Floating or flexible rates

In a floating or flexible exchange rate regime, the exchange rate is allowed to find its equilibrium level on the foreign exchange market without central bank intervention.

Flexible exchange rates: Supply and demand in the foreign exchange market determine the equilibrium exchange rate without central bank intervention.

Figures 12.2 and 12.3 showed the exchange rates that would result if rates adjusted flexibly and freely in response to changes in demand and supply. The central bank did not intervene to fix or adjust the rate. The rise in the demand for US dollars would result in a rise in the exchange rate to clear the foreign exchange market and maintain the balance of payments. Alternatively, the fall in demand would result in a fall in the exchange rate. The Bank of Canada would not intervene in either case. The holdings of official foreign exchange reserves and the domestic money supply would not be affected by foreign exchange market adjustments.

The alternative is a fixed exchange rate as explained below. In this regime, the central bank sets an official exchange rate and intervenes in the foreign exchange market to offset the effects of fluctuations in supply and demand and maintain a constant exchange rate. In Canada in the 1960s the exchange rate was fixed by policy at $1US=$1.075 Cdn ($1Cdn $0.925US) and the Bank of Canada intervened in the foreign exchange market to maintain that rate.

$0.925US) and the Bank of Canada intervened in the foreign exchange market to maintain that rate.

How do countries choose between fixed and floating exchange rates? Obviously, there is not one answer for all countries or we would not see different exchange rate regimes today. With flexible rates, the foreign exchange market sets the exchange rate, and monetary policy is available to pursue other targets. On the other hand, fixed exchange rates require central bank intervention. Monetary policy is aimed at the exchange rate.

The importance a country attaches to an independent monetary policy is one very important factor in the choice of an exchange rate regime. Another is the size and volatility of the international trade sector of the economy. A flexible exchange rate provides some automatic adjustment and stabilization in times of change in net exports or net capital flows.

Fixed exchange rates

In a fixed exchange rate regime, the government intervenes actively through the central bank to maintain convertibility of their currency into other currencies at a fixed exchange rate. A currency is convertible if the central bank will buy or sell as much of the foreign currency as people wish to trade at a fixed exchange rate.

Fixed exchange rate: an exchange rate set by government policy that does not change as a result of changes in market conditions.

Convertible currency: a national currency that can be freely exchanged for a different national currency at the prevailing exchange rate.

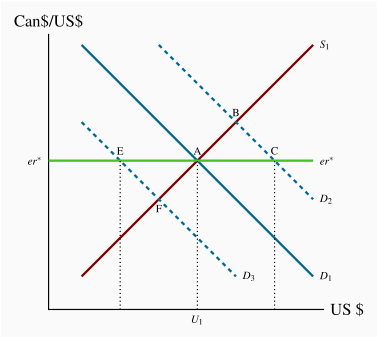

In Figure 12.4, suppose the exchange rate is fixed at  . There would be a free market equilibrium at A if the supply curve for US dollars is S1 and the demand curve for US dollars is D1. The central bank does not need to buy or sell US dollars. The market is in equilibrium and clears by itself at the fixed rate.

. There would be a free market equilibrium at A if the supply curve for US dollars is S1 and the demand curve for US dollars is D1. The central bank does not need to buy or sell US dollars. The market is in equilibrium and clears by itself at the fixed rate.

Suppose demand for US dollars shifts from D1 to D2. Canadians want to spend more time in Florida to escape the long, cold Canadian winter. They need more US dollars to finance their expenditures in the United States. The free market equilibrium would be at B, and the exchange rate would rise if the Bank of Canada took no action.

However, with the exchange rate fixed by policy at  there is an excess demand for US dollars equal to AC. To peg the exchange rate, the Bank of Canada sells US dollars from the official exchange reserves in the amount AC. The supply of US dollars on the market is then the "market" supply represented by S1 plus the amount AC supplied by the Bank of Canada. The payment the Bank receives in Canadian dollars is the amount (

there is an excess demand for US dollars equal to AC. To peg the exchange rate, the Bank of Canada sells US dollars from the official exchange reserves in the amount AC. The supply of US dollars on the market is then the "market" supply represented by S1 plus the amount AC supplied by the Bank of Canada. The payment the Bank receives in Canadian dollars is the amount ( AC), which reduces the monetary base by that amount, just like an open market sale of government bonds. The lower monetary base pushes domestic interest rates up and attracts a larger net capital inflow. Higher interest rates also reduce domestic expenditure and the demand for imports and for foreign exchange. The exchange rate target drives the Bank's monetary policy, which in turn changes both international capital flows and domestic income and expenditure.

AC), which reduces the monetary base by that amount, just like an open market sale of government bonds. The lower monetary base pushes domestic interest rates up and attracts a larger net capital inflow. Higher interest rates also reduce domestic expenditure and the demand for imports and for foreign exchange. The exchange rate target drives the Bank's monetary policy, which in turn changes both international capital flows and domestic income and expenditure.

Official exchange reserves: government foreign currency holdings managed by the central bank.

What if the demand for US dollars falls to D3? The market equilibrium would be at F. At the exchange rate at  there is an excess supply of US dollars EA. To defend the peg, the Bank of Canada would have to buy EA US dollars, reducing the supply of US dollars on the market to meet the "unofficial" demand. The Bank of Canada would have to buy EA US dollars, reducing the supply of US dollars on the market to meet the "unofficial" demand. The Bank of Canada's purchase would be added to foreign exchange reserves. The Bank would pay for these US dollars by creating more monetary base, as in the case of an open market purchase of government securities. In either case, maintaining a fixed exchange rate requires central bank intervention in the foreign currency market. The central bank's monetary policy is expansionary because it is committed to the exchange rate target.

there is an excess supply of US dollars EA. To defend the peg, the Bank of Canada would have to buy EA US dollars, reducing the supply of US dollars on the market to meet the "unofficial" demand. The Bank of Canada would have to buy EA US dollars, reducing the supply of US dollars on the market to meet the "unofficial" demand. The Bank of Canada's purchase would be added to foreign exchange reserves. The Bank would pay for these US dollars by creating more monetary base, as in the case of an open market purchase of government securities. In either case, maintaining a fixed exchange rate requires central bank intervention in the foreign currency market. The central bank's monetary policy is expansionary because it is committed to the exchange rate target.

Central bank intervention: purchases or sales of foreign currency intended to manage the exchange rate.

When the demand schedule is D2, foreign exchange reserves are running down. When the demand schedule is D3, foreign exchange reserves are increasing. If the demand for US dollars fluctuates between D2 and D3, the Bank of Canada can sustain and stabilize the exchange rate in the long run.

However, if the demand for US dollars is, on average, D2, the foreign exchange reserves are steadily declining to support the exchange rate  , and the monetary base is falling as well. In this case, the Canadian dollar is overvalued at

, and the monetary base is falling as well. In this case, the Canadian dollar is overvalued at  ; or, in other words,

; or, in other words,  is too low a price for the US dollar. A higher er is required for long-run equilibrium in the foreign exchange market and the balance of payments. As reserves start to run out, the government may try to borrow foreign exchange reserves from other countries and the International Monetary Fund (IMF), an international body that exists primarily to lend to countries in short-term difficulties.

is too low a price for the US dollar. A higher er is required for long-run equilibrium in the foreign exchange market and the balance of payments. As reserves start to run out, the government may try to borrow foreign exchange reserves from other countries and the International Monetary Fund (IMF), an international body that exists primarily to lend to countries in short-term difficulties.

At best, this is only a temporary solution. Unless the demand for US dollars decreases, or the supply increases in the longer term, it is necessary to devalue the Canadian dollar. If a fixed exchange rate is to be maintained, the official rate must be reset at a higher domestic currency price for foreign currency.

Devaluation (revaluation): a reduction (increase) in the international value of the domestic currency.

For many years frequent media and political discussions of the persistent rise in China's foreign exchange holdings provide a good example of the defense of an undervalued currency. With the yuan at its current fixed rate relative to US dollars and other currencies, China has a large current account surplus that is not offset by a financial account deficit. Balance of payments equilibrium requires ongoing intervention by the Chinese central bank to buy foreign exchange and add to official reserve holdings. Buying foreign exchange adds to the monetary base and money supply, raising concerns about inflation. The Bank has responded in part with a small revaluation of the yuan and in part with an increase in the reserve requirements for Chinese banks. Neither of these adjustments has been sufficient to change the situation fundamentally and growth in official foreign exchange reserves continues.

In Europe the euro currency system effectively fixes exchange rates among member countries. Individual member countries do not have national monetary policies. Monetary policy is set by the European Central Bank. In the years following the 'great recession' this has been a source of controversy because economic and fiscal conditions have differed significantly among countries. Countries trying to adjust fiscal deficits and national public debt crises have been forced into fiscal austerity without offsetting monetary policy support. In many cases the results have been deep and prolonged recessions without solving their debt problems. Greece is the poster child.

Of course, it is not necessary to adopt the extreme regimes of pure or clean floating on the one hand and perfectly fixed exchange rates on the other hand. Dirty or managed floating is used to offset large and rapid shifts in supply or demand schedules in the short run. The intent is to smooth the adjustment as the exchange rate is gradually allowed to find its equilibrium level in response to longer-term changes.

a shift in demand for US$ to D2 creates excess demand AC. The central bank intervenes, supplying AC US$ from official reserve holdings in exchange for Can$. To maintain

a shift in demand for US$ to D2 creates excess demand AC. The central bank intervenes, supplying AC US$ from official reserve holdings in exchange for Can$. To maintain  if demand shifted to D3 would create the opposite condition and central bank would have to buy US$.

if demand shifted to D3 would create the opposite condition and central bank would have to buy US$.