting in the creation of deadweight loss (triangle bounded by the demand curve and the vertical line representing the after-tax quantity supplied), similar to a binding constraint.

Harberger’s Triangle: Deadweight loss, represented by Harberger’s triangle, is the yellow triangle. It represents lost efficiency.

The area represented by the Harberger’s triangle results from the intersection of the supply and demand curves above market equilibrium resulting in a reduction in consumer surplus and producer surplus relative to their value before the imposition of the tax. The loss of the surplus, not recouped by tax revenues, is deadweight loss.

Some economists have argued that these triangles do not have a huge impact on the economy, whereas others maintain that they can seriously affect long term economic trends by pivoting the trend downwards, causing a magnification of losses in the long run.