In this chapter we will explore:

| 9.1 | The competitive marketplace

|

| 9.2 | Market characteristics

|

| 9.3 | Supply in the short run

|

| 9.4 | Dynamics: Entry and exit

|

| 9.5 | Industry supply in the long run

|

| 9.6 | Globalization and technological change

|

| 9.7 | Perfect competition and market efficiency

|

9.1 The perfect competition paradigm

A competitive market is one that encompasses a very large number of

suppliers, each producing a similar or identical product. Each supplier

produces an output that forms a small part of the total market, and the sum

of all of these individual outputs represents the production of that sector

of the economy. Florists, barber shops, corner stores and dry cleaners all

fit this description.

At the other extreme, a market that has just a single supplier is a

monopolist. For example, the National Hockey League is the sole supplier of

top-quality professional hockey games in North America; Hydro Quebec is a

monopoly electricity distributor in Quebec; Via Rail is the only supplier of

passenger rail services between Windsor, Ontario and the city of Quebec.

We use the word 'paradigm' in the title to this section: It implies that we

will develop a model of supply behaviour for a market in which

there are many small suppliers, producing essentially the same product,

competing with one-another to meet the demands of consumers.

The structures that we call perfect competition and monopoly are extremes in

the market place. Most sectors of the economy lie somewhere between these

limiting cases. For example, the market for internet services usually

contains several providers in any area – some provide using a fibre cable,

others by satellite. The market for smart-phones in North America is dominated by two major

players – Apple and Samsung (although there are several others). Hence, while these markets that have a limited

number of suppliers are competitive in that they freely and perhaps fiercely compete

for the buyer's expenditure, these are not perfectly competitive

markets, because they do not have a very large number of suppliers.

In all of the models we develop in this chapter we will assume that the

objective of firms is to maximize profit – the difference between revenues

and costs.

A perfectly competitive industry is one in which many suppliers, producing an identical product, face many buyers, and no one participant can influence the market.

Profit maximization is the goal of competitive suppliers – they seek to maximize the difference between revenues and costs.

The presence of so many sellers in perfect competition means that each firm

recognizes its own small size in relation to the total market, and that its

actions have no perceptible impact on the market price for the good or

service being traded. Each firm is therefore a price taker—in

contrast to a monopolist, who is a price setter.

The same 'smallness' characteristic was assumed when we examined the demands

of individuals earlier. Each buyer takes the price as given. He or she is

not big enough to be able to influence the price. In contrast, when

international airlines purchase or lease aircraft from Boeing or

Airbus, they negotiate over the price and other conditions of

supply. The market models underlying these types of transactions are

examined in Chapter 11.

Hence, when we describe a market as being perfectly competitive we do not

mean that other market types are not competitive; all market structure are

competitive in the sense that the suppliers wish to make profit, and they

produce as efficiently as possible in order to meet that goal.

9.2 Market characteristics

The key attributes of a perfectly competitive market are the following:

There must be many firms, each one so small that it cannot influence price or quantity in the industry, and powerless

relative to the entire industry.

The product must be standardized. Barber shops offer a

standard product, but a Lexus differs from a Ford. Barbers tend to be price

takers, but Lexus does not charge the same price as Ford, and is a price

setter.

Buyers are assumed to have full information about the product

and its pricing. For example, buyers know that the products of different

suppliers really are the same in quality.

There are many buyers.

There is free entry and exit of firms.

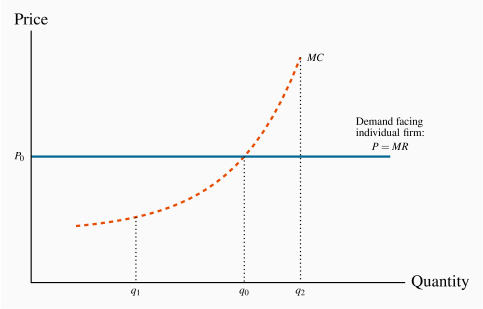

In terms of the demand curve that suppliers face, these market

characteristics imply that the demand curve facing the perfectly competitive

firm is horizontal, or infinitely elastic, as we defined in Chapter 4.

In contrast, the demand curve facing the whole industry

is downward sloping. The demand curve facing a firm is represented in

Figure 9.1. It implies that the supplier can sell any output he

chooses at the going price  . He is a small player in the market, and variations in his output have no perceptible impact in the marketplace. But what quantity should he choose, or

what quantity will maximize his profit? The profit-maximizing choice is his

target, and the MC curve plays a key role in this decision.

. He is a small player in the market, and variations in his output have no perceptible impact in the marketplace. But what quantity should he choose, or

what quantity will maximize his profit? The profit-maximizing choice is his

target, and the MC curve plays a key role in this decision.

9.3 The firm's supply decision

The concept of marginal revenue is key to analyzing the supply

decision of an individual firm. We have used marginal analysis at several

points to date. In consumer theory, we saw how consumers balance the utility

per dollar at the margin in allocating their budget. Marginal

revenue is the additional revenue accruing to the firm from the sale of one

more unit of output.

Marginal revenue is the additional revenue accruing to the firm resulting from the sale of one more unit of output.

In perfect competition, a firm's marginal revenue (MR) is the price of the

good. Since the price is constant for the individual supplier, each

additional unit sold at the price P brings in the same additional revenue.

Therefore, P=MR. For example, whether a dry cleaning business launders 10

shirts or 100 shirts per day, the price charged to customers is the same.

This equality holds in no other market structure, as we shall see in the

following chapters.

Supply in the short run

Recall how we defined the short run in the previous chapter: Each firm's

plant size is fixed in the short run, so too is the number of

firms in an industry. In the long run, each individual firm

can change its scale of operation, and at the same time new firms can enter

or existing firms can leave the industry.

Perfectly competitive suppliers face the choice of how much to produce at

the going market price: That is, the amount that will maximize their profit.

We abstract for the moment on how the price in the marketplace is

determined. We shall see later in this chapter that it emerges as the value

corresponding to the intersection of the supply and demand curves for the

whole market – as described in Chapter 3.

The firm's MC curve is critical in defining the optimal amount to supply

at any price. In Figure 9.1, MC is the firm's marginal

cost curve in the short run. At the price the optimal amount to

supply is  , the amount determined by the intersection of the MC and

the demand. To see why, imagine that the producer chose to supply the

quantity

, the amount determined by the intersection of the MC and

the demand. To see why, imagine that the producer chose to supply the

quantity  . Such an output would leave the opportunity for further

profit untapped. By producing one additional unit beyond , the

supplier would get in additional revenue and incur an additional

cost that is less than in producing this unit. In fact, on every

unit between and he can make a profit, because the MR

exceeds the associated cost, MC. By the same argument, it makes no sense

to increase output beyond , to

. Such an output would leave the opportunity for further

profit untapped. By producing one additional unit beyond , the

supplier would get in additional revenue and incur an additional

cost that is less than in producing this unit. In fact, on every

unit between and he can make a profit, because the MR

exceeds the associated cost, MC. By the same argument, it makes no sense

to increase output beyond , to  for example, because the cost

of such additional units of output, MC, exceeds the revenue from them.

The MC therefore defines an optimal supply response.

for example, because the cost

of such additional units of output, MC, exceeds the revenue from them.

The MC therefore defines an optimal supply response.

Application Box 9.1 The law of one price

If information does not flow then prices in different parts of a market may differ and potential entrants may not know to enter a profitable market.

Consider the fishermen off the coast of Kerala, India in the late 1990s. Their market was studied by Robert Jensen, a development economist. Prior to 1997, fishermen tended to bring their fish to their home market or port. This was cheaper than venturing to other ports, particularly if there was no certainty regarding price. This practice resulted in prices that were high in some local markets and low in others – depending upon the daily catch. Frequently fish was thrown away in low-price markets even though it might have found a favourable price in another village's fish market.

This all changed with the advent of cell phones. Rather than head automatically to their home port, fishermen began to phone several different markets in the hope of finding a good price for their efforts. They began to form agreements with buyers before even bringing their catch to port. Economist Jensen observed a major decline in price variation between the markets that he surveyed. In effect the 'law of one price' came into being for sardines as a result of the introduction of cheap technology and the relatively free flow of information.

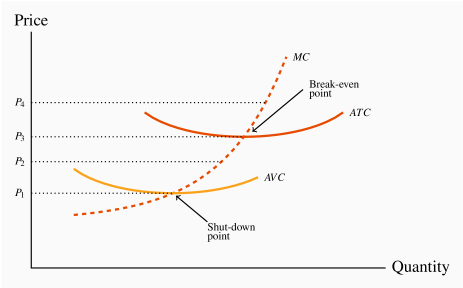

While the choice of the output is the best choice for the producer,

Figure 9.1 does not tell us anything about profit. For that we need more information on costs. Accordingly, in

Figure 9.2 the firm's AVC and ATC curves have been added to

Figure 9.1. As explained in the previous chapter, the ATC

curve includes both fixed and variable cost components, and the MC curve

cuts the AVC and the ATC at their minima.

First, note that any price below  , which corresponds to the minimum

of the ATC curve, yields no profit, since it does not enable the producer

to cover all of his costs. This price is therefore called the

break-even price. Second, any price below

, which corresponds to the minimum

of the ATC curve, yields no profit, since it does not enable the producer

to cover all of his costs. This price is therefore called the

break-even price. Second, any price below  , which

corresponds to the minimum of the AVC, does not even enable the producer

to cover variable costs. What about a price such as

, which

corresponds to the minimum of the AVC, does not even enable the producer

to cover variable costs. What about a price such as  , that lies

between these? The answer is that, if the supplier has already incurred some

fixed costs, he should continue to produce, provided he can cover his

variable cost. But in the long run he must cover all of his costs, fixed and

variable. Therefore, if the price falls below , he should shut down,

even in the short run. This price is therefore called the shut-down price. If a price at least equal to cannot

be sustained in the long run, he should leave the industry. But at a price

such as he can cover variable costs and therefore should continue to

produce in the short run. His optimal output at is defined by the

intersection of the line with the MC curve. The firm's

short-run supply curve is, therefore, that portion of the MC

curve above the minimum of the AVC.

, that lies

between these? The answer is that, if the supplier has already incurred some

fixed costs, he should continue to produce, provided he can cover his

variable cost. But in the long run he must cover all of his costs, fixed and

variable. Therefore, if the price falls below , he should shut down,

even in the short run. This price is therefore called the shut-down price. If a price at least equal to cannot

be sustained in the long run, he should leave the industry. But at a price

such as he can cover variable costs and therefore should continue to

produce in the short run. His optimal output at is defined by the

intersection of the line with the MC curve. The firm's

short-run supply curve is, therefore, that portion of the MC

curve above the minimum of the AVC.

To illustrate this more concretely, consider again the example of our

snowboard producer, and imagine that he is producing in a perfectly

competitive marketplace. How should he behave in response to different

prices? Table 9.1 reproduces the data from Table 8.2.

Table 9.1 Profit maximization in the short run

|

Labour | Output | Total | Average | Average | Marginal | Total | Profit |

|

| | Revenue $ | Variable | Total Cost | Cost $ | Cost $ | |

|

| | | Cost | $ | | | |

|

L | Q | TR | AVC | ATC | MC | TC | TR-TC |

|

0 | 0 | | | | | 3,000 | |

|

1 | 15 | 1,050 | 66.67 | 266.67 | 66.67 | 4,000 | –2,950 |

|

2 | 40 | 2,800 | 50.0 | 125.0 | 40.0 | 5,000 | –2,200 |

|

3 | 70 | 4,900 | 42.86 | 85.71 | 33.33 | 6,000 | –1,100 |

|

4 | 110 | 7,700 | 36.36 | 63.64 | 25.0 | 7,000 | 700 |

|

5 | 145 | 10,150 | 34.48 | 55.17 | 28.57 | 8,000 | 2,150 |

|

6 | 175 | 12,250 | 34.29 | 51.43 | 33.33 | 9,000 | 3,250 |

|

7 | 200 | 14,000 | 35.0 | 50.0 | 40.0 | 10,000 | 4,000 |

|

8 | 220 | 15,400 | 36.36 | 50.0 | 50.0 | 11,000 | 4,400 |

|

9 | 235 | 16,450 | 38.30 | 51.06 | 66.67 | 12,000 | 4,450 |

|

10 | 240 | 16,800 | 41.67 | 54.17 | 200.0 | 13,000 | 3,800 |

Output Price=$70; Wage=$1,000; Fixed Cost=$3,000. The shut-down point occurs at a price of

, where the

AVC attains a minimum. Hence no production, even in the short run, takes place unless the price exceeds this value. The break-even level of output occurs at a price of

, where the

ATC attains a minimum.

The shut-down price corresponds to the minimum value of the AVC curve.

The break-even price corresponds to the minimum of the ATC curve.

The firm's short-run supply curve is that portion of the MC curve above the minimum of the AVC.

Suppose that the price is $70. How many boards should he produce? The

answer is defined by the behaviour of the MC curve. For any output less

than or equal to 235, the MC is less than the price. For example, at L=9

and Q=235, the MC is $66.67. At this output level, he makes a profit on

the marginal unit produced, because the MC is less than the revenue he

gets ($70) from selling it.

But, at outputs above this, he registers a loss on the marginal units

because the MC exceeds the revenue. For example, at L=10 and Q=240,

the MC is $200. Clearly, 235 snowboards is the optimum. To produce more

would generate a loss on each additional unit, because the additional cost

would exceed the additional revenue. Furthermore, to produce fewer

snowboards would mean not availing of the potential for profit on additional

boards.

His profit is based on the difference between revenue per unit and cost per

unit at this output: (P–ATC). Since the ATC for the 235 units produced

by the nine workers is $51.06, his profit margin is  per board, and total profit is therefore

per board, and total profit is therefore  .

.

Let us establish two other key outputs and prices for the producer. First,

the shut-down point is the minimum of his AVC curve. Table 9.1

indicates that the price must be at least $34.29 for him

to be willing to supply any output, since that is the value of the

AVC at its minimum. Second, the minimum of his ATC is at $50.

Accordingly, provided the price exceeds $50, he will cover both variable

and fixed costs and make a maximum profit when he chooses an output where

P=MC, above  . It follows that the short-run supply curve for

Black Diamond Snowboards is the segment of the MC curve in

Figure 8.4 above the AVC curve.

. It follows that the short-run supply curve for

Black Diamond Snowboards is the segment of the MC curve in

Figure 8.4 above the AVC curve.

Given that we have developed the individual firm's supply curve, the next

task is to develop the industry supply curve.

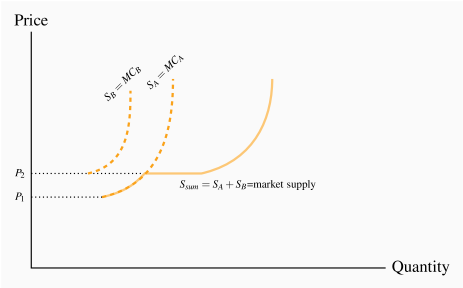

Industry supply in the short run

In Chapter 3 it was demonstrated that individual demands

can be aggregated into an industry demand by summing them horizontally. The

industry supply is obtained in exactly the same manner—by summing the

firms' supply quantities across all firms in the industry.

To illustrate, imagine we have many firms, possibly operating at different

scales of output and therefore having different short-run MC curves. The

MC curves of two of these firms are illustrated in Figure 9.3.

The MC of A is below the MC of B; therefore, B

likely has a smaller scale of plant than A. Consider first the supply

decisions in the price range P1 to P2. At any price between these

limits, only firm A will supply output – firm B does not cover its AVC in

this price range. Therefore, the joint contribution to industry supply of

firms A and B is given by the MC curve of firm A. But once a price of P2

is attained, firm B is now willing to supply. The  schedule is the

horizontal addition of their supply quantities. Adding the supplies of every

firm in the industry in this way yields the industry supply.

schedule is the

horizontal addition of their supply quantities. Adding the supplies of every

firm in the industry in this way yields the industry supply.

Industry supply (short run) in perfect competition is the horizontal sum of all firms' supply curves.

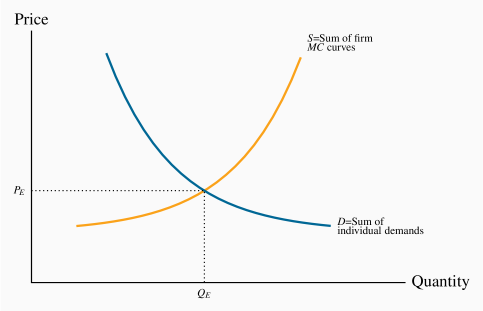

Industry equilibrium

Consider next the industry equilibrium. Since the industry supply is the sum

of the individual supplies, and the industry demand curve is the sum of

individual demands, an equilibrium price and quantity (PE,QE) are

defined by the intersection of these industry-level curves, as in

Figure 9.4. Here, each firm takes PE as given (it is so small that it

cannot influence the going price), and supplies an amount determined by the

intersection of this price with its MC curve. The sum of such quantities

is therefore QE.

Short-run equilibrium in perfect competition occurs when each firm maximizes profit by producing a quantity where P=MC, provided the price exceeds the minimum of the average variable cost.

9.4 Dynamics: Entry and exit

We have now described the market and firm-level equilibrium in the short

run. However, this equilibrium may be only temporary; whether it can be

sustained or not depends upon whether profits (or losses) are being

incurred, or whether all participant firms are making what are termed normal

profits. Such profits are considered an essential part of a firm's

operation. They reflect the opportunity cost of the resources used in

production. Firms do not operate if they cannot make a minimal, or normal,

profit level. Above such profits are economic profits (also

called supernormal profits), and these are what entice entry

into the industry.

Recall from Chapter 7 that accounting and

economic profits are different. The economist includes opportunity costs in

determining profit, whereas the accountant considers actual revenues and

costs. In the example developed in Section 7.2 the

entrepreneur recorded accounting profit, but not economic profit. Suppose

now that the numbers were slightly different, and are as defined in Table 9.2: Felicity invests $250,000 in her business

in the form of capital, as before. But she now has gross revenues of

$165,000 and incurs a cost of $90,000 to buy the clothing wholesale that

she then sells retail. She pays herself a salary of $35,000. If these

numbers represent her balance sheet, then she records an accounting profit

of $40,000.

Table 9.2 Economic profits

|

Sales | | $165,000 |

|

Materials costs | | $90,000 |

|

Wage costs | | $35,000 |

|

Accounting profit | | $40,000 |

|

Capital invested | $250,000 | |

|

Implicit return on capital at 4% | | $10,000 |

|

Additional implicit wage costs | | $20,000 |

|

Total implicit costs | | $30,000 |

|

Economic profit | | $10,000 |

Her economic profit calculation must include opportunity costs. The

opportunity cost of tying up $250,000 of capital, if the interest rate is

4%, amounts to $10,000. In addition, if Felicity could earn $55,000 in

her best alternative job then an additional implicit cost of $20,000 must

be considered. When these two opportunity (or implicit) costs are added to

the balance sheet, her profit is reduced to $10,000. This is her economic

profit. If Felicity's economic profit is representative of the retail

clothing sector of the economy, then that profitability should attract new

entrepreneurs. Our conclusion is that this sector of the economy should experience new entrants and hence an outward shift of the supply curve. In contrast, in the numerical example considered in Section 7.2, Felicity was experiencing losses (negative economic profits),

and in the longer term she would have to consider leaving the business. If

she and other suppliers exited, then the market supply curve would shift

back to the left – representing a reduction in supply.

The critical point in this distinction between accounting and economic cost

is that the decision to enter or leave a market in the longer term is based

on what the entrepreneur can earn in the wider market place. That is,

economic profits rather than accounting profits will determine the

equilibrium number of firms in the long term. In terms of our cost curves,

we will assume that the full economic costs are included in the various

curves that we use. Consequently any profits (or losses) that arise are

based upon the full economic costs of the firm's operation.

Economic (supernormal) profits are those profits above normal profits that induce firms to enter an industry.

Let us return to our graphical analysis, and begin by supposing that the

market equilibrium described in Figure 9.4 results in profits

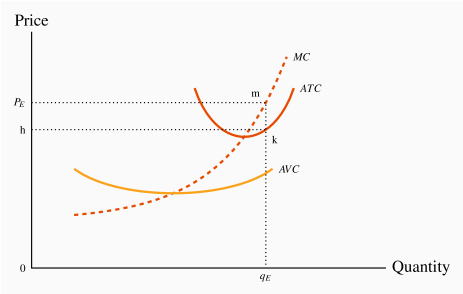

being made by some firms. Such an outcome is described in Figure 9.5, where the price exceeds the ATC. At the price  , a profit-making firm supplies the quantity

, a profit-making firm supplies the quantity  , as determined

by its MC curve. On average, the cost of producing each unit of output, , is defined by the point on the ATC at that output level, point k. Profit per unit is thus given by the value (m–k) – the difference

between revenue per unit and cost per unit. Total (economic) profit is

therefore the area

, as determined

by its MC curve. On average, the cost of producing each unit of output, , is defined by the point on the ATC at that output level, point k. Profit per unit is thus given by the value (m–k) – the difference

between revenue per unit and cost per unit. Total (economic) profit is

therefore the area  , which is quantity times profit per unit.

, which is quantity times profit per unit.

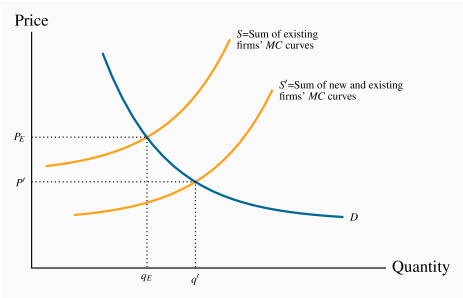

While represents an equilibrium for the firm, it is only a

short-run, or temporary, equilibrium for the industry. The assumption of

free entry and exit implies that the presence of economic profits will

induce new entrepreneurs to enter and start producing. The impact of this

dynamic is illustrated in Figure 9.6. An increased number

of firms shifts supply rightwards to become  , thereby increasing

the amount supplied at any price. The impact on price of this supply shift

is evident: With an unchanged demand, the equilibrium price must fall.

, thereby increasing

the amount supplied at any price. The impact on price of this supply shift

is evident: With an unchanged demand, the equilibrium price must fall.

How far will the price fall, and how many new firms will enter this

profitable industry? As long as economic profits exist new firms will enter

and the resulting increase in supply will continue to drive the price

downwards. But, once the price has been driven down to the minimum of the ATC of a representative firm, there is no longer an incentive for new

entrepreneurs to enter. Therefore, the

long-run industry

equilibrium is where the market price equals the minimum point of a firm's ATC curve. This generates normal profits, and there is no incentive for

firms to enter or exit.

A long-run equilibrium in a competitive industry requires a price equal to the minimum point of a firm's ATC. At this point, only normal profits exist, and there is no incentive for firms to enter or exit.

In developing this dynamic, we began with a situation in which economic

profits were present. However, we could have equally started from a position

of losses. With a market price between the minimum of the AVC and the

minimum of the ATC in Figure 9.5, revenues per unit

would exceed variable costs but not total costs per unit. When firms cannot

cover their ATC in the long run, they will cease production. Such closures

must reduce aggregate supply; consequently the market supply curve

contracts, rather than expands as it did in Figure 9.6.

The reduced supply drives up the price of the good. This process continues

as long as firms are making losses. A final industry equilibrium is attained

only when the price reaches a level where firms can make a normal profit.

Again, this will be at the minimum of the typical firm's ATC.

Accordingly, the long-run equilibrium is the same, regardless of whether we

begin from a position in which firms are incurring losses, or where they are

making profits.

Application Box 9.2 Entry and exit: Oil rigs

Oil drilling is a competitive market. There are a large number of suppliers, information is ubiquitous, and entry and exit are relatively free.

In the years 2012 and 2013 the price of crude oil was around $100 US per barrel. Towards the end of 2014 the price of oil began to drop on world markets, and by early 2015 it fluctuated around $50. The response of drillers in the US was substantial and immediate. The number of active rigs declined dramatically. In terms of our economic model, certain suppliers exited; they moth-balled their rigs and waited for the price of oil to recover.

Another such cycle, even more pronounced, occurred in 2020. With the coronavirus pandemic, the demand for oil dropped and its price plummeted. Again, many firms shut down their rigs and had no choice but to sit out the price decline. A highly informative graphic is presented at tradingeconomics.com/united-states/crude-oil-rigs.

In addition to the decline in traditional oil recovery rigs, the number of operating shale crews declined by even greater amounts. Details at https://www.forbes.com/sites/davidblackmon/2020/05/12/a-grim-earnings-season-for-the-us-shale-business/#6f55a95a1cf2

9.5 Long-run industry supply

When aggregating the firm-level supply curves, as illustrated in

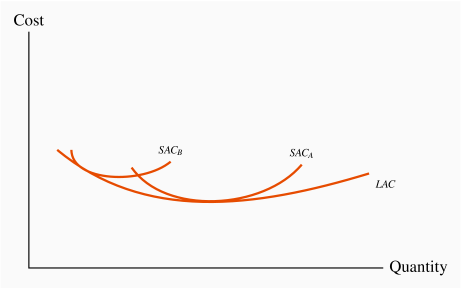

Figure 9.3, we did not assume that all firms were identical. In

that example, firm A has a cost structure with a lower AVC curve, since

its supply curve starts at a lower dollar value. This indicates that firm A

may have a larger plant size than firm B – one that puts A closer to the

minimum efficient scale region of its long-run ATC curve.

Can firm B survive with his current scale of operation in the long run? Our

industry dynamics indicate that it cannot. The reason is that, provided

some firms are making economic profits, new entrepreneurs will

enter the industry and drive the price down to the minimum of the ATC curve

of those firms who are operating with the lowest cost plant size.

B-type firms will therefore be forced either to leave the industry or to

adjust to the least-cost plant size—corresponding to the lowest point on

its long-run ATC curve. Remember that the same technology is

available to all firms; they each have the same long-run ATC curve, and

may choose different scales of operation in the short run, as illustrated in

Figure 9.7. But in the long run they must all produce

using the minimum-cost plant size, or else they will be driven from the

market.

This behaviour enables us to define a long-run industry supply.

The long run involves the entry and exit of firms, and leads to a price

corresponding to the minimum of the long-run ATC curve. Therefore, if the

long-run equilibrium price corresponds to this minimum, the long-run

supply curve of the industry is defined by a particular price value—it is

horizontal at the price corresponding to the minimum of the LATC. More or

less output is produced as a result of firms entering or leaving the

industry, with those present always producing at the same unit cost in a

long-run equilibrium.

Industry supply in the long run in perfect competition is horizontal at a price corresponding to the minimum of the representative firm's long-run ATC curve.

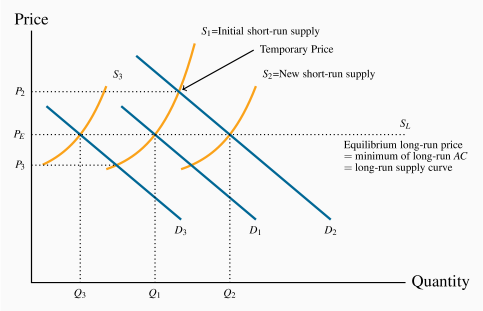

This industry's long-run supply curve, SL, and a particular short-run

supply are illustrated in Figure 9.8. Different points on

SL are attained when demand shifts. Suppose that, from an initial

equilibrium Q1, defined by the intersection of D1 and S1, demand

increases from D1 to D2 because of a growth in income. With a fixed

number of firms, the additional demand can be met only at a higher price (P2),

where each existing firm produces more using their existing plant size. The

economic profits that result induce new operators to produce. This addition

to the industry's production capacity shifts the short-run supply outwards

and price declines until normal profits are once again being made. The new

long-run equilibrium is at Q2, with more firms each producing at the

minimum of their long-run ATC curve, PE.

The same dynamic would describe the industry reaction to a decline in

demand—price would fall, some firms would exit, and the resulting

contraction in supply would force the price back up to the long-run

equilibrium level. This is illustrated by a decline in demand from D1 to

D3.

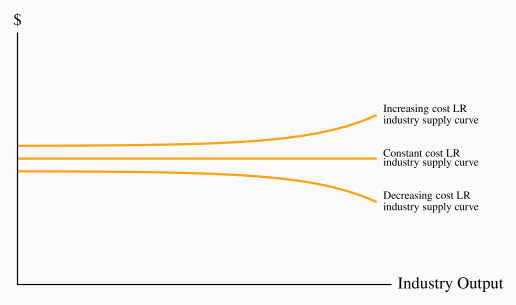

Increasing and decreasing cost industries

While a horizontal long-run supply is the norm for perfect competition, in

some industries costs increase with the scale of industry output; in others

they decrease. This may be because all of the producers use a particular

input that itself becomes more or less costly, depending upon the amount

supplied.

Decreasing cost sectors are those that benefit from a decline in

the prices of their inputs as the size of their market expands. This is

frequently because the suppliers of the inputs themselves can benefit from

scale economies as a result of expansion in the market for the final good. A

case in point has been the computer market, or the tablet market: As output

in these markets has grown, the producers of videocards and random-access

memory have benefited from scale economies and thus been able to sell these

components at a lower price to the manufacturers of the final goods. An

example of an increasing cost market is the market for landings and

take-offs at airports. Airports are frequently limited in their ability to

expand their size and build additional runways. In such markets, as use

grows, planes about to land may have to adopt a circling holding pattern,

while those departing encounter clearance delays. Such delays increase the

time costs to passengers and the fuel and labour costs to the suppliers.

Decreasing and increasing industry costs are reflected in the long-run

industry supply curve by a downward-sloping segment or an upward sloping

segment, as illustrated in Figure 9.9.

Increasing (decreasing) cost industry is one where costs rise (fall) for each firm because of the scale of industry operation.

9.6 Globalization and technological change

Globalization and technological change have had a profound impact on the way

goods and services are produced and brought to market in the modern world.

The cost structure of many firms has been reduced by outsourcing to

lower-wage economies. Furthermore, the advent of the communications

revolution has effectively increased the minimum efficient scale for

many industries, as illustrated in Chapter 8

(Figure 8.7). Larger firms are less difficult to manage nowadays,

and the LAC curve may not slope upwards until very high output levels are

attained. The consequence is that some industries may not have sufficient

"production space" to sustain a large number of firms. In order to reap

the advantages of scale economies, firms become so large that they can

supply a significant part of the market. They are no longer so small as to

have no impact on the price.

Outsourcing and easier communications have in many cases simply eliminated

many industries in the developed world. Garment making is an example. Some

decades ago Quebec was Canada's main garment maker: Brokers dealt with

'cottage-type' garment assemblers outside Montreal and Quebec City. But

ultimately the availability of cheaper labour in the developing world

combined with efficient communications undercut the local manufacture. Most

of Canada's garments are now imported. Other North American and European

industries have been impacted in similar ways. Displaced labour has had to

reskill, retool, reeducate itself, and either seek alternative employment in

the manufacturing sector, or move to the service sector of the economy, or

retire.

Globalization has had a third impact on the domestic economy, in so far as

it reduces the cost of components. Even industries that continue to

operate within national boundaries see a reduction in their cost structure

on account of globalization's impact on input costs. This is particularly in

evidence in the computing industry, where components are produced in

numerous low-wage economies, imported to North America and assembled into

computers domestically. Such components are termed intermediate goods.

9.7 Efficient resource allocation

Economists have a particular liking for competitive markets. The reason is

not, as is frequently thought, that we love competitive battles; it really

concerns resource allocation in the economy at large. In Chapter 5

we explained why markets are frequently an excellent vehicle

for transporting the economy's resources to where they are most valued: A

perfectly competitive marketplace in which there are no externalities

results in resources being used up to the point where the demand and supply

prices are equal. If demand is a measure of marginal benefit and supply is a

measure of marginal cost, then a perfectly competitive market ensures that

this condition will hold in equilibrium. Perfect competition,

therefore, results in resources being used efficiently.

Our initial reaction to this perspective may be: If market equilibrium is

such that the quantity supplied always equals the quantity demanded, is not

every market efficient? The answer is no. As we shall see in the next

chapter on monopoly, the monopolist's supply decision does not reflect the

marginal cost of resources used in production, and therefore does not result

in an efficient allocation in the economy.

Key Terms

Perfect competition: an industry in which many suppliers, producing an identical product, face many buyers, and no one participant can influence the market.

Profit maximization is the goal of competitive suppliers – they seek to maximize the difference between revenues and costs.

Marginal revenue is the additional revenue accruing to the firm resulting from the sale of one more unit of output.

Shut-down price corresponds to the minimum value of the AVC curve.

Break-even price corresponds to the minimum of the ATC curve.

Short-run supply curve for perfect competitor: the portion of the MC curve above the minimum of the AVC.

Industry supply (short run) in perfect competition is the horizontal sum of all firms' supply curves.

Short-run equilibrium in perfect competition occurs when each firm maximizes profit by producing a quantity where P=MC.

Economic (supernormal) profits are those profits above normal profits that induce firms to enter an industry. Economic profits are based on the opportunity cost of the resources used in production.

Long-run equilibrium in a competitive industry requires a price equal to the minimum point of a firm's ATC. At this point, only normal profits exist, and there is no incentive for firms to enter or exit.

Industry supply in the long run in perfect competition is horizontal at a price corresponding to the minimum of the representative firm's long-run ATC curve.

Increasing (decreasing) cost industry is one where costs rise (fall) for each firm because of the scale of industry operation.

Exercises for Chapter 9

Wendy's Window Cleaning is a small local operation. Wendy presently cleans the outside windows in her neighbours' houses for $36 per house. She does ten houses per day. She is incurring total costs of $420, and of this amount $100 is fixed. The cost per house is constant.

What is the marginal cost associated with cleaning the windows of one house – we know it is constant?

At a price of $36, what is her break-even level of output (number of houses)?

If the fixed cost is 'sunk' and she cannot increase her output in the short run, should she shut down?

A manufacturer of vacuum cleaners incurs a constant variable cost of production equal to $80. She can sell the appliances to a wholesaler for $130. Her annual fixed costs are $200,000. How many vacuums must she sell in order to cover her total costs?

For the vacuum cleaner producer in Exercise 9.2:

Draw the MC curve.

Next, draw her AFC and her AVC curves.

Finally, draw her ATC curve.

In order for this cost structure to be compatible with a perfectly competitive industry, what must happen to her MC curve at some output level?

Consider the supply curves of two firms in a competitive industry: P=qA and P=2qB.

On a diagram, draw these two supply curves, marking their intercepts and slopes numerically (remember that they are really MC curves).

Now draw a supply curve that represents the combined supply of these two firms.

Amanda's Apple Orchard Productions Limited produces 10,000 kilograms of apples per month. Her total production costs at this output level are $8,000. Two of her many competitors have larger-scale operations and produce 12,000 and 15,000 kilos at total costs of $9,500 and $11,000 respectively. If this industry is competitive, on what segment of the LAC curve are these producers producing?

Consider the data in the table below. TC is total cost, TR is total revenue, and Q is output.

|

Q | 0 | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 | 9 | 10 |

|

TC | 10 | 18 | 24 | 31 | 39 | 48 | 58 | 69 | 82 | 100 | 120 |

|

TR | 0 | 11 | 22 | 33 | 44 | 55 | 66 | 77 | 88 | 99 | 110 |

Add some extra rows to the table and for each level of output calculate the MR, the MC and total profit.

Next, compute AFC, AVC, and ATC for each output level, and draw these three cost curves on a diagram.

What is the profit-maximizing output?

How can you tell that this firm is in a competitive industry?

Optional: The market demand and supply curves in a perfectly competitive industry are given by: Qd=30,000–600P and Qs=200P–2000.

Draw these functions on a diagram, and calculate the equilibrium price of output in this industry.

Now assume that an additional firm is considering entering. This firm has a short-run MC curve defined by MC=10+0.5q, where q is the firm's output. If this firm enters the industry and it knows the equilibrium price in the industry, what output should it produce?

Optional: Consider two firms in a perfectly competitive industry. They have the same MC curves and differ only in having higher and lower fixed costs. Suppose the ATC curves are of the form: 400/q+10+(1/4)q and 225/q+10+(1/4)q. The MC for each is a straight line: MC=10+(1/2)q.

In the first column of a spreadsheet enter quantity values of 1, 5, 10, 15, 20,..., 50. In the following columns compute the ATC curves for each quantity value.

Compute the MC at each output in the next column, and plot all three curves.

Compute the break-even price for each firm.

Explain why both of these firms cannot continue to produce in the long run in a perfectly competitive market.