In this chapter we will explore:

| 11.1 | The principle ideas

|

| 11.2 | Imperfect competitors

|

| 11.3 | Imperfect competitors: measures of structure and market power

|

| 11.4 | Imperfect competition: monopolistic competition

|

| 11.5 | Imperfect competition: economies of scope and platforms

|

| 11.6 | Strategic behaviour: oligopoly and games

|

| 11.7 | Strategic behaviour: duopoly and Cournot games

|

| 11.8 | Strategic behaviour: entry, exit and potential competition

|

| 11.9 | Matching markets: design

|

11.1 The principle ideas

The preceding chapters have explored extreme forms of supply: The monopolist

is the sole supplier and possesses as much market power as possible. In

contrast, the perfect competitor is small and has no market power

whatsoever. He simply accepts the price for his product that is determined

in the market by the forces of supply and demand. These are very useful

paradigms to explore, but the real world for the most part lies between

these extremes. We observe that there are a handful of dominant brewers in

Canada who supply more than three quarters of the market, and they are

accompanied by numerous micro brewers that form the fringe of the brewing

business. We have a small number of air carriers and one of them controls

half of the national market. The communications market has just three major

suppliers; the Canadian Football League has nine teams and there are just a

handful of major hardware/builders' suppliers stores nationally. At the

other end of the spectrum we have countless restaurants and fitness centres,

but they do not supply exactly the same product to the marketplaces for

'food' or 'health', and so these markets are not perfectly competitive,

despite the enormous number of participants.

In this chapter we will explore three broad topics: First is the

relationship between firm behaviour and firm size relative to the whole

sector. This comes broadly under the heading of imperfect

competition and covers a variety of market forms. Second, we will explore

the principle modern ideas in strategic behavior. In a sense all

decisions in microeconomics have an element of strategy to them - economic

agents aim to attain certain goals and they adopt specific maximizing

strategies to attain them. But in this chapter we explore a more specific

concept of strategic behavior - one that focuses upon direct interactions

between a small number of players in the market place. Third, we explore the

principle characteristics of what are termed matching' markets.

These are markets where transactions take place without money and involve

matching heterogeneous suppliers with heterogeneous buyers.

11.2 Imperfect competitors

Imperfect competitors can be defined by the number of firms in

their sector, or the share of total sales going to a small number of

suppliers. They can also be defined in terms of the characteristics of the demand curves they all face. A

perfect competitor faces a perfectly elastic demand at the existing market

price, and this is the only market structure to have this characteristic. In all

other market structures suppliers effectively face a downward-sloping

demand. This means that they have some influence on the price of the good,

and also that if they change the price they charge, they can expect demand

to reflect this in a predictable manner. So, in theory, we can classify all market

structures apart from perfect competition as being imperfectly competitive. In practice we use the term to denote firms that fall between the extremes of perfect competition and monopoly.

Imperfectly competitive firms face a downward-sloping demand curve, and their output price reflects the quantity sold.

The demand curve for the firm and industry coincide for the monopolist, but

not for other imperfectly competitive firms. It is convenient to categorize

the producing sectors of the economy as either having a relatively small

number of participants, or having a large number. The former market

structures are called oligopolistic, and the latter are called monopolistically competitive. The word oligopoly

comes from the Greek word oligos meaning few, and polein

meaning to sell.

Oligopoly defines a market with a small number of suppliers.

Monopolistic competition defines a market with many sellers of products that have similar characteristics. Monopolistically competitive firms can exert only a small influence on the whole market.

The home appliance industry is an oligopoly. The prices of KitchenAid appliances depend not only on their own output and sales, but also on the

prices of Whirlpool, Maytag and Bosch. If a firm

has just two main producers it is called a duopoly. Canadian National and Canadian Pacific are the only two major rail freight carriers

in Canada; they thus form a duopoly. In contrast, the local Italian restaurant is

a monopolistic competitor. Its output is a package of distinctive menu

choices, personal service, and convenience for local customers. It can

charge a different price than the out-of-neighbourhood restaurant, but if

its prices are too high local diners may travel elsewhere for their food

experience, or switch to a different cuisine locally. Many markets are defined by producers who supply similar but not

identical products. Canada's universities all provide degrees, but they differ one from another in their programs, their balance of

in-class and on-line courses, their student activities, whether they are

science based or liberal arts based, whether they have cooperative programs

or not, and so forth. While universities are not in the business of making

profit, they certainly wish to attract students, and one way of doing this

is to differentiate themselves from other institutions. The profit-oriented

world of commerce likewise seeks to increase its market share by

distinguishing its product line.

Duopoly defines a market or sector with just two firms.

These distinctions are not completely airtight. For example, if a sole

domestic producer is subject to international competition it cannot act in

the way we described in the previous chapter – it has potential, or actual,

competition. Bombardier may be Canada's sole rail car manufacturer,

but it is not a monopolist, even in Canada. It could best be described as

being part of an international oligopoly in rail-car manufacture. Likewise,

it is frequently difficult to delineate the boundary of a given market. For

example, is Canada Post a monopoly in mail delivery, or an

oligopolist in hard-copy communication? We can never fully remove these

ambiguities.

The role of cost structures

A critical determinant of market structure is the way in which demand and

cost interact to determine the likely number of market participants in a

given sector or market. Structure also evolves over the long run: Time is

required for entry and exit.

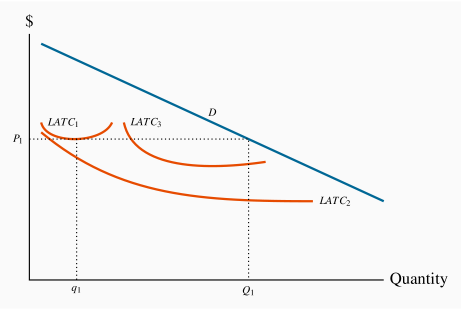

Figure 11.1 shows the demand curve D for

the output of an industry in the long run. Suppose, initially, that all

firms and potential entrants face the long-run average cost curve LATC1.

At the price P1, free entry and exit means that each firm produces q1.

With the demand curve D, industry output is Q1. The number of firms in

the industry is N1 (=Q1/q1). If q1, the minimum average cost

output on LATC1, is small relative to D, then N1 is large. This

outcome might be perfect competition (N virtually infinite), or

monopolistic competition (N large) with slightly differentiated products

produced by each firm.

Instead, suppose that the production structure in the industry is such that

the long-run average cost curve is LATC2. Here, scale economies are vast,

relative to the market size. At the lowest point on this cost curve, output

is large relative to the demand curve D. If this one firm were to act like

a monopolist it would produce an output where MR=MC in the long run and

set a price such that the chosen output is sold. Given the scale economies,

there may be no scope for another firm to enter this market, because such a

firm would have to produce a very high output to compete with the existing

producer. This situation is what we previously called a "natural"

monopolist.

Finally, the cost structure might involve curves of the type LATC3, which

would give rise to the possibility of several producers, rather than one or

very many. This results in oligopoly.

It is clear that one crucial determinant of market structure is

minimum efficient scale relative to the size of the total market as shown

by the demand curve. The larger the minimum efficient scale relative to

market size, the smaller is the number of producers in the industry.

11.3 Imperfect competitors: measures of structure and market power

Sectors of the economy do not fit neatly into the limited number of categories

described above. The best we can say in most cases is that they resemble

more closely one type of market than another. Consider the example of

Canada's brewing sector: It has two large brewers in Molson-Coors

and Labatt, a couple of intermediate sized firms such as

Sleeman, and an uncountable number of small boutique brew pubs. While such

a large number of brewers satisfy one requirement for perfect competition,

it would not be true to say that the biggest brewers wield no market power;

and this is the most critical element in defining market structure.

By the same token, we could not define this market as a duopoly: Even though

there are just two major participants, there are countless others who,

together, are important.

One way of defining what a particular structure most closely resembles is to

examine the percentage of sales in the market that is attributable to a small number

of firms. For example: What share is attributable to the largest three or

four firms? The larger the share, the more concentrated the market

power. Such a statistic is called a concentration ratio. The N-firm concentration ratio is the sales share of the largest

N firms in that sector of the economy.

The N-firm concentration ratio is the sales share of the largest N firms in that sector of the economy.

Table 11.1 Concentration in Canadian food processing 2011

|

Sector | % of shipments |

|

Sugar | 98 |

|

Breakfast cereal | 96 |

|

Canning | 60 |

|

Meat processing | 23 |

Source: "Four Firm Concentration Ratios (CR4s) for selected food processing sectors," adapted from Statistics Canada publication Measuring industry concentration in Canada's food processing sectors, Agriculture and Rural Working Paper series no. 70, Catalogue 21-601,

http://www.statcan.gc.ca/pub/21-601-m/21-601-m2004070-eng.pdf.

Table 11.1 contains information on the 4-firm

concentration ratio for several sectors of the Canadian economy. It

indicates that, at one extreme, sectors such as breakfast cereals and sugars

have a high degree of concentration, whereas meat processing has much less.

A high degree of concentration suggests market power, and possibly economies

of scale.

11.4 Imperfect competition: monopolistic competition

Monopolistic competition presumes a large number of quite small producers or

suppliers, each of whom may have a slightly differentiated

product. The competition element of this name signifies that there are many

participants, while the monopoly component signifies that each supplier

faces a downward-sloping demand. In concrete terms, your local coffee shop

that serves "fair trade" coffee has a product that differs slightly from

that of neighbouring shops that sell the traditional product. They coexist

in the same sector, and probably charge different prices: The fair trade

supplier likely charges a higher price, but knows nonetheless that too large

a difference between her price and the prices of her competitors will see

some of her clientele migrate to those lower-priced establishments. That is

to say, she faces a downward-sloping demand curve.

The competition part of the name also indicates that there is free

entry and exit. There are no barriers to entry. As a consequence, we know

at the outset that only normal profits will exist in a long-run equilibrium.

Economic profits will be competed away by entry, just as losses will erode

due to exit.

As a general rule then, each firm can influence its market share to some

extent by changing its price. Its demand curve is not horizontal because

different firms' products are only limited substitutes. A lower price level

may draw some new customers away from competitors, but convenience or taste

will prevent most patrons from deserting their local businesses. In concrete

terms: A pasta special at the local Italian restaurant that reduces the

price below the corresponding price at the competing local Thai restaurant

will indeed draw clients away from the latter, but the foods are

sufficiently different that only some customers will leave the Thai

restaurant. The differentiated menus mean that many customers will continue

to pay the higher price.

A differentiated product is one that differs slightly from other products in the same market.

Given that there are very many firms, the theory also envisages limits to

scale economies. Firms are small and, with many competitors, individual

firms do not compete strategically with particular rivals. Because

the various products offered are slightly differentiated, we avoid graphics

with a market demand, because this would imply that a uniform

product is being considered. At the same time the market is a well-defined

concept—it might be composed of all those restaurants within a reasonable

distance, for example, even though each one is slightly different from the

others. The market share of each firm depends on the price that it charges

and on the number of competing firms. For a given number of

suppliers, a shift in industry demand also shifts the demand facing each

firm. Likewise, the presence of more firms in the industry reduces the

demand facing each one.

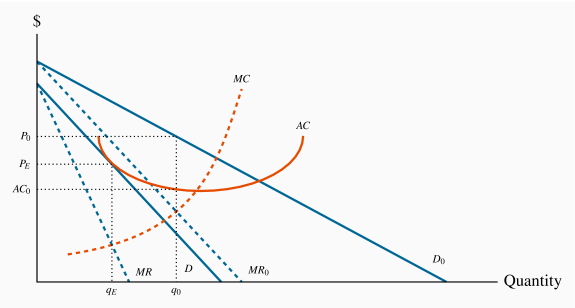

Equilibrium is illustrated in Figure 11.2. Here

D0 is the initial demand facing a representative firm, and MR0 is the

corresponding marginal revenue curve. Profit is maximized where MC=MR, and

the price P0 is obtained from the demand curve corresponding to the

output q0. Total profit is the product of output times the difference

between price and average cost, which equals  .

.

With free entry, such profits attract new firms. The increased number of

firms reduces the share of the market that any one firm can claim. That is,

the firm's demand curve shifts inwards when entry occurs. As long as

(economic) profits exist, this process continues. For entry to cease,

average cost must equal price. A final equilibrium is illustrated by the

combination  , where the demand has shifted inward to D.

, where the demand has shifted inward to D.

At this long-run equilibrium, two conditions must hold: First, the optimal

pricing rule must be satisfied—that is MC=MR; second it must be the case

that only normal profits are made at the final equilibrium. Economic profits

are competed away as a result of free entry. Graphically this implies that ATC must equal

price at the output where MC=MR. In turn this implies that the ATC is

tangent to the demand curve where P=ATC. While this could be proven

mathematically, it is easy to intuit why this tangency must exist: If ATC

merely intersected the demand curve at the output where MC=MR, we could

find some other output where the demand price would be above ATC,

suggesting that profits could be made at such an output. Clearly that could

not represent an equilibrium.

The monopolistically competitive equilibrium in the long run requires the firm's demand curve to be tangent to the ATC curve at the output where MR=MC.

11.5 Imperfect competition: economies of scope and platforms

The communications revolution has impacted market structure in modern

economies profoundly: it has facilitated economies of scope, meaning that

firms may yield more collective profit if merged than if operating

independently.

Economies of Scope

Imagine an aspiring entrepreneur who envisages a revolution of the

traditional taxi sector of the economy. He decides to develop a smartphone

application that will match independent income-seeking vehicle owners

(drivers) with individuals seeking transport (passengers) from point A to

point B. We know how this adventure evolves. In one case it takes the form

of the corporation Uber, in another the corporation Lyft, and others

worldwide.

These corporations have grown in leaps and bounds and have taken business

from the conventional taxi corporations. As of 2019 they cannot turn a

profit, yet the stock market continues to bet upon future success: investors

believe that when these corporations evolve into fully integrated

multi-product suppliers, both costs will decline and demand will increase

for each component of the business. In the case of transportation companies,

they aim to become a 'one-stop-shop' for mobility services. Uber is not only

a ride-hailing service, it also transports meals through its Uber-eats

platform, and is developing the electric scooter and electric bike markets

in addition. In some local markets it is linked to public transport

services. All of this is being achieved through a single smartphone

application. The objective is to simplify movement for persons, by providing

multiple options on a variety of transport modes, accessed through a single

portal.

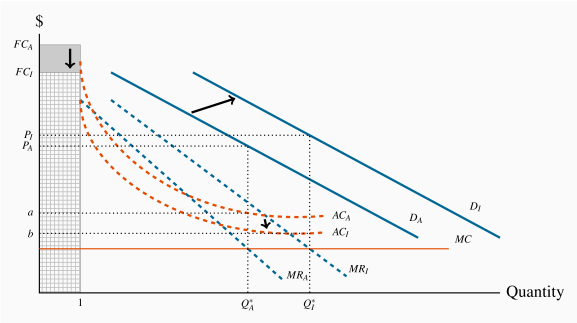

This phenomenon is described in Figure 11.3. The subscripts A and I

represent market conditions when the service supplier is operating Alone or

in an Integrated corporation. The initial equilibrium is defined by the A

demand and cost conditions. The profit maximizing output occurs when  , leading to a price

, leading to a price  and a quantity

and a quantity  .

Each unit of the good yields a profit margin of

.

Each unit of the good yields a profit margin of  .

.

This firm now merges with another transportation corporation - perhaps a

food delivery service, perhaps an electric bike service. Since each firm has

a similar type of fixed cost, these costs can be reduced by the merger. In

technical terms, the merged firms, or merged operations, share a common

hardware-cum-software platform. Each firm will therefore incur

lower average costs, even if marginal costs remain unchanged: the AC curve

declines to  . In addition to the decline in average costs, each firm

sees an increase in its customer base, because transportation service buyers

find it preferable to choose their mode of transport through a single portal

rather than through several different modes of access. This is represented

by an outward shift in the demand curve for vehicle rides to

. In addition to the decline in average costs, each firm

sees an increase in its customer base, because transportation service buyers

find it preferable to choose their mode of transport through a single portal

rather than through several different modes of access. This is represented

by an outward shift in the demand curve for vehicle rides to  .

.

The new profit maximizing equilibrium occurs at  Total

profit necessarily increases both because average costs have fallen and the

number of buyers willing to buy at any price has risen. The analytics in

this figure also describe the benefits accruing to the other firm or firms

in the merger.

Total

profit necessarily increases both because average costs have fallen and the

number of buyers willing to buy at any price has risen. The analytics in

this figure also describe the benefits accruing to the other firm or firms

in the merger.

A platform describes a technology that is common to more than one product in a multi-product organization.

We conclude from this analysis that, if scope economies are substantial, it

may be difficult for stand-alone firms specializing in just one component of

the transportation services sector to remain profitable. It may also be

impossible to define a conventional equilibrium in this kind of marketplace.

This is because some conglomerate firms may have different component

producers in their suite of firms. For example, Lyft may not have a food

delivery service, but it may have a limousine or bus service. What is

critical for an equilibrium is that firms of a particular type, whether they

are part of a conglomerate or not, be able to compete with corresponding

firms. This means that their cost structure must be similar.

As a further example: Amazon initially was primarily an on-line book seller.

But it expanded to include the sale of other products. And once it became a

'market for everything' the demand side of the market exploded in parallel

with the product line, because it becomes easy to shop for 'anything' or

even different objects on a single site. Only Walmart, in North America,

comes close to being able to compete with Amazon.

11.6 Strategic behaviour: Oligopoly and games

Under perfect competition or monopolistic competition, there are so many

firms in the industry that each one can ignore the immediate effect of its

own actions on particular rivals. However, in an oligopolistic industry

each firm must consider how its actions affect the decisions of its

relatively few competitors. Each firm must guess how its rivals will react.

Before discussing what constitutes an intelligent guess, we investigate

whether they are likely to collude or compete. Collusion is a

means of reducing competition with a view to increasing profit.

Collusion is an explicit or implicit agreement to avoid competition with a view to increasing profit.

A particular form of collusion occurs when firms co-operate to form a

cartel, as we saw in the last chapter. Collusion is more difficult if there

are many firms in the industry, if the product is not standardized, or if

demand and cost conditions are changing rapidly. In the absence of

collusion, each firm's demand curve depends upon how competitors react: If

Air Canada contemplates offering customers a seat sale on a particular

route, how will West Jet react? Will it, too, make the same offer to buyers?

If Air Canada thinks about West Jet's likely reaction, will it go ahead with

the contemplated promotion? A conjecture is a belief that one

firm forms about the strategic reaction of another competing firm.

A conjecture is a belief that one firm forms about the strategic reaction of another competing firm.

Good poker players will attempt to anticipate their opponents' moves or

reactions. Oligopolists are like poker players, in that they try to

anticipate their rivals' moves. To study interdependent decision making, we

use game theory. A game is a situation in which contestants

plan strategically to maximize their payoffs, taking account of rivals'

behaviour.

A game is a situation in which contestants plan strategically to maximize their payoffs, taking account of rivals' behaviour.

The players in the game try to maximize their own payoffs.

In an oligopoly, the firms are the players and their payoffs are their

profits. Each player must choose a strategy, which is a plan

describing how a player moves or acts in different situations.

A strategy is a game plan describing how a player acts, or moves, in each possible situation.

Equilibrium outcomes

How do we arrive at an equilibrium in these games? Let us begin by defining

a commonly used concept of equilibrium. A Nash equilibrium is

one in which each player chooses the best strategy, given the strategies

chosen by the other players, and there is no incentive to move or change

choice.

A Nash equilibrium is one in which each player chooses the best strategy, given the strategies chosen by the other player, and there is no incentive for any player to move.

In such an equilibrium, no player wants to change strategy, since the other

players' strategies were already figured into determining each player's own

best strategy. This concept and theory are attributable to the Princeton

mathematician John Nash, who was popularized by the Hollywood movie version

of his life, A Beautiful Mind.

In most games, each player's best strategy depends on the strategies chosen

by their opponents. Occasionally, a player's best strategy

is independent of those chosen by rivals. Such a strategy is called a

dominant strategy.

A dominant strategy is a player's best strategy, independent of the strategies adopted by rivals.

We now illustrate these concepts with the help of two different games. These

games differ in their outcomes and strategies. Table 11.2

contains the domestic happiness game. Will

and Kate are attempting to live in harmony, and their happiness depends upon

each of them carrying out domestic chores such as shopping, cleaning and

cooking. The first element in each pair defines Will's outcome, the second

Kate's outcome. If both contribute to domestic life they each receive a

happiness or utility level of 5 units. If one contributes and the other does

not the happiness levels are 2 for the contributor and 6 for the

non-contributor, or 'free-rider'. If neither contributes happiness levels

are 3 each. When each follows the same strategy the payoffs are on the

diagonal, when they follow different strategies the payoffs are on the

off-diagonal. Since the elements of the table define the payoffs resulting

from various choices, this type of matrix is called a payoff

matrix.

A payoff matrix defines the rewards to each player resulting from particular choices.

So how is the game likely to unfold? In response to Will's choice of a

contribute strategy, Kate's utility maximizing choice involves lazing: She

gets 6 units by not contributing as opposed to 5 by contributing. Instead,

if Will decides to be lazy what is in Kate's best interest? Clearly it is to

be lazy also because that strategy yields 3 units of happiness compared to 2

units if she contributes. In sum, Kate's best strategy is to be lazy,

regardless of Will's behaviour. So the strategy of not contributing is a

dominant strategy, in this particular game.

Will also has a dominant strategy – identical to Kate's. This is not

surprising since the payoffs are symmetric in the table. Hence, since each

has a dominant strategy of not contributing the Nash equilibrium is in the

bottom right cell, where each receives a payoff of 3 units. Interestingly,

this equilibrium is not the one that yields maximum combined happiness.

Table 11.2 A game with dominant strategies

|

| | Kate's choice |

|

| | Contribute | Laze |

|

Will's choice | Contribute | 5,5 | 2,6 |

| Laze | 6,2 | 3,3 |

The first element in each cell denotes the payoff or utility to Will; the second element the utility to Kate.

The reason that the equilibrium yields less utility for each player in this

game is that the game is competitive: Each player tends to their own

interest and seeks the best outcome conditional on the choice of the other

player. This is evident from the (5,5) combination. From this position

Kate would do better to defect to the Laze strategy, because her utility

would increase.

To summarize: This game has a unique equilibrium and each player has a

dominant strategy. But let us change the payoffs just slightly to the values

in Table 11.3. The off-diagonal elements have changed.

The contributor now gets no utility as a result of his or her contributions:

Even though the household is a better place, he or she may be so annoyed

with the other person that no utility flows to the contributor.

Table 11.3 A game without dominant strategies

|

| | Kate's choice |

|

| | Contribute | Laze |

|

Will's choice | Contribute | 5,5 | 0,4 |

| Laze | 4,0 | 3,3 |

The first element in each cell denotes the payoff or utility to Will; the second element the utility to Kate.

What are the optimal choices here? Starting again from Will choosing to

contribute, what is Kate's best strategy? It is to contribute: She gets 5

units from contributing and 4 from lazing, hence she is better contributing.

But what is her best strategy if Will decides to laze? It is to laze,

because that yields her 3 units as opposed to 0 by contributing. This set of

payoffs therefore contains no dominant strategy for either player.

As a result of there being no dominant strategy, there arises the

possibility of more than one equilibrium outcome. In fact there are two

equilibria in this game now: If the players find themselves both

contributing and obtaining a utility level of (5,5) it would not be

sensible for either one to defect to a laze option. For example, if Kate

decided to laze she would obtain a payoff of 4 utils rather than the 5 she

enjoys at the (5,5) equilibrium. By the same reasoning, if they find

themselves at the (laze, laze) combination there is no incentive to move to

a contribute strategy.

Once again, it is to be emphasized that the twin equilibria emerge in a

competitive environment. If this game involved cooperation or collusion the

players should be able to reach the (5,5) equilibrium rather than the

(3,3) equilibrium. But in the competitive environment we cannot say

ex ante which equilibrium will be attained.

Repeated games

This game illustrates the tension between collusion and competition. While

we have developed the game in the context of the household, it can equally

be interpreted in the context of a profit maximizing game between two market

competitors. Suppose the numbers define profit levels rather than utility as

in Table 11.4. The 'contribute' option can be

interpreted as 'cooperate' or 'collude', as we described for a cartel in the

previous chapter. They collude by agreeing to restrict output, sell that

restricted output at a higher price, and in turn make a greater total profit

which they split between themselves. The combined best profit outcome

(5,5) arises when each firm restricts its output.

Table 11.4 Collusion possibilities

|

| | Firm K's profit |

|

| | Low output | High output |

|

Firm W's profit | Low output | 5,5 | 2,6 |

| High output | 6,2 | 3,3 |

The first element in each cell denotes the profit to Firm W; the second element the profit to Firm K.

But again there arises an incentive to defect: If Firm W agrees to maintain

a high price and restrict output, then Firm K has an incentive to renege and

increase output, hoping to improve its profit through the willingness of

Firm W to restrict output. Since the game is symmetric, each firm has an

incentive to renege. Each firm has a dominant strategy – high output, and

there is a unique equilibrium (3,3).

Obviously there arises the question of whether these firms can find an

operating mechanism that would ensure they each generate a profit of 5 units

rather than 3 units, while remaining purely self-interested. This question

brings us to the realm of repeated games. For example,

suppose that firms make strategic choices each quarter of the year. If firm

K had 'cheated' on the collusive strategy it had agreed with firm W in the

previous quarter, what would happen in the following quarter? Would firms

devise a strategy so that cheating would not be in the interest of either

one, or would the competitive game just disintegrate into an unpredictable

pattern? These are interesting questions and have provoked a great deal of

thought among game theorists. But they are beyond our scope at the present

time.

A repeated game is one that is repeated in successive time periods and where the knowledge that the game will be repeated influences the choices and outcomes in earlier periods.

We now examine what might happen in one-shot games of the type we have been

examining, but in the context of many possible choices. In particular,

instead of assuming that each firm can choose a high or low output, how

would the outcome of the game be determined if each firm can choose an

output that can lie anywhere between a high and low output? In terms of the

demand curve for the market, this means that the firms can choose some

output and price that is consistent with demand conditions: There may be an

infinite number of choices. This framing of a game enables us to explore new

concepts in strategic behavior.

11.7 Strategic behaviour: Duopoly and Cournot games

The duopoly model that we frequently use in economics to analyze competition

between a small number of competitors is fashioned after the ideas of French

economist Augustin Cournot. Consequently it has come to be known as the Cournot duopoly model. While the maximizing behaviour that is

incorporated in this model can apply to a situation with several firms

rather than two, we will develop the model with two firms. This differs

slightly from the preceding section, where each firm has simply a choice

between a high or low output.

The critical element of the Cournot approach is that the firms each

determine their optimal strategy – one that maximizes profit – by reacting

optimally to their opponent's strategy, which in this case involves their

choice of output.

Cournot behaviour involves each firm reacting optimally in their choice of output to their competitors' output decisions.

A central element here is the reaction function of each firm,

which defines the optimal output choice conditional upon their opponent's

choice.

Reaction functions define the optimal choice of output conditional upon a rival's output choice.

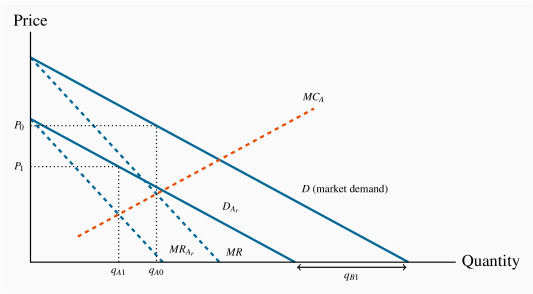

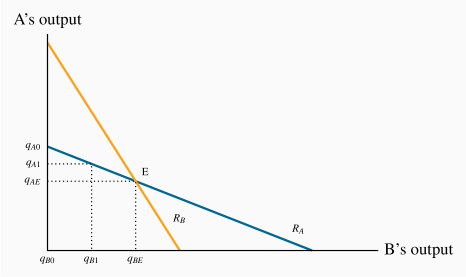

We can develop an optimal strategy with the help of Figure 11.4.

D is the market demand, and two firms supply this

market. If B supplies a zero output, then A would face the whole demand,

and would maximize profit where MC=MR. Let this output be defined by

. We transfer this output combination to Figure 11.5,

where the output of each firm is on one of the axes—A on the vertical

axis and B on the horizontal. This particular combination of zero output

for B and for A is represented on the vertical axis as the

point .

. We transfer this output combination to Figure 11.5,

where the output of each firm is on one of the axes—A on the vertical

axis and B on the horizontal. This particular combination of zero output

for B and for A is represented on the vertical axis as the

point .

Instead, suppose that B produces a quantity  in Figure 11.4.

This reduces the demand curve facing A

correspondingly from D to

in Figure 11.4.

This reduces the demand curve facing A

correspondingly from D to  , which we call A's residual demand. When subject to such a choice by B, firm A maximizes

profit by producing where

, which we call A's residual demand. When subject to such a choice by B, firm A maximizes

profit by producing where  , where

, where  is the

marginal revenue corresponding to the residual demand . The

optimum for A is now

is the

marginal revenue corresponding to the residual demand . The

optimum for A is now  , and this pair of outputs is represented by

the combination

, and this pair of outputs is represented by

the combination  in Figure 11.5.

in Figure 11.5.

Firm A forms a similar optimal response for every possible output level

that B could choose, and these responses define A's reaction

function. The reaction function illustrated for A in Figure 11.5

is thus the locus of all optimal response outputs on the

part of A. The downward-sloping function makes sense: The more B

produces, the smaller is the residual market for A, and therefore the less

A will produce.

But A is just one of the players in the game. If B acts in the same

optimizing fashion, B too can formulate a series of optimal reactions to

A's output choices. The combination of such choices would yield a

reaction function for B. This is plotted as  in Figure 11.5.

in Figure 11.5.

An equilibrium is defined by the intersection of the two reaction functions,

in this case by the point E. At this output level each firm is

making an optimal decision, conditional upon the choice of its opponent.

Consequently, neither firm has an incentive to change its output; therefore

it can be called the Nash equilibrium.

Any other combination of outputs on either reaction function would lead one

of the players to change its output choice, and therefore could not

constitute an equilibrium. To see this, suppose that B produces an output

greater than  ; how will A react? A's reaction function

indicates that it should choose a quantity to supply less than

; how will A react? A's reaction function

indicates that it should choose a quantity to supply less than  . If

so, how will B respond in turn to that optimal choice? It responds with a

quantity read from its reaction function, and this will be less than the

amount chosen at the previous stage. By tracing out such a sequence of

reactions it is clear that the output of each firm will move to the

equilibrium

. If

so, how will B respond in turn to that optimal choice? It responds with a

quantity read from its reaction function, and this will be less than the

amount chosen at the previous stage. By tracing out such a sequence of

reactions it is clear that the output of each firm will move to the

equilibrium  .

.

Application Box 11.1 Cournot: Fixed costs and brand

Why do we observe so many industries on the national, and even international, stages with only a handful of firms? For example, Intel produces more than half of the world's computer chips, and AMD produces a significant part of the remainder. Why are there only two major commercial aircraft producers in world aviation – Boeing and Airbus? Why are there only a handful of major North American suppliers in pharmaceuticals, automobile tires, soda pop, internet search engines and wireless telecommunications?

The answer lies primarily in the nature of modern product development. Product development (fixed) costs, coupled with a relatively small marginal cost of production, leads to markets where there is enough space for only a few players. The development cost for a new cell phone, or a new aircraft, or a new computer-operating system may run into billions, while the cost of producing each unit may in fact be constant. The enormous development cost associated with many products explains not only why there may be a small number of firms in the domestic market for the product, but also why the number of firms in some sectors is small worldwide.

The Cournot model yields an outcome that lies between monopoly (or

collusion/cartel) and competitive market models. It does not necessarily

assume that the firms are identical in terms of their cost structure,

although the lower-cost producer will end up with a larger share of the market.

The next question that arises is whether this duopoly market will be

sustained as a duopoly, or if entry may take place. In particular, if

economic profits accrue to the participants will such profits be competed

away by the arrival of new producers, or might there be barriers of either a

'natural' or 'constructed' type that operate against new entrants?

11.8 Strategic behaviour: Entry, exit & potential competition

At this point we inquire about the potential entry and impact of new firms

– firms who might enter the industry if conditions were sufficiently

enticing, meaning the presence of economic profits. One way of examining

entry in this oligopolistic world is to envisage potential entry barriers as

being either intended or unintended, though the difference between the two

can be blurred. Broadly, an unintended or 'natural' barrier is one related

to scale economies and the size of the market. An intended barrier involves

a strategic decision on the part of the firm to prevent entry.

Unintended entry barriers

Oligopolists tend to have substantial fixed costs, accompanied by declining

average costs up to high output levels. Such a cost structure

'naturally' gives rise to a supply side with a small number of suppliers.

For examples, given demand and cost structures, could Vancouver support two

professional soccer teams; could Calgary support two professional hockey

teams; could Montreal sustain two professional football teams? The answer to

each of these questions is likely 'no'. Because given the cost structure of

these markets, it would not be possible to induce twice as many spectators

without reducing the price per game ticket to such a degree that revenue

would be insufficient to cover costs. (We will neglect for the moment that

the governing bodies of these sports also have the power to limit entry.)

Fixed costs include stadium costs, staff payrolls and player payrolls. In

fact most costs in these markets are relatively fixed. Market size relative

to fixed and variable costs is not large enough to sustain two teams in most

cities. Exceptions in reality are huge urban areas such as New York and Los

Angeles.

Accordingly, it is possible that the existing team, or teams, may earn

economic profit from their present operation; but such profit does not

entice further entry, because the market structure is such that the entry of

an additional team could lead to each team making losses.

Intended entry barriers

Patent Law

This is one form of protection for incumbent firms. Research

and development is required for the development of many products in the

modern era. Pharmaceuticals are an example. If innovations were not

protected, firms and individuals would not be incentivized to devote their

energies and resources to developing new drugs. Society would be poorer as a

result. Patent protection is obviously a legal form of protection. At the same time, patent

protection can be excessive. If patents provide immunity from replication or

copying for an excessive period of time - for longer than required to recoup

R & D costs - then social welfare declines because monopoly profits are

being generated as a result of output restriction at too high a price.

Advertising

Advertising is a second form of entry deterrence. In this instance

firms attempt to market their product as being distinctive and even

enviable. For example, Coca-Cola and PepsiCo invest

hundreds of millions annually to project their products in this light. They

sponsor sports, artistic and cultural events. Entry into the cola business

is not impossible, but brand image is so strong for these firms that

potential competitors would have a very low probability of entering this

sector profitably. Likewise, in the 'energy-drinks' market, Red Bull

spends hundreds of millions of dollars per annum on Formula One racing, kite

surfing contests, mountain biking events and other extreme sports. In doing

this it it reinforcing its brand image and distinguishing its product from

Pepsi or Coca-Cola. This form of advertising is one of product

differentiation and enables the manufacturer to maintain a higher price for

its products by convincing its buyers that there are no close substitutes.

Predatory pricing

This form of pricing constitutes an illegal form of entry deterrence. It

involves an incumbent charging an artificially low price for its product in

the event of entry of a new competitor. This is done with a view to making

it impossible for the entrant to earn a profit. Given that incumbents have

generally greater resources than entrants, they can survive a battle of

losses for a more prolonged period, thus ultimately driving out the entrant.

An iconic example of predatory pricing is that of Amazon deciding to take on

a startup called Quidsi that operated the website diapers.com.

The latter was proving to be a big hit with consumers in 2009 and Amazon

decided that it was eating into Amazon profits on household and baby

products. Amazon reacted by cutting its own prices dramatically, to the

point where it was ready to loose a huge amount of money in order to grind

Quidsi into the ground. The ultimate outcome was that Quidsi capitulated

and sold to Amazon.

Whether this was a legal tactic or not we do not know, but it underlines the

importance of war chests.

Maintaining a war chest

Many large corporations maintain a mountain of cash. This might seem like an

odd thing to do when it could be paying that cash out to owners in the form

of dividends. But there are at least two reasons for not doing this. First,

personal taxes on dividends are frequently higher than taxes on capital

gains; accordingly if a corporation can transform its cash into capital gain

by making judicious investments, that strategy ultimately yields a higher

post-tax return to the stock holders. A second reason is that a cash war

chest serves as a credible threat to competitors of the type described

involving Amazon and Quidsi above.

Network externalities

These externalities arise when the existing number of buyers

itself influences the total demand for a product. Facebook is now a

classic example. An individual

contemplating joining a social network has an incentive to join one where

she has many existing 'friends'. Not everyone views the Microsoft

operating system (OS) as the best. Many prefer a simpler system such as

Linux that also happens to be free. However, the fact that almost

every new computer (that is not Apple) coming onto the market place

uses Microsoft OS, there is an incentive for users to continue to use it

because it is so easy to find a technician to repair a breakdown.

Transition costs and loyalty cards

Transition costs can be erected by firms who do not wish to lose

their customer base. Cell-phone plans are a good example.

Contract-termination costs are one obstacle to moving to a new supplier.

Some carriers grant special low rates to users communicating with other

users within the same network, or offer special rates for a block of users

(perhaps within a family). Tim Hortons and other coffee chains offer loyalty cards that give

one free cup of coffee for every eight purchased. These suppliers are not

furnishing love to their caffeine consumers, they are providing their

consumers with an incentive not to switch to a competing supplier. Air miles

rewards operate on a similar principle. So too do loyalty cards for hotel

chains.

How do competitors respond to these loyalty programs? Usually by offering

their own. Hilton and Marriot each compete by offering a free night after a

given points threshold is reached.

Over-investment

An over-investment strategy means that an existing supplier

generates additional production capacity through investment in new plant or

capital. This is costly to the incumbent and is intended as a signal to any

potential entrant that this capacity could be brought on-line immediately

should a potential competitor contemplate entry. For example, a ski-resort

owner may invest in a new chair-lift, even if she does not use it frequently. The

existence of the additional capacity may scare potential entrants. A key

component of this strategy is that the incumbent firm invests ahead of time

– and inflicts a cost on itself. The incumbent does not simply say "I will

build another chair-lift if you decide to develop a nearby mountain into a

ski hill." That policy does not carry the same degree of credibility as

actually incurring the cost of construction ahead of time. However, such a

strategy may not always be feasible: It might be just too costly to pre-empt

entry by putting spare capacity in place. Spare capacity is not so different

from brand development through advertising; both are types of sunk cost. The

threats associated with the incumbent's behaviour become a credible threat because the incumbent incurs costs up front.

A credible threat is one

that is effective in deterring specific behaviours; a competitor must

believe that the threat will be implemented if the competitor behaves in a

certain way.

Lobbying

In our chapter on monopoly we stressed the role of political/lobbying

activity. Large firms invariably employ public relations firms, and maintain

their own public relations departments. The role of these units is not

simply to portray a positive image of the corporation to the public; it is

to maintain and increase whatever market power such firms already possess.

It is as much in the interest of an oligopolistic firm as a monopolist to

prevent entry and preserve supernormal profits.

In analyzing perfect competition, we saw that free entry is critical to

maintaining normal profits. Lobbying is designed to obstruct entry, and it

is also designed to facilitate mergers and acquisitions. The economist

Thomas Philippon has written about the increasing concentration of economic

power in recent decades in the hands of a small number of corporations in

many sectors of the North American economy. He argues that this

concentration of power contributes to making the distribution of income more

favorable to corporate interests and less favorable to workers. In his

recent book ("The Great Reversal: How America Gave up Free

Markets" ), he shows that, contrary to traditional beliefs,

Europe is now much more competitive than the US in most sectors of the

economy. More broadband suppliers result in rates in Europe that are about

half of US rates. Whereas in the US four airlines control 80% of the

market, In Europe they control 40%. If scale economies were the prime

determinant of corporate concentration we should not expect such large

differences. Likewise, if globalization and technological change were the

main determinants of corporate concentration, we should expect experiences in

Europe and North America to be similar. But they are not. Hence, it is

reasonable to conclude that entry barriers in North America are more

effective, or that regulatory forces are stronger in Europe.

11.9 Matching markets: design

Markets are institutions that facilitate the exchange of goods and services.

They act as clearing houses. The normal medium of exchange is money in some form.

But many markets deal in exchanges that do not involve money and frequently

involve matching: Graduating medical students are normally matched with

hospitals in order that graduates complete their residency requirement; in

many jurisdictions in the US applicants for places in public schools that

form a pool within a given school-board must go through an application

process that sorts the applicants into the different schools within the

board; patients in need of a new kidney must be matched with kidney donors.

These markets are clearinghouses and have characteristics that distinguish

them from traditional currency-based markets that we have considered to this point.

The good or service being traded is generally heterogeneous.

For example, patients in search of a kidney donor must be medically

compatible with the eventual donor if the organ transplant is not to be

rejected. Hospitals may seek residents in particular areas of health, and

they must find residents who are, likewise, seeking such placements. Students

applying to public schools may be facing a choice between schools that focus

upon science or upon the arts. Variety is key.

Frequently the idea of a market that is mediated by money is repugnant. For example, the only economy in the world that permits the sale

of human organs is Iran. Elsewhere the idea of a monetary payment for a

kidney is unacceptable. A market in which potential suppliers of kidneys

registered their reservation prices and demanders registered their

willingness to pay is incompatible with our social mores. Consequently,

potential living donors or actual deceased donors must be directly

matched with a patient in need. While some individuals believe

that a market in kidneys would do more good than harm, because a monetary

payment might incentivize the availability of many more organs and therefore

save many more lives, virtually every society considers the downside to such

a trading system to outweigh the benefits.

Modern matching markets are more frequently electronically

mediated, and the communications revolution has led to an increase in the

efficiency of these markets.

The Economics prize in memory of Alfred Nobel was awarded to Alvin Roth and

Lloyd Shapley in 2011 in recognition of their contributions to designing

markets that function efficiently in the matching of demanders and suppliers

of the goods and services. What do we mean by an efficient mechanism? One

way is to define it is similar to how we described the market for apartments

in Chapter 5: following an equilibrium in the market, is it possible to

improve the wellbeing of one participant without reducing the wellbeing of

another? We showed in that example that the market performed efficiently: a

different set of renters getting the apartments would reduce total surplus

in the system.

Consider a system in which medical graduates are matched with hospitals, and

the decision process results in the potential for improvement: Christina

obtains a residency in the local University Hospital while Ulrich obtains a

residency at the Childrens' Hospital. But Christina would have preferred the

Childrens' and Ulrich would have preferred the University. The matching

algorithm here was not efficient because, at the end of the allocation

process, there is scope for gains for each individual. Alvin Roth devised a matching mechanism

that surmounts this type of inefficiency. He called it the deferred

acceptance algorithm.

Roth also worked on the matching of kidney donors to individuals in need of

a kidney. The fundamental challenge in this area is that a patient in need

of a kidney may have a family member, say a sibling, who is willing to

donate a kidney, but the siblings are not genetically compatible. The

patient's immune system may attack the implantation of a 'foreign' organ.

One solution to this incompatibility is to find matching pairs of donors

that come from a wider choice set. Two families in each of which there is patient

and a donor may be able to cross-donate: donor in Family A can donate to

patient in Family B, and donor in Family B can donate to patient in Family

A, in the sense that the donor organs will not be rejected by recipients'

immune systems. Hence if many patient-donor families register in a

clearinghouse, a computer algorithm can search for matching pairs.

Surgical operations may be performed simultaneously in order to prevent one donor from

backing out following his sibling's receipt of a kidney.

A more recent development concerns 'chains'. In this case a good Samaritan

('unaligned donor') offers a kidney while seeking nothing in return. The

algorithm then seeks a match for the good Samaritan's kidney among all of

the recipient-donor couples registered in the data bank. Having found (at

least) one, the algorithm seeks a recipient for the kidney that will come

from the first recipient's donor partner. And so on. It turns out that an

algorithm which seeks to maximize the potential number of participating

pairs is fraught with technical and ethical challenges: should a young

patient, who could benefit from the organ for a whole lifetime, get priority

over an older patient, who will benefit for fewer years of life, even if the

older patient is in greater danger of dying in the absence of a transplant?

This is an ethical problem.

Examples where these algorithms have achieved more than a dozen linked

transplants are easy to find on an internet search - they are called chains, for the obvious reason.

Consider the following efficiency aspect of the exchange. Suppose a patient

has two siblings, each of whom is willing to donate (though only one of the

two actually will); should such a patient get priority in the computer

algorithm over a patient who has just a single sibling willing to donate?

The answer may be yes; the dual donor patient should get priority

because if his two siblings have different blood types, this greater variety

on the supply side increases the chances for matching in the system as a

whole and is therefore beneficial. If a higher priority were not given to

the dual-donor patient, there would be an incentive for him to name just one

potential donor, and that would impact the efficiency of the whole matching

algorithm.

It is not always recognized that the discipline of Economics explores social

problems of the nature we have described here, despite the fact that the

discipline has developed the analytical tools to address them.

Conclusion

Monopoly and perfect competition are interesting paradigms; but few markets

resemble them in the real world. In this chapter we addressed some of the

complexities that define the economy we inhabit: It is characterized by

strategic planning, entry deterrence, differentiated products and so forth.

Entry and exit are critical to competitive markets. Frequently entry is

blocked because of scale economies – an example of a natural or unintended

entry barrier. In addition, incumbents can formulate numerous strategies to limit

entry.

Firms act strategically – particularly when there are just a few

participants in the market. Before acting, firms make conjectures about how

their competitors will react, and incorporate such reactions into their own

planning. Competition between suppliers can frequently be analyzed in terms

of a game, and such games usually have an equilibrium outcome. The Cournot

duopoly model that we developed is a game between two competitors in which

an equilibrium market output is determined from a pair of reaction functions.

Scale economies are critical. Large development costs or setup costs may mean

that the market can generally support just a limited number of producers. In

turn this implies that potential new (small-scale) firms cannot benefit from

the scale economies and will not survive competition from large-scale

suppliers.

Product differentiation is critical. If small differences exist

between products produced in markets where there is free entry we get a

monopolistically competitive structure. In these markets long-run profits

are 'normal' and firms operate with some excess capacity. It is not possible

to act strategically in this kind of market.

The modern economy also has sectors that have successfully erected barriers.

These barriers lead to fewer competitors than could efficiently supply the

market. Ultimately the owners of capital are the beneficiaries of these

barriers and consumers suffer from higher prices.

Key Terms

Imperfectly competitive firms face a downward-sloping demand curve, and their output price reflects the quantity sold.

Oligopoly defines an industry with a small number of suppliers.

Monopolistic competition defines a market with many sellers of products that have similar characteristics. Monopolistically competitive firms can exert only a small influence on the whole market.

Duopoly defines a market or sector with just two firms.

Concentration ratio: N-firm concentration ratio is the sales share of the largest N firms in that sector of the economy.

Differentiated product is one that differs slightly from other products in the same market.

The monopolistically competitive equilibrium in the long run requires the firm's demand curve to be tangent to the ATC curve at the output where MR=MC.

Collusion is an explicit or implicit agreement to avoid competition with a view to increasing profit.

Conjecture: a belief that one firm forms about the strategic reaction of another competing firm.

Game: a situation in which contestants plan strategically to maximize their profits, taking account of rivals' behaviour.

Strategy: a game plan describing how a player acts, or moves, in each possible situation.

Nash equilibrium: one in which each player chooses the best strategy, given the strategies chosen by the other player, and there is no incentive for any player to move.

Dominant strategy: a player's best strategy, whatever the strategies adopted by rivals.

Payoff matrix: defines the rewards to each player resulting from particular choices.

Credible threat: one that, after the fact, is still optimal to implement.

Cournot behaviour involves each firm reacting optimally in their choice of output to their competitors' decisions.

Reaction functions define the optimal choice of output conditional upon a rival's output choice.

Exercises for Chapter 11

Imagine that the biggest four firms in each of the sectors listed below produce the amounts defined in each cell. Compute the three-firm and four-firm concentration ratios for each sector, and rank the sectors by degree of industry concentration.

|

Sector | Firm 1 | Firm 2 | Firm 3 | Firm 4 | Total market |

|

Shoes | 60 | 45 | 20 | 12 | 920 |

|

Chemicals | 120 | 80 | 36 | 24 | 480 |

|

Beer | 45 | 40 | 3 | 2 | 110 |

|

Tobacco | 206 | 84 | 30 | 5 | 342 |

You own a company in a monopolistically competitive market. Your marginal cost of production is $12 per unit. There are no fixed costs. The demand for your own product is given by the equation P=48–(1/2)Q.

Plot the demand curve, the marginal revenue curve, and the marginal cost curve.

Compute the profit-maximizing output and price combination.

Compute total revenue and total profit [Hint: Remember AC=MC here].

In this monopolistically competitive industry, can these profits continue indefinitely?

Two firms in a particular industry face a market demand curve given by the equation P=100–(1/3)Q. The marginal cost is $40 per unit and the marginal revenue is MR=100–(2/3)Q. The quantity intercepts for demand and MR are 300 and 150.

Draw the demand curve and MR curve to scale on a diagram. Then insert the MC curve.

If these firms got together to form a cartel, what output would they produce and what price would they charge?

Assuming they each produce half of the total what is their individual profit?

The classic game theory problem is the "prisoners' dilemma." In this game, two criminals are apprehended, but the police have only got circumstantial evidence to prosecute them for a small crime, without having the evidence to prosecute them for the major crime of which they are suspected. The interrogators then pose incentives to the crooks-incentives to talk. The crooks are put in separate jail cells and have the option to confess or deny. Their payoff depends upon what course of action each adopts. The payoff matrix is given below. The first element in each box is the payoff (years in jail) to the player in the left column, and the second element is the payoff to the player in the top row.

|

| | B's strategy |

|

| | Confess | Deny |

|

A's strategy | Confess | 6,6 | 0,10 |

| Deny | 10,0 | 1,1 |

Does a "dominant strategy" present itself for each or both of the crooks?

What is the Nash equilibrium to this game?

Is the Nash equilibrium unique?

Was it important for the police to place the crooks in separate cells?

Taylormade and Titlelist are considering a production strategy for their new golf drivers. If they each produce a small output, they can price the product higher and make more profit than if they each produce a large output. Their payoff/profit matrix is given below.

|

| | Taylormade strategy |

|

| | Low output | High output |

|

Titleist strategy | Low output | 50,50 | 20,70 |

| High output | 70,20 | 40,40 |

Does either player have a dominant strategy here?

What is the Nash equilibrium to the game?

Do you think that a cartel arrangement would be sustainable?

Ronnie's Wraps is the only supplier of sandwich food and makes a healthy profit. It currently charges a high price and makes a profit of six units. However, Flash Salads is considering entering the same market. The payoff matrix below defines the profit outcomes for different possibilities. The first entry in each cell is the payoff/profit to Flash Salads and the second to Ronnie's Wraps.

|

| | Ronnie's Wraps |

|

| | High price | Low price |

|

Flash Salads | Enter the market | 2,3 | -1,1 |

| Stay out of market | 0,6 | 0,4 |

If Ronnie's Wraps threatens to lower its price in response to the entry of a new competitor, should Flash Salads stay away or enter?

Explain the importance of threat credibility here.

Optional: Consider the market demand curve for appliances: P=3,200–(1/4)Q. There are no fixed production costs, and the marginal cost of each appliance is  . As usual, the MR curve has a slope that is twice as great as the slope of the demand curve.

. As usual, the MR curve has a slope that is twice as great as the slope of the demand curve.

Illustrate this market geometrically.

Determine the output that will be produced in a 'perfectly competitive' market structure where no profits accrue in equilibrium.

If this market is supplied by a monopolist, illustrate the choice of output.

Optional: Consider the outputs you have obtained in Exercise 11.7.

Can you figure out how many firms would produce at the perfectly competitive output? If not, can you think of a reason?

If, in contrast, each firm in that market had to cover some fixed costs, in addition to the variable costs defined by the MC value, would that put a limit on the number of firms that could produce in this market?