Causes and Immediate Impacts of the Crisis

Banks, consumers, and the government all contributed to improper borrowing and lending, which in turn created a downward spiraling economy.

learning objectives

- Summarize the causes that led to the 2007 banking crisis

The recent financial crisis, commonly referred to as the sub-prime mortgage crisis of 2007-2008, was borne of the failure of a series of derivative-based consolidation of mortgage-backed securities that encapsulated extremely high risk loans to homeowners into a falsely ‘safe’ investment. To simplify this, banks pushed mortgages on prospective homeowners who could not afford to repay them. Then they combined and packaged varying mortgage-backed securities based off of these loans and sold them as highly dependable and safe investments, either through a lack of due diligence (negligence) or lack of ethical consideration. This created an economic meltdown, starting with the United States, that spread across the global markets.

The inherent complexity of the causes and dramatic repercussions (most of which are still ongoing) require a great deal of context. It is a fiercely debated and widely discussed issue in the field of economics (and in mainstream media), providing a real-life case study for many of the critical concepts of economic theory.

How Did This Happen?

The inputs to the 2007-2008 economic collapse, briefly touched upon above, are complex and still evolving. That being said, there are a few key talking points from an economic perspective that should be discussed. A useful perspective to take is the various stakeholders and their contributions:

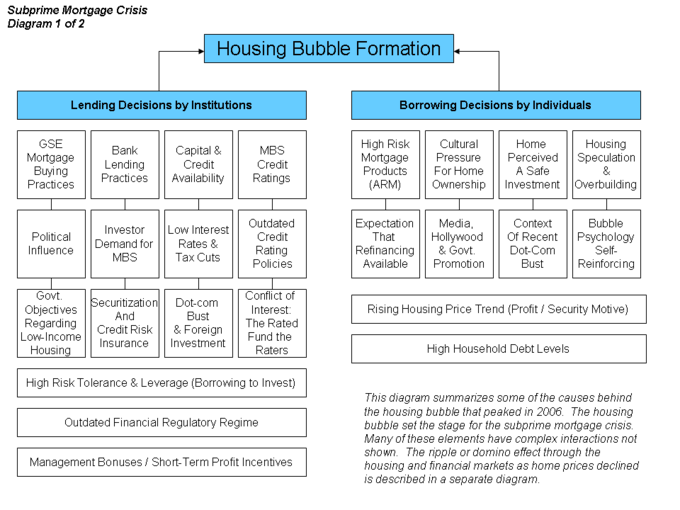

Inputs to the Mortgage Crisis: This graph outlines two of the three parties in the collapse (excludes government), as the banks and the buyers both took on ridiculous amounts of risk.

- Banks: Simply put, the banks made two critical errors. First, they lent money to people who could not pay it back (to buy homes). They pursued what is referred to as ‘predatory lending,’ or lending to individuals they knew could never pay it back. Secondly, banks knowingly grouped these loans into bundles called collateralized debt obligations (CDOs) and sold them as extremely safe derivative investments. They were not safe.

- Consumers: Consumers played their role as well, acting as easy prey for the banks predatory practices. Individuals bought homes they could not afford utilizing loans they could not pay back. This drove them into debt, to the extent at which they had to default. This meant that the capital banks expected to get back did not arrive, it simply was not there.

- Government: The government did not regulate the housing market, as a result of the elimination of two critical legal clauses that required the verification of income and a 20% down payment. In short, the U.S. government used to ensure that prospective home buyers could put down 20% of the their borrowing in addition to verify that their income could cover their mortgage payments. Without such verification, it became easier for people to get mortgages they could not afford.

Combining these factors, the problem largely revolved around irresponsible lending and borrowing which was then turned into derivatives that were labeled safe despite their massive risks. This resulted in an economic realization of loans that could not be repaid, which spread through the banking system and turned into large scale obligations that could not be met.

Economic Impact

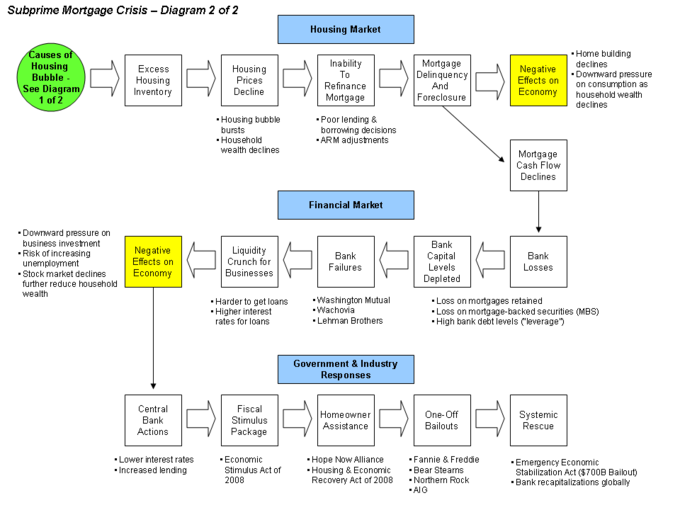

What happened next is well captured in the diagram below. In short, the banks eventually failed due to their investments. In order to prevent the entire financial system from collapsing, some of the banks (and other financial institutions) were bailed out.

2008 Crisis Flow Chart: This chart embodies critical checkpoints in the economic decline reactions to poor mortgage management by the banks. Understanding the implications of each point on this diagram will greatly enhance the larger understanding of the short term effects of this economic collapse.

Of course the negative effects did not stop there. The U.S. stock market lost confidence in financial institutions and some of the companies connected to them and subsequently crashed. The NYSE fell by half, drastically reducing the value of the U.S. economy. This was then telegraphed into a loss of consumer confidence and business access to investment. Within a few months, there were job cuts, bankruptcies, and reduced spending, as the crisis spread throughout the economy (both domestically and globally).

Recovery

The objective of economic recovery when in crisis is to stabilize the economy and recapture the value lost using economic stimulus strategies.

learning objectives

- Discuss the characteristics of the recovery from the 2007 crisis

The 2007-2009 economic crisis has had far-reaching and profound effects on both the domestic and global markets, primarily as a result of the sub-prime mortgage disaster originating in the United States. Addressing these economic ramifications to induce recovery has been the focal point of global governments and global agencies such as the International Monetary Fund (IMF). The objective of economic recovery when in crisis is to stabilize the economy, and from there recapture the value lost through economic stimulus strategies while addressing the factors which contributed to the collapse in the first place.

Stimulus Package

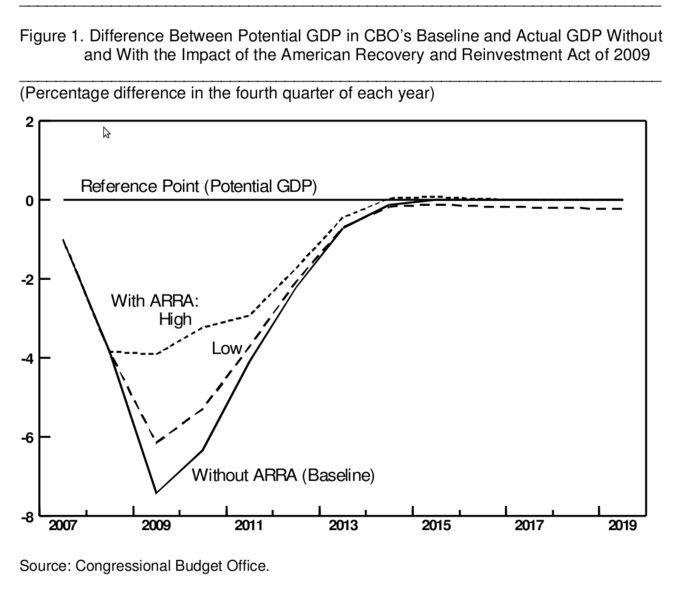

One of the key components to the crisis recover in the United States is an act called the American Recovery and Reinvestment Act of 2009 (ARRA), put into place by the Obama administration just as the first days of his term were beginning. This act has seen substantial debate, both positively and negatively, as to the efficacy and overall implementation of the program. Understanding the inputs, and expected outcomes, is critical to understanding the economics behind reacting to economic crises (particularly from a Keynesian perspective).

The stimulus package can be broken down via the attached figure in regards to monetary investment in specific places, totaling $831 billion (USD) between 2009 and 2019. The goal of investing or providing tax relief and subsidies for individuals and companies is to drive up purchasing behavior and offset the positive feedback loop attributed to economic crises. This is largely based on the Keynesian concept of driving spending through enabling spending, in turn driving up demand, creating jobs, and driving spending up further. President Obama’s administration was criticized by classical economists for employing this as well as Keynesian economists (such as Paul Krugman) for not employing it enough. That being said, the efficacy in the attached figure demonstrates that it was likely a strategic reaction to the economic crisis.

ARRA Efficacy Projections: This graph points out the economic opportunity cost of not utilizing the ARRA, which would likely have left the U.S. (and subsequently, the global) economy in significantly worse shape than it is now.

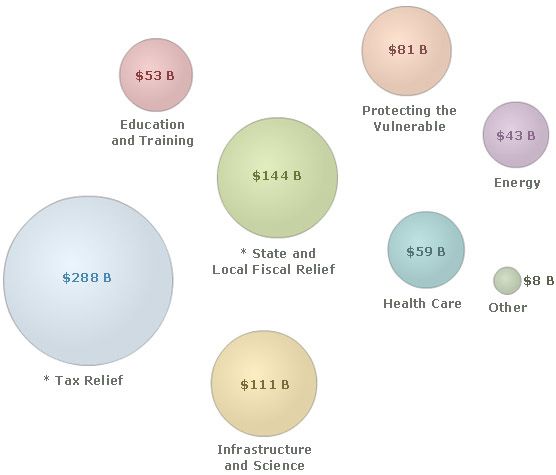

Stimulus Investments (U.S.) of ARRA: This graphic demonstrates the different silos receiving government aid within the domestic economy, as a direct result of the American Recover and Reinvestment Act (ARRA).

Troubled Asset Relief Program (TARP)

Perhaps more debatable still, is the reaction to the inevitable and deserved bankruptcy of the banks and insurers involved in the toxic mortgage-backed securities (i.e. CDO’s) that drove the economy into disaster were bailed out by the government. These companies, such as AIG, Bank of America, Citigroup, and other distributors of toxic investments were handed the required capital by the government to offset their massive losses due to undue risk and poor leveraging. This was in the form of the government utilizing tax money to purchase these securities, removing the toxic assets from the books of the companies involved (who were deemed ‘too big to fail’). This move saved the economic decline and restored consumer confidence through direct government intervention.

TARP was also largely criticized, with a high number of seemingly reasonable objections. The first, and most intuitive, is that these businesses deserved to go under. Bad business practice, poor investment, and grossly unethical behavior deserves bankruptcy. Instead, the government demonstrated that, as long as certain fiscal influence is achieved, these competitive rules are negligible. Secondly, and slightly more complex, is the implementation of the TARP act (which necessitated SIG-TARP, an oversight group ensuring that TARP money went out to those who it was intended for). It was noted on many occasions that TARP money was ill-used.

Outcomes

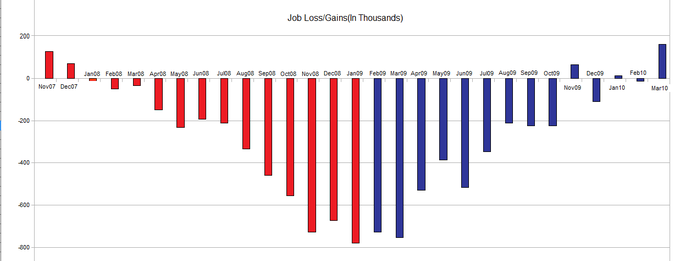

While the long-term outcomes of these practices cannot yet be predicted, the progress made so far is worth analyzing economically. First and foremost, job numbers have improved, although not as much as had been hoped or expected (see ). While this is positive, it does not capture the large number of people who are underemployed or the individuals who have abandoned the search for employment. GDP growth has inched along to positive numbers, as has the profitability of many businesses and industries. Interestingly enough, as of the end of 2013, the stock market has not only recovered but expanded beyond 2007 levels.

U.S. Job Gains and Losses: This graph demonstrates the negative affect that the collapse had on jobs as well as the pacing of economic recovery in the short-term.

Global Impacts

The 2007-2009 economic collapse was damaging not only to the U.S. but also global markets, driving the global economy into recession.

learning objectives

- Analyze the extent to which the 2007 crisis was global

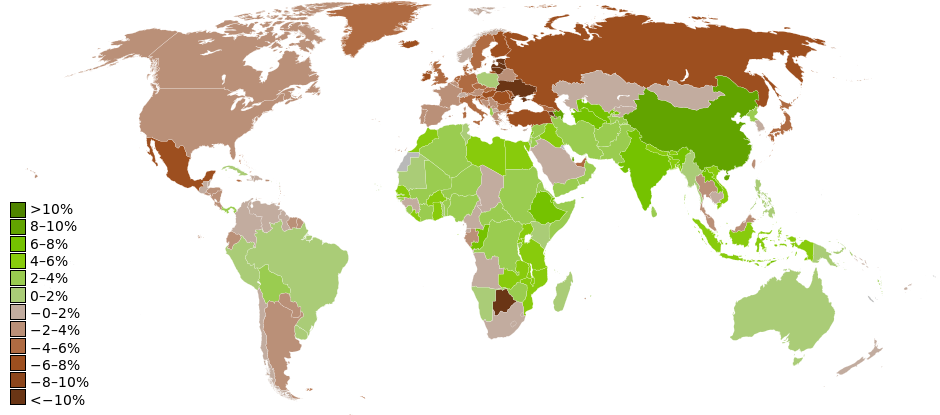

Modern markets are dependent upon one another across national borders, where global trends in economic growth and well-being will have a dramatic impact on national economic well-being and vice versa. As a result, the 2007-2009 economic collapse had large effects not only at the origin (in the United States), but also on a global scale. The speed in which the market decline spread across the globe underlines just how far globalization and international interdependence has come, with GDP growth numbers in 2009 already demonstrating substantial losses across the map (see ).

2009 Global GDP Growth and Decline): As this map illustrates, many international markets fell rapidly into decline as a direct result of the U.S. sub-prime mortgage disaster.

Recession: Domestic to Global

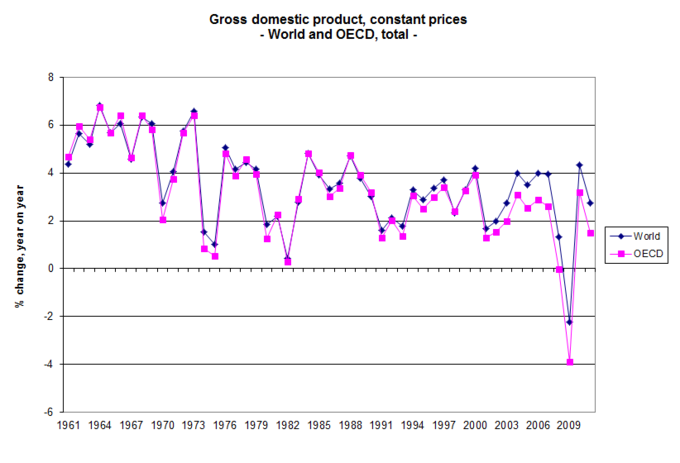

In December 2007, the U.S. officially fell into an 18-month long recessionary period of negative GDP growth (over two consecutive quarters). This recessionary period spread rapidly around the map, creating a global recession in Q3 and Q4 in 2008 and Q1 of 2009 (defined as a contraction in global GDP growth during that time) as is represented in this figure. To provide additional context to the global adverse effects of the sub-prime mortgage crisis, of 65 countries that record and report GDP only 11 escaped a recessionary period between 2006 and today.

World GDP Growth: It is quite clear in this graphic, the global GDP growth dropped dramatically following the U.S. crisis, pitching the entire global economy into a recession.

Even countries where double-digit economic growth had been a consistent trend going into 2008, such as China, began to experience growth reductions due to reduced consumer purchasing power on a global scale. China has seen reductions towards the 7%-8% economic GDP growth (year on year), from clear double-digits in previous years.

Political Instability

Another indirect global impact that occurred as a result of the economic collapse is political instability, primarily due to the inability of developed nations to pursue social welfare investments and global poverty reduction processes during recessionary times. Indeed, these instabilities are not only isolated to developing nations. Countries in the EU, such as Greece, Spain and Italy, have seen dramatic GDP decreases and unemployment numbers reaching or exceeding 20% in some cases. This instability has placed a great deal of pressure on government officials to solve these huge economic problems in the short-term. The United States has also seen an incredible reduction in governmental efficacy with the least effective house of representatives for nearly a century alongside dramatic polarization of public opinion towards left-wing and right-wing ideas.

Global Responses

Positively, many global organizations and countries are actively employing policies to minimize the likelihood of a re-occurrence in the future. Reducing interest rates to drive up borrowing and investment, providing tax benefits to the unemployed and underemployed, and subsidizing new business have created positive steps towards meaningful recovery globally.

There have also been a series of banking and financial regulatory changes across the world.These global safety nets and prevention policies are setting the tone for future strategies to avoid economic crises and minimize the prospective damage that occurs as a result of these unethical practices.

Key Points

- The recent financial crisis, commonly referred to as the sub-prime mortgage crisis of 2007-2008, began with the failure of a series of derivative-based consolidation of mortgage-backed securities that encapsulated extremely high risk loans to home-owners into a falsely ‘safe’ investment.

- Banks offered loans to debtors that couldn’t afford them, and then bundles these debt instruments and sold them.

- The banking crisis spread into a broader financial crisis as companies were negatively affected by the crisis in financial institutions to which they were connected.

- The government did not regulate the housing market at all, as a result of the elimination of two critical clauses: verification of income and a 20% down payment.

- The U.S. stock market, realizing the scale of errors of the banks, lost all investment confidence. This cut the NYSE in half, drastically reducing the value of the U.S. economy.

- One of the key components to the crisis recovery in the United States is an act called the American Recovery and Reinvestment Act of 2009 (ARRA). It invests money in the economy to drive spending and recovery.

- ARRA is largely based on the Keynesian macro-environmental concept of driving spending through enabling spending, in turn driving up demand, creating jobs, and driving spending up further.

- The Troubled Asset Relief Program (TARP) was another recovery strategy, buying toxic assets off the banks to prevent them from failing.

- TARP was criticized for protecting banks who behaved unethically and with a lack of strategic intelligence as businesses, essentially implying that they should have failed.

- While the stock market has recovered and the banks are in better shape now than before the collapse, the average American is still less likely to have a job or to be underemployed.

- Modern markets are dependent upon one another across national borders, where global trends in economic growth and well-being will have a dramatic impact on national economic well-being and vice versa.

- In December 2007, the U.S. officially fell into an 18-month long recessionary period of negative GDP growth, which This spread rapidly around the map to create a global recession in Q3 and Q4 in 2008 and Q1 of 2009.

- Another indirect global impact that occurred as a result of the economic collapse was political instability, primarily due to the inability of developed nations to pursue altruistic investments and global poverty reduction processes during recessionary times.

- On the upside, many global organizations and countries are actively employing policies to minimize the likelihood of a re-occurrence in the future.

Key Terms

- CDO: A type of asset-backed security and structured credit product constructed from a portfolio of fixed-income assets.

- Sub-prime: Designating a loan (typically at a greater than usual rate of interest) offered to a borrower who is not qualified for other loans (e.g. because of poor credit history).

- stimulus: Anything that may have an impact or influence on a system. In 2009, it is the monetary investments in the economy to recover from the collapse.

- Economic crises: A period of economic slowdown characterized by declining productivity and devaluing of financial institutions often due to reckless and unsustainable money lending.

- recession: A significant decline in economic activity spread across the economy, lasting more than a few months, normally visible in real GDP, real income, employment, and industrial production.

LICENSES AND ATTRIBUTIONS

CC LICENSED CONTENT, SHARED PREVIOUSLY

- Curation and Revision. Provided by: Boundless.com. License: CC BY-SA: Attribution-ShareAlike

CC LICENSED CONTENT, SPECIFIC ATTRIBUTION

- Financial crisis of 2007u201308. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financi...007%E2%80%9308. License: CC BY-SA: Attribution-ShareAlike

- Subprime mortgage crisis. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Subprime_mortgage_crisis. License: CC BY-SA: Attribution-ShareAlike

- Sub-prime. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Sub-prime. License: CC BY-SA: Attribution-ShareAlike

- CDO. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/CDO. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...-_10_19_08.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...agram_-_X1.png. License: CC BY-SA: Attribution-ShareAlike

- Financial crisis of 2007u201308. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financial_crisis_of_2007%E2%80%9308. License: CC BY-SA: Attribution-ShareAlike

- Troubled Asset Relief Program. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Troubled_Asset_Relief_Program. License: CC BY-SA: Attribution-ShareAlike

- Great Recession. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Great_Recession. License: CC BY-SA: Attribution-ShareAlike

- American Recovery and Reinvestment Act of 2009. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/American_Recovery_and_Reinvestment_Act_of_2009. License: CC BY-SA: Attribution-ShareAlike

- Subprime mortgage crisis. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Subprime_mortgage_crisis. License: CC BY-SA: Attribution-ShareAlike

- stimulus. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/stimulus. License: CC BY-SA: Attribution-ShareAlike

- Economic crises. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/Economic+crises. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...-_10_19_08.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...agram_-_X1.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._ARRA_2009.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...mentbubble.jpg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...obLossGain.png. License: CC BY-SA: Attribution-ShareAlike

- Financial crisis of 2007u201308. Provided by: Wikipedia. Located at: en.Wikipedia.org/wiki/Financial_crisis_of_2007%E2%80%9308. License: CC BY-SA: Attribution-ShareAlike

- recession. Provided by: Wiktionary. Located at: en.wiktionary.org/wiki/recession. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...-_10_19_08.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/Wikipedia/en/1/13/Subprime_Crisis_Diagram_-_X1.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi..._ARRA_2009.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...mentbubble.jpg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...obLossGain.png. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...eal_Growth.svg. License: CC BY-SA: Attribution-ShareAlike

- Provided by: Wikimedia. Located at: upload.wikimedia.org/wikipedi...upOECDengl.PNG. License: CC BY-SA: Attribution-ShareAlike